US Investment Management Firm GMO on How to Profit from a Growth Bubble

Rick Friedman of GMO

Apr 19, 2021

In a virtual event co-hosted on March 3 by Hubbis and US investment management firm GMO LLC (“GMO”), Hubbis invited a group of leading wealth management experts and gatekeepers across Asia to ‘Zoom’ in for a discussion titled ‘How to Profit from a Growth Bubble’, a topic that Jeremy Grantham, one of GMO’s co-founders, has long written about in the context of the relationship between market valuations and those ‘bubbles’, and how to ride through to extra returns. In fact, Jeremy Grantham was amongst the first to define ‘quality’ stocks in the early 1980s, and GMO’s research has shown that despite stretched equity valuations, the firm sticks firmly to the view that investing in the highest-quality, strongest, safest companies has generally delivered better performance than the broad markets, with lower absolute risk over the long term. The discussion event included presentations from Rick Friedman, Portfolio Strategist and a member of GMO’s Asset Allocation team, and also from Kimball Mayer, Portfolio Strategist, who oversees investor relations as well as a research analyst within the GMO’s Focused Equity team. Together they reviewed the current valuation levels across asset classes globally, reviewed the GMO benchmark-free allocations of today and zoomed in on the opportunity created by the wide spreads between value and growth stocks globally. They explained that the scale of such dislocation looks in some ways similar to that created by the Tech bubble in the late 1990s but with key differences, and they presented some ideas on smart implementation to capitalise on the opportunity set that is arising as a result of this dislocation. Aside from offering insights into their approach to equity dislocation, they presented great detail on their Quality Portfolio Strategy, they also offered some interesting insights to their Resources Strategy, pointing to its role in hedging against inflation, and within briefly explained about their very topical, dedicated Climate Change portfolio.

Key Observations from GMO’s Asset Allocation Team

GMO’s Rolling Seven-Year Views

Since 1994, GMO has been producing its much-anticipated and highly-regarded seven-year forecasts, and building a long history of bold calls on bubbles that had saved clients from large losses and helped them outperform the key comparables and benchmarks. Investors have perennially mispriced assets, never more so than at periods of excess fear or greed.

Growth has been Trumping Value

The charts GMO offered delegated show very clearly how value has been losing out to growth for some years, especially since around 2012, and that in 2020 there was an even more dramatic shift driving what look like bubble valuations of many stocks, especially those such as Tesla, GameStop and many others that have been driven by what seems to be pure speculation. QuantumScape, a company that GMO likes in terms of its potential, was propelled to a ‘scary’ valuation of USD80 billion but is still perhaps two years away from producing any revenues at all.

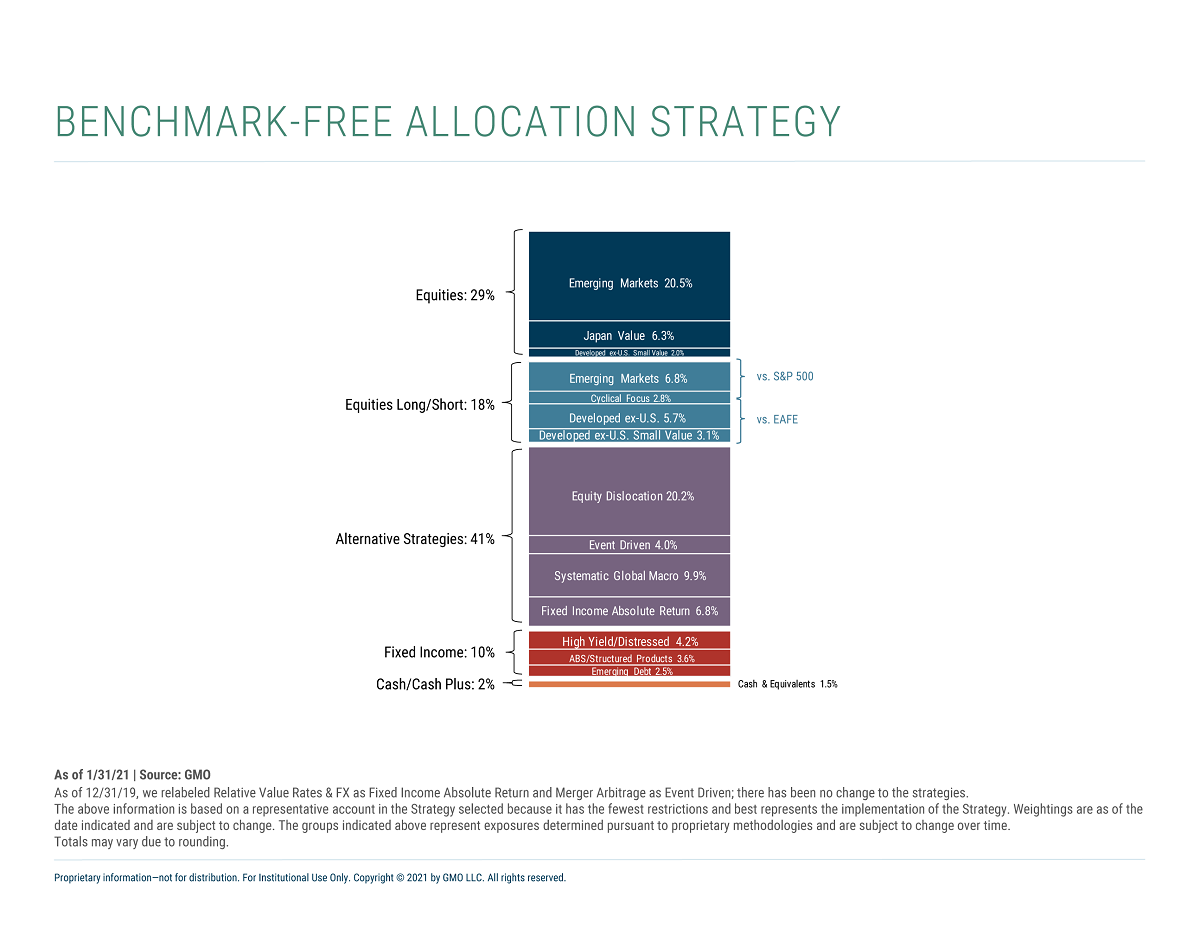

The Big Picture – GMO’s Benchmark-Free Portfolio Allocation

GMO reported that despite the exuberance around equities, especially in the US, there are still opportunities in equities, including international value, emerging value, and Japanese value. Far from the old 60/40 norm of a normalised financial world of yore, the GMO benchmark-free global allocation today is only 29% long equities, 18% long/short equity, 41% in alternative strategies (of which equity dislocation is roughly half, and the rest event-driven assets, systematic global macro and fixed income absolute return), and only 10% in fixed income, with virtually nothing in duration such as sovereign debt or Treasury inflation protected securities.

Equity Dislocation Strategy Turns Adversity into Opportunity

Since its launch in October, GMO has turned price/fair value into a long-short strategy, which represents 20.2% of the total benchmark-free GMO allocation, or nearly half of the 41% alternative strategies within GMO’s benchmark-free allocation. The dislocation strategy involves assessment of the global opportunity and building a broadly diversified portfolio across a wide number of companies – more than 200 in total none of which represent more than 1% of the allocation - and across many countries/regions to move in line with the discount that value trades at relative to growth and with a beta of zero.

Equity Dislocation offers Robust Returns

GMO’s long portfolio positions in this dislocation strategy, at 10.6 times forward earnings, are much cheaper than the market, and a similar story emerges for price to book or price to sales. Since GMO launched this approach in late October 2020, the performance was up 8.6% through January 31, while the equity dislocation beta to the value versus growth was 1.02.

GMO’s Global Quality Strategy offers Selectivity with Low Risk

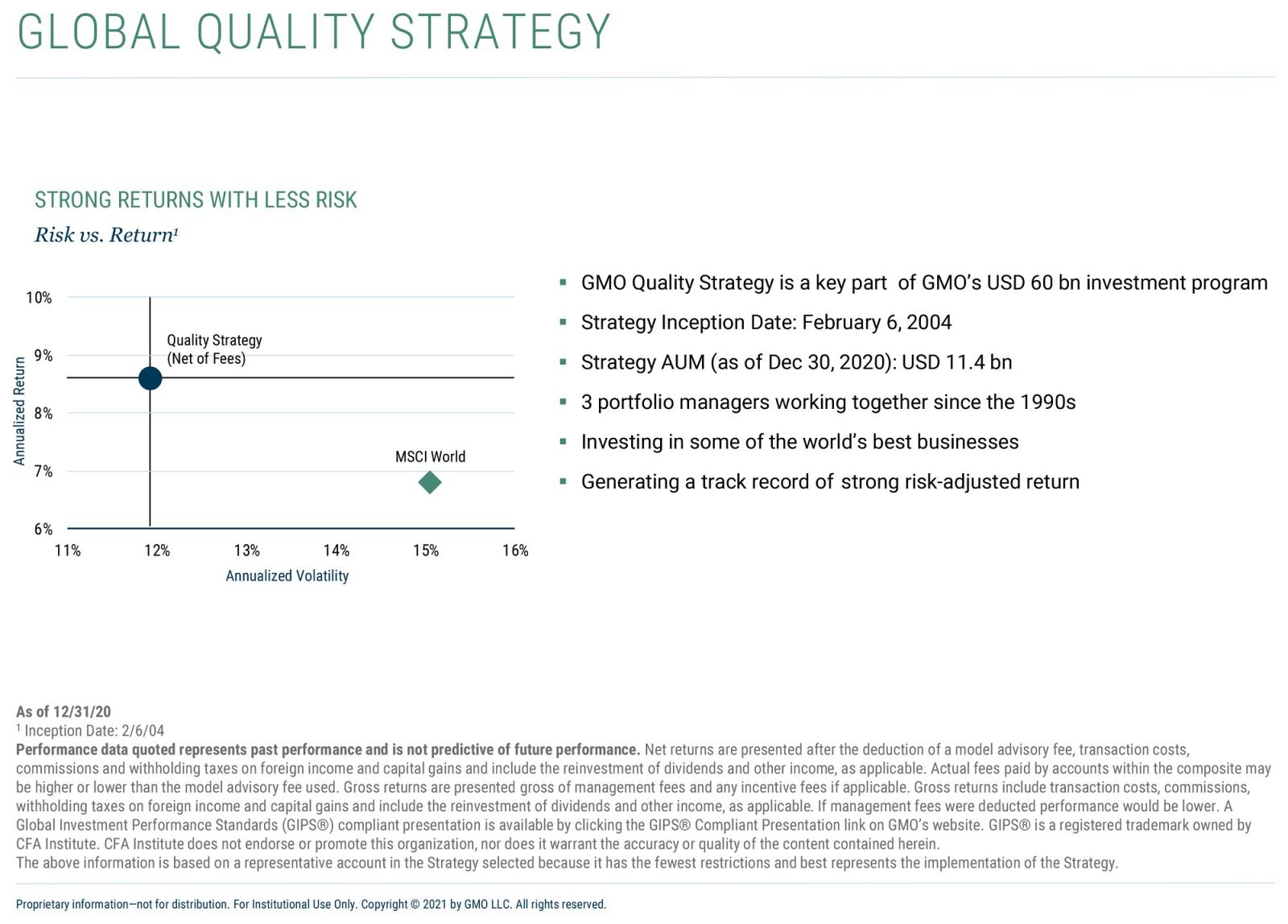

GMO’s flagship Global Quality Strategy, at roughly USD11.5 billion in early March, is central to GMO’s overall USD60 billion-plus total investment programme. The strategy launched in 2004 and has generated a track record of strong risk adjusted returns, beating the MSCI World by over 150 basis points per year during the 17 years of the strategy. Moreover, it is relatively lower risk, delivering annualised volatility of just under 12%, compared to annualised volatility of about 15% for MSCI World.

The Allocation to Quality Must be Carefully Defined and Smartly Assembled

GMO offered a variety of key criteria for its selection of companies for the Quality strategy, including high and sustainable return on capital, long-term durability of business model, and management demonstrating discipline and prudent investment of capital. Selecting these companies out carefully, from 1990 to 2020, quality had outperformed global companies through filtering the opportunities based on strong return on capital, a stable return on capital, low leverage and manageable valuations.

Despite Superior Quality, Value and Defensiveness Are Available

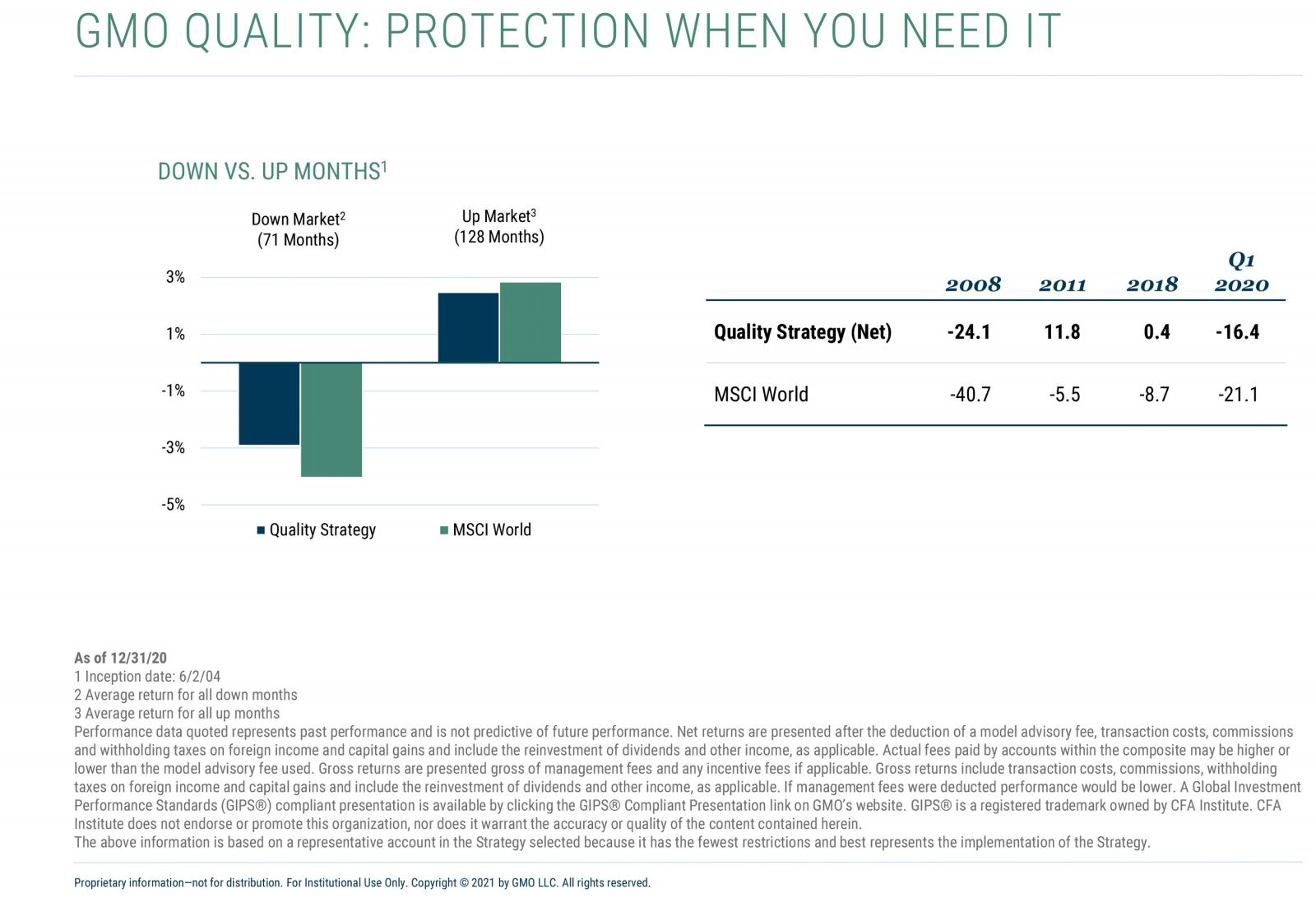

Despite the superior attributes of the ‘quality’ companies GMO has assembled in this strategy, they are only trading at levels in line with the rest of the market. Moreover, this portfolio is more defensive, offering downside protection relative to benchmark indices, outperforming particularly during periods of extreme stress, for example in 2008, when the strategy dropped only 24% compared with a slump of nearly 41% for the MSCI World Index.

The GMO Quantitative Filtering Methodology

GMO starts with a ‘quality’ basket of some 2000 names and securities to which a quantitative screen is first applied, combined with fundamental vetting to assess each potential investment’s quality, and ends up with a high conviction portfolio of about 40 to 50 names.

Key Sectors Dominate the Quality Allocation

This process has thrown up several key sectors and themes that dominate the portfolio – technology is over 40%, back-to-normal names account for somewhat over 25%, healthcare roughly 25% and classic defensive names a few percent.

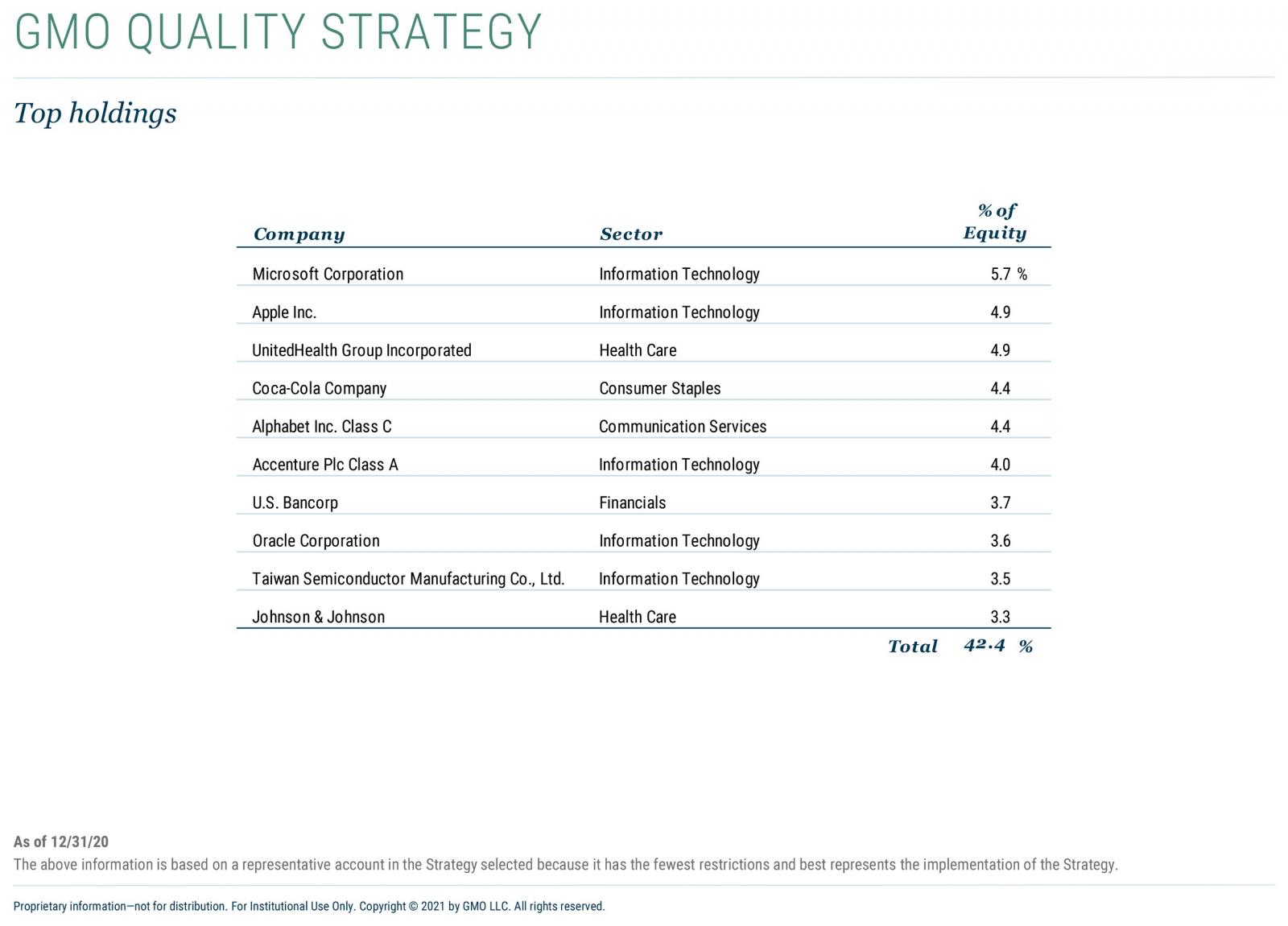

GMO’s Top 10 Quality Names

The Quality strategy at the end of February had its top 10 portfolio holdings ranging from Microsoft Corporation Information Technology at 5.7% to Johnson & Johnson at 3.3% with the other eight names comprising Apple, UnitedHealth Group, Coca-Cola, Alphabet, Class C Communication Services, Accenture Class A, US Bancorp, Oracle, and TSMC.

Want a Hedge against Inflation in the Portfolio? Consider Resources…

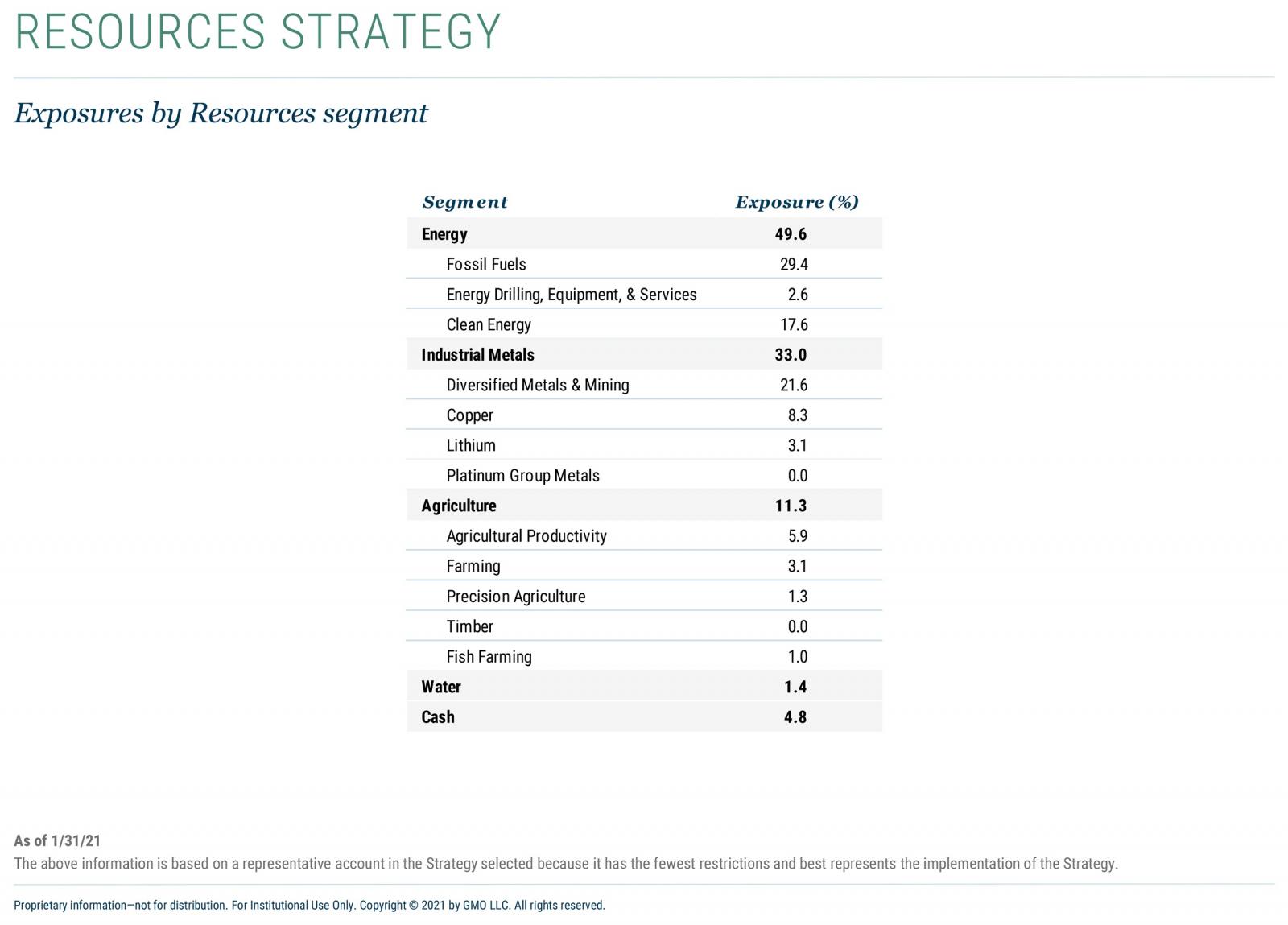

GMO recognises that inflation might take off and that in any well-balance total portfolio, a hedge for that in the form of resources stocks is advisable. The GMO Resources Strategy does precisely that, focusing on energy companies, metals companies, agricultural companies, and water companies, and is globally diversified. Within those segments, there is careful elimination of certain stocks, for example no fossil fuels, no refiners, no water utilities and so forth, and all the businesses must produce a positive correlation with a rising commodity price.

Selected Resources Stocks offer Tremendous Value today

The selected stocks for this allocation had over the past three decades traded at about a 25% discount to the market, but today that figure is nearer a 70% discount. And the portfolio is globally diversified, with the US accounting for slightly under 25%, and the other roughly 75% of holdings spread broadly across around 10 countries across the world, from Canada to the UK to China and Australia. Since inception in December 2011, the Resources Strategy has produced annualised total returns of 8.8% and a past five-year record of 16%, as at the end of January this year.

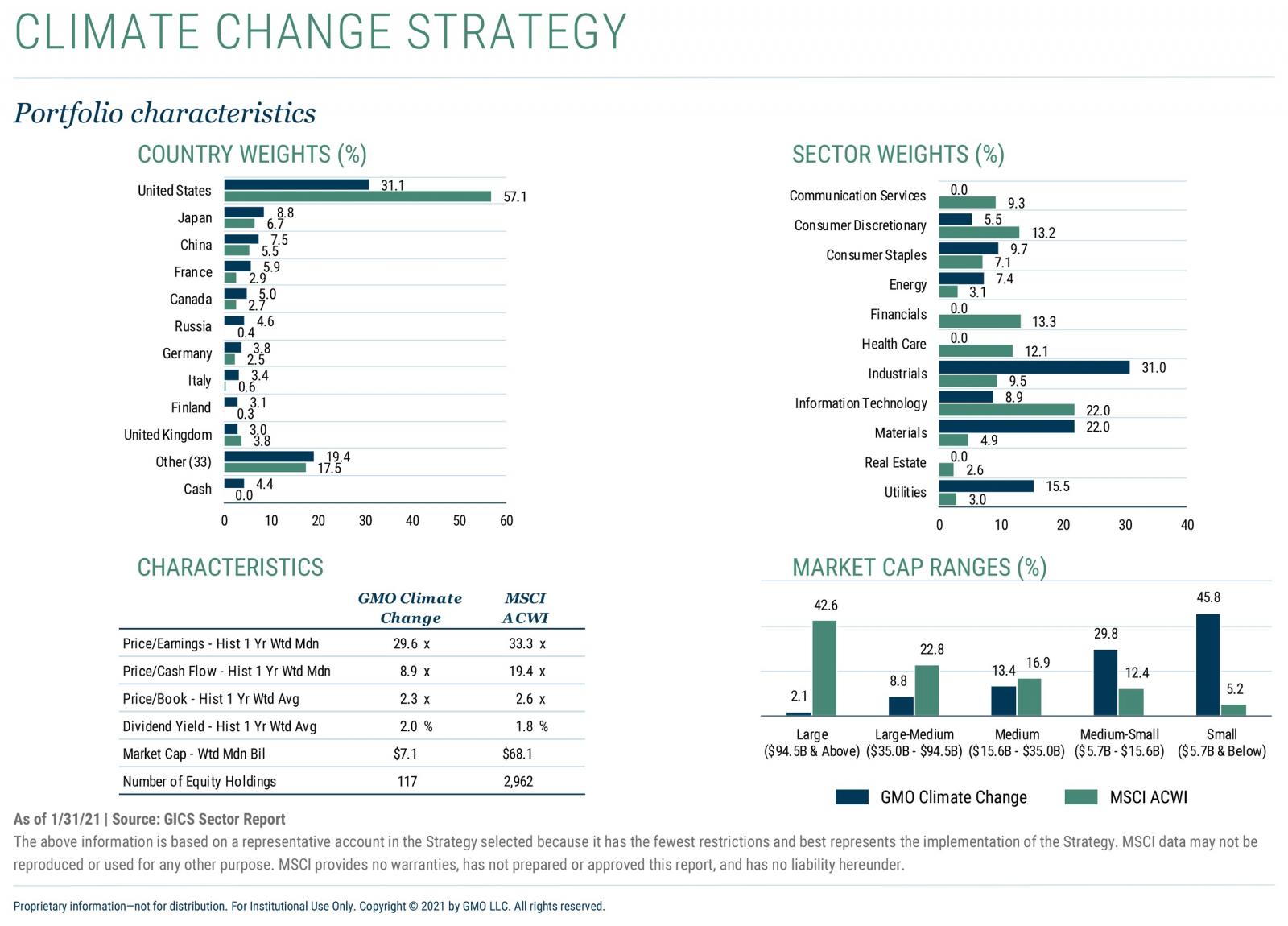

GMO’s Climate Change Strategy offers Clean and Appealing Returns

GMO has also since 2017 created a specialised subset of the Resources portfolio that only focuses on the clean energy transition, centring on climate change as a key force, and including the agriculture sector too. The companies in this strategy are focused on either climate change mitigation or are helping the world adapt to climate change. In the past one year the portfolio was up 32.7% at the end of January, and was up 6.8% annualised since inception in April 2017.

2021 a Year of Transition, so Let’s Hope 2022 sees Greater ‘Normality’

There was a lively Q&A session after GMO’s presentations (see below) and the final word went to GMO who said that with the vaccines rolling out, 2021 is more of a year of transition, and echoed global sentiment that we must all hope 2022 will be the year when things start to resemble what we knew before.

The Main Event

GMO – a determinedly contrarian value-seeker

Mehak Dua, a member of GMO’s Global Client Relations team located in the Singapore office, opened the discussion, highlighting GMO’s history dating back to 1977, when GMO was founded as a private partnership whose sole business is investment management, as it is today. She remarked how one of the GMO co-founders, Jeremy Grantham, is a well-regarded value investor often quoted in the media and reported that GMO’s quarterly letters and the 7-year forecasts produced by GMO’s Asset Allocation team are widely read across the financial world.

The firm manages global portfolios with offices and clients around the world. Investment offerings include equity, fixed income, multi-asset class, and alternative strategies. GMO is known for blended fundamental and quantitative investment research expertise and a long-term orientation toward value opportunities. GMO is currently managing USD63 billion of strategies from its HQ in Boston, from where the teams work closely with the firm’s six different locations around the globe.

Taking the long view

“As a private partnership,” Dua reported, “our sole business is that of investment management, and we only take the longer-term view. GMO is willing and able to take and hold significant and unconventional positions when we see markets move to extreme valuations. We take a contrarian value investment approach to identify and exploit opportunities, and the rationale behind this approach is that economic reality and investor behaviour cause securities and markets to overshoot their fair value. We focus on compounding wealth for our clients by identifying mispriced opportunities and then exploiting them in a systematic and disciplined way.”

She also highlighted the firm’s differentiated research, explaining that GMO counts as clients some of the most prestigious and sophisticated investors globally. “We are well known for our candid, academically-rigorous market insights and advice that underpin the research that we undertake,” she explained.

Focusing on the wealth community

She added that while GMO has been institutional focused historically, over the last couple of years, the firm is increasingly working with the wealth channel and the intermediary channel. “Accordingly, we are really delighted to see many of you here today from the wealth and asset management community in Asia, where we have had a presence since the early 2000s out of Singapore,” she said. “We will highlight approaches, products and vehicles that are very well suited for the wealth channel in addition to the institutional channel. My keywords for you today are that GMO is value-sensitive, long-term in outlook, and often contrarian.”

GMO’s topics of the day – Quality, Value, Resources & Sustainability

With that, Dua introduced Rick Friedman, who joined the discussion from California, and Kimball Mayer, who joined from Boston.

“Together they will analyse how GMO perceives markets and asset valuations today,” Dua reported. “Specifically, they will focus on the GMO Quality Strategy, which is an evergreen strategy that focuses on companies that we believe are of high quality, and this is a strategy that we've run at the firm for several years since 2004 and it's done exceedingly well, delivering returns north of 9%. They will also cover two thematic strategies, our Resources Strategy and within that the Climate Change Strategy, the latter of which has been a great performer in the past year.

Friedman and Mayer

She explained that Rick Friedman is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2013, he was a senior vice president at AllianceBernstein and before that a partner at Arrowpath Venture Capital and a principal at Technology Crossover Ventures. He earned his B.S. in Economics from the University of Pennsylvania and his MBA from Harvard Business School.

And she noted that Kim Mayer oversees investor relations and is also a research analyst within GMO’s Focused Equity team. Previously at GMO, he was a member of the Global Equity team focusing on the Quality Strategy. Prior to joining GMO in 2006, he managed the U.S. fixed income syndicate desk at Morgan Stanley. He earned his B.A. in History from Princeton University.

Friedman paints the Big Picture

Working through a high quality 50-page slide presentation, Friedman highlighted how GMO had since 1994 been producing seven-year forecasts, and during the past roughly four decades the firm has built a long history of bold calls on bubbles that had saved clients from large losses and had for many years delivered quarterly letters, white papers, and thought leadership reports that had provided clients with detailed explanations of our thinking on important topics.

“When valuations become very dispersed from one another,” he reported, “we have both gone on record, often early in saying something is amiss, and oftentimes built and delivered an individual strategy to benefit from the bursting of that bubble.”

Avoiding bubbles and fixed income

He explained that since time in memoriam investors had continually mispriced assets. And he reported that GMO today is de-risked due to many uncertainties and is accordingly aiming to be robust across varied outcomes, rotated longs into Long/Short, excited about Emerging Value equity, and cautious on duration.

He reported that as a result and based on the 7-year forecast for returns from January 31, the firm is bearish on fixed income, and negative on much of the US equity space, negative but less so on international large caps and Emerging Markets equity, and that despite the overall scenario globally, that there are most definitely some very interesting pockets of opportunity in equities, including international value, emerging value, and Japanese value.

Growth smashes value in 2020

“We can see from the charts how value had been slowly losing to growth for quite some years,” he explained. “And then we reach 2020 and suddenly we see a dramatic shift that shows we have reached what we would consider to be a bubble in growth, and broadly bubble valuations of stocks, although with some stocks, which Kim will point to later, potentially able to maintain a profit advantage for a long time ahead.”

He elaborated on this point, adding that there is a second criteria for a bubble prevalent today, namely raw speculation. “We see fervour, enthusiasm, crazy behaviour, or as my boss Bin Inker calls it ‘stupidity’,” he stated. “We see stories such as the hype around electric vehicles driving valuations of stocks such as Tesla ever upwards. Yes, Tesla is a phenomenal company, I have one of their cars, but they have produced a mere roughly 400,000 units out of roughly 44 million worldwide in the past year, yet it is valued at more than all the other auto companies combined.”

Rolling the dice…

He pointed to another stock propelled by this fervour, QuantumScape. “Actually, Jeremy Grantham, our founder, is a big investor in the company, a big believer, but it has leapt in a very short time to more than USD80 billion in valuation but will have no revenues for a couple of years. And a different type of scenario can affect lower quality narratives, for example a company like Hertz, which actually was in bankruptcy when its price quadrupled during the past summer. In short, this all looks like we are getting to the end here, just like we saw in the late 1990s before the Tech bubble burst.”

That led Friedman to then explain GMO’s current flagship benchmark free allocation strategy, which he reported broadly aims to deliver inflation plus 5%.

GMO’s Benchmark-Free Allocation Today

“If everything was priced at fair or equilibrium levels, investors historically might have about 60% in stocks, and 40% in bonds,” he reported. “But today we are only 29% long equities, some 18% long/short equity, and only 10% in fixed income, with virtually nothing in duration such as sovereign debt or Treasury inflation protected securities. And we have 41% in alternative strategies, which comprise equity dislocation, event-driven assets, systematic global macro and fixed income absolute return.”

He explained that the ‘bounce’ of the portfolio allocation as it stands is in trying to capture some sort of relative value disparity, especially the 18% equity long-short (comprising stocks GMO prefers) and the 41% alternatives (which are essentially pure hedge fund style strategies).

“Of the allocation to alternatives,” he added, “we have since October last year built up the 20.2% equity dislocations strategy to benefit from that combination of extreme valuations and movement up in growth stocks relative to value and the speculative fervour that was building. At just over 20%, this has become a significant part of our portfolio.”

Exploiting the gaps

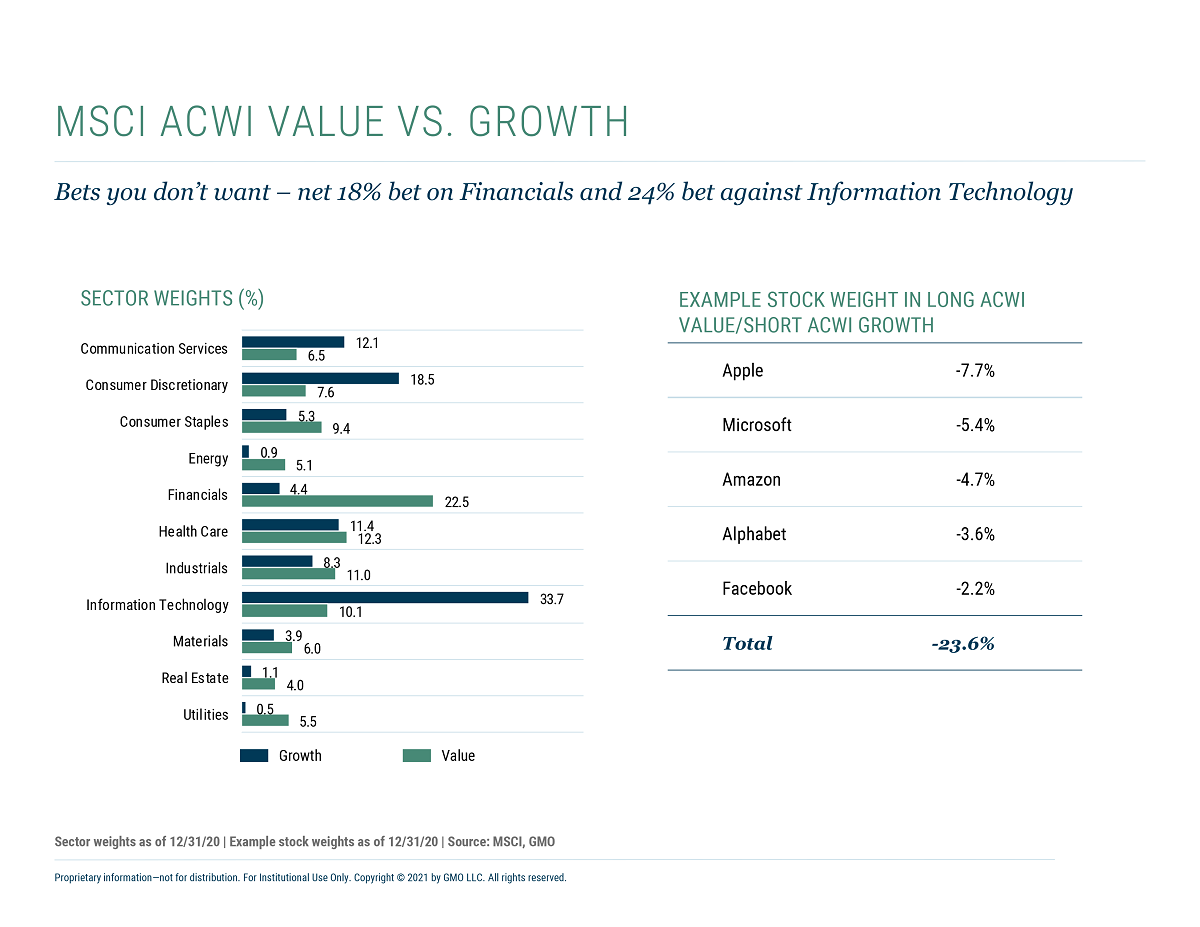

He then explained how GMO proposes that investors benefit from any major gaps between value and growth stocks, noting that GMO has proven track record of identifying and profiting from such dislocations, that value is extraordinarily cheap, that many growth companies show signs of speculative excess, that the opportunity looks similar to the one created by the Tech bubble, and therefore that the adoption of a long/short strategy can generate meaningful absolute returns, providing there is a concomitant smart and risk-controlled approach to avoid pitfalls of ‘style-box’ value versus growth.

Investing, not placing bets

Friedman explained that an investor could buy the MSCI ACWI value index and short the growth index, but that would result in some significant sector bets, such as 18% overweight financials, and 24% underweight information technology, with some major single stock risk, such as betting 7.7% against Apple, and 5.4% against Microsoft.

But what GMO proposes via the Equity Dislocation strategy is turning price/fair value into a long-short strategy. This involves looking at the global opportunity set with US, EAFE, and EM names, a diversified portfolio with less than 1% maximum position size and 200 to 250 names per side, meaningful sector tilts at plus or minus industry and sector limits, small country bets with plus or minus 3% country limits, and entirely non-directional, with 100% each side with an ex-ante beta of approximately zero.

“What we are expressing through this allocation,” he reports, “is that the disparity between growth and value is global in nature, so we are everywhere, we are across different sectors, and we avoid single-stock risks. We are trying to build a portfolio that will move in line with the gap, or the discount that value trades at relative to growth; as that narrows, we want to be winning regardless of what's happening in the stock market, hence a beta of zero.”

Referring to a chart on page 17 of the presentation, Friedman concluded his portion of the presentation by noting that GMO’s Equity Dislocation long portfolio positions at 10.6 times forward earnings are much cheaper than the market at 50 plus times on the short side, and a similar story emerges for price to book or price to sales.

“That's pretty staggering right now, the number of companies at 10, 20, even 50 times price to sales,” he remarked. “And then you add in our 200 plus name diversification and other risk controls and we end up with the exposure that we want, long betting with cheap stocks, betting against those many expensive stocks.”

He concluded that the result since GMO launched this approach in late October has been robust absolute performance of 8.6% to end January and outperformed the ACWI value minus ACWI growth, which was up 6.5% at the same date. “And importantly, as it's been a short period of measure, the equity dislocation beta to the value versus growth was 1.02, a good achievement.”

His final comment was that GMO believes this represents a significant return opportunity, and that on the back of this strategy, GMO had successfully onboarded some sophisticated endowments, an RAA and a number of family offices since they started offering the strategy at the end of November.

Kim Mayer zooms in on Quality

Kim Mayer then took the floor for the second portion of the presentation, titled ‘Investing in Equities during a Growth Bubble: Quality and Value’. “My case today is that it is still possible, despite the conditions that exist in the markets, to invest successfully in equities during a growth bubble,” he stated. “You just need to be willing to look quite different from the rest of the market.”

He looked first at GMO’s Global Quality Strategy, highlighting how growth stock prices have skyrocketed despite much of the developed world remaining in some form of lockdown, he pointed to interest rates at extraordinarily low levels around the world, and maintained that quality investing looks attractive for participating in responsible growth and getting a good night’s sleep.

He reiterated and expanded on some of Friedman’s comments about over-exuberance, noting that Tesla surged around 800% during 2020, and that new SPACs - Special Purpose Acquisition Vehicles – had been emerging literally daily. “It is tough,” he observed, “to think of SPACs as anything more than a compensation scheme that's dressed up to look like an investment scheme, yet they're proliferating like crazy. Add in names like GameStop, and the ‘Robinhood’ phenomenon here in the US and it appears like a lot of crazy, speculative behaviour out there.”

The global quest for Quality

He moved on to how investors should react to all this, pointing to GMO’s flagship Global Quality Strategy, at roughly USD11.5 billion today very clearly a key part of GMO’s overall USD60 billion investment programme.

“We started the strategy back in 2004. We have three portfolio managers on it that have been working together since the 1990s, and with GMO for over 25 years, and very simply we invest in some of the world's best companies, and by doing so, we've generated a track record of strong risk adjusted returns and have been able to beat MSCI World by over 150 basis points per year during the 17 years of the strategy.”

Moreover, he reported this had been achieved with substantially less risk, delivering annualised volatility of just under 12%, compared to annualised volatility of about 15% for MSCI World Index.

Defining characteristics of quality

He then went into considerable detail about what makes a company qualify for the GMO quality status. Firstly, the company generates high and sustainable return on capital. Secondly, they are relevant with proven long-term durability of business model, and thirdly they exhibit capital discipline, with management having a proven record of investing prudently and with a long horizon.

He explained that from 1990 to 2020, during those three decades, quality had outperformed global companies. He observed that these companies are able to generate growth at a higher rate than the rest of the market over long periods of time, with GMO applying its quantitative definition of quality based on the three identifiers that Jeremy Grantham came up with back in the early days of GMO, focusing in on companies that generate strong return on capital, a stable return on capital and low leverage.

Long-term durability

“Moreover,” he added, “they generate revenue growth that is consistently higher than inflation. This is perhaps not the exciting, short, steep trajectory that many investors are chasing today, but is more long-term durable growth that can be delivered over years and years. And that is why these companies truly are compounding machines.”

He reported that despite the superior attributes of the ‘quality’ companies in the portfolio, they are only trading at levels in line with the rest of the market. “We have built our quality universe using valuation as the primary stock selection tool,” he elucidated. “Accordingly, this portfolio that gives investors responsible exposure to both growth and value, without any of the extremes of either.”

Beating the benchmarks

He pointed to another attribute, namely the portfolio is more defensive, offering downside protection relative to benchmark indices. For example, in Q1 2020, the decline was 16.4% versus 21.1% for the MSCI, and in 2018 the drop was minimal at minus 0.4% compared to a fall of over 8% for the MSCI. “Ours is a portfolio that during average down months does substantially better than MSCI World, and then during periods of up markets it does a very good job of keeping up,” he commented. “then during times of extreme stress and volatility such as in 2008, it performs even more favourably, dropping just over 24% during the global financial crisis compared with a fall of nearly 41% for the MSCI World.”

Screening and filtering

He then ran delegates through the selection process, which moves from a universe of some 2000 securities to which a quantitative screen is first applied, combined with fundamental vetting to assess each potential investment’s quality, looking backward and forward, and through to the valuation work to ensure the most hyped-up quality companies are avoided. In the end there is a high conviction portfolio of about 40 to 50 names.

Sectors and themes

Mayer explained that GMO’s final allocation to this strategy centres on four sectors, which paint a thematic picture dominating. Technology accounts for over 40%, back-to-normal names account for somewhat over 25%, health care roughly 25% and classic defensive names a few percent.

He ran through some of the names in each segment, with examples from the technology sector, the largest of the sectors represented, being names such as Accenture, Texas Instruments and Taiwan’s TSMC. Accenture, he commented, has delivered compounded growth of 7% per year over the past 20 years, during that time multiplying its value by roughly 20 times. Texas Instruments, he said, is a great example of a company that has differentiated approach to semiconductors, making analogue semiconductors that are very different from the commoditised memory chips, with longer product cycles, and higher switching costs. He remarked that the company also boasts what he called tremendous capital allocation discipline.

The best ‘back-to-normals’

Amongst the back-to-normal names, financials such as US Bancorp and American Express feature large. “These types of businesses traded down as a result of the pandemic, but that we feel they have the balance sheet strength and the liquidity profile to survive a prolonged downturn, if that's what eventually occurs here,” he commented, “but they also have the strength to thrive when things return to normal. We have consumer facing names within that as well, such as Coca-Cola, traditionally thought of as a classic defensive company but that has suffered from the hiatus in the hospitality and restaurant segment.” But of course, the company is likely to bounce back dramatically if and when ‘normal’ life resumes.

Also in this back-to-normal segment, there are industrial names such as Raytheon, or B2B names such as Compass, the global caterer. “Raytheon,” he observed, “is in defence, and it also has an important airplane engine building and servicing business that was badly impacted by the pandemic, but we feel like it will be able to return to strong growth ahead.

Health and vitality

And the healthcare names are diversified across big pharmaceutical names such as Roche, medical device companies like Medtronic, and also managed care or health insurance providers, such as UnitedHealth Group, the last of which he noted had been compounding at an incredible 30% per year since 1987. “We've owned this company in our portfolio since we started back in 2004,” he reported, “and since 1987, it has multiplied its value over 160 times for investors. Truly incredible.”

GMO’s Top 10 Quality stocks

Mayer highlighted the top 10 portfolio holdings, ranging from Microsoft Corporation Information Technology at 5.7% to Johnson & Johnson at 3.3% with the other eight names comprising Apple, UnitedHealth Group, Coca-Cola, Alphabet, Class C Communication Services, Accenture Class A, US Bancorp, Oracle, and TSMC. And finally, he explained that in terms of revenues, the portfolio is very similar in terms of exposure to US revenues, developed market ex-US revenues, and emerging markets’ revenues.

He concluded this segment by commenting that GMO has been a pioneer in quality investing for some four decades, bringing a powerful blend of quantitative discipline as well as fundamental analysis. “It is an excellent way to deliver a lower-risk equity returns with that protection investors want,” he said.

GMO’s Resources Strategy – hedging some bets

Mayer then focused briefly on the firm’s Resources strategy, which he said offers a truly compelling valuation opportunity. The strategy focuses on four segments, namely energy companies, metals companies, agricultural companies, and water companies, and is globally diversified.

“But we invest only in those companies that have a positive correlation with a rising commodity price,” he reported, “and that is an important secular trend for investors to have as part of their portfolio, we believe. “Investors and advisors be aware that this is an excellent route to generate some form of inflation protection within overall portfolios.”

He explained that some 50% of the portfolio is currently in energy, but only about 30% of that in fossil fuels companies, with the bulk centred on clean energy and on equipment and services companies as well. Some one third of the portfolio is in industrial metals, just over 11% in agriculture and a small allocation of below 2% in the water sector.

“Valuation determines our selection,” he explained. “Once we eliminate companies that we do not investor in for strategic reasons, for example in energy we do not touch refiners of pipelines, in water we exclude the utilities and focus on engineering, recycling and efficiencies.”

Compelling valuations

As to the valuations, he noted that on average the stocks for the past three decades had traded at about a 25% discount to the market. “And look at where they are today,” he remarked. “After a run in the second half of 2020, they're still trading at somewhere around a 70% discount to the rest of the market. Well, you square that with the expectations for commodity price rise with the inflation protection that this type of portfolio can offer, and we think it's a really compelling opportunity.”

He then pointed to the global diversification of the allocation, with the US accounting for slightly under 25%, and stocks broadly held across countries such as Russia, the UK, Brazil, Canada, Australia, China, India, Mexico and Norway, as well as some holdings dotted around smaller countries.

Since inception in December 2011, the Resources Strategy has produced annualised total returns of 8.8% and a past five-year record of 16%, as at the end of January this year. “Overall,” he concluded, “whether you're looking at the one-, three- or five-year track record or performance since inception in 2011, we've significantly added value versus our index, and we've delivered a series of returns that looks significantly different from any of our competitors.”

Mayer added that since April 2017, GMO even has a specialised version of this portfolio that only focuses on the clean energy transition. This is the Climate Change Strategy that centres on climate change as a key force, and include the agriculture sector too. “We've been managing this strategy since 2017, so coming up on our fourth year, and again, we have really achieved a very compelling track record, both versus the index as well as versus our competitors in the field,” he reported.

The Climate Change Strategy enjoyed a stellar 2020, rising 32.7% by the end of January this year, and at that time was up 6.8% annualised since inception in April 2017.

Conclusion

The tasks of investors and wealth managers have in many ways seldom been more difficult, as the world faces up to the ongoing pandemic and the ensuing economic, financial, social and welfare uncertainties. But we must all hope and believe the world will return to some or most, ideally all, of its former shape.

History tells us much about the future, and GMO’s value-based approach is carved out of the long history of the global financial markets. Delegates who attended the virtual presentations and discussion were offered some fascinating opportunities to consider, founded on sound principles that have created not only GMO’s benchmark-free allocation of today, but also the particular strategies within that to offer investors some cause for optimism about the years ahead.

GMO – A Snapshot

GMO offers a snapshot of the firm for investors and wealth management partners:

Global Asset Management Firm: GMO is a USD 63 bn Boston-headquartered global asset management firm founded in 1977, with offices at 6 different locations around the globe. One of our co-founders is Jeremy Grantham, a well-regarded value investor often quoted in the same breath as Warren Buffett. Jeremy’s quarterly letters and 7-year forecasts are widely read in the industry.

Long-Term Investing: We are a private partnership and this structure means our sole business is investment management. As an independently-owned private partnership, we are built to invest the way we believe will deliver the best results over the long-term for our clients. At GMO, we are willing and able to take and hold significant and unconventional positions when we see markets move to extreme valuations.

Contrarian Value Investing: We take a contrarian value investment approach to identify and exploit opportunities and the rationale behind this approach is that economic reality and investor behaviour cause securities and markets to overshoot their fair value. We focus on compounding wealth for our clients by identifying mispriced opportunities and then exploiting them in a systematic and disciplined way.

Differentiated Research: We are proud to serve some of the most prestigious and sophisticated investors globally and work hard to partner with them. We are well known for our candid, academically-rigorous market insights and advice that underpin the research that we undertake.

Addendum – the Audience Q&A

After the fascinating presentations by GMO, delegates had a few minutes to pose some questions. Hubbis has briefly summarised the questions and the GMO responses as below.

Delegate: Is there a bubble right now? How cautious should people be right now?

GMO/Friedman: Is this 2000 all over? Not quite, but there are some similarities. It is difficult to imagine that someone who buys GameStop at USD150, that was USD40 a day earlier is thinking that is justified by fundamentals. No, they're simply hoping that it goes to USD300. So retail investors are flooding in.

But the differences are there too. The tech bubble of 2000 was much more concentrated in the US, in particular, and in internet and TMT stocks. Now it is across every sector, but not quite as extended. Moreover, back in 1999/2000, the Fed was raising rates. Today, it is very different from that perspective. If we are in a low-rate world forever, our view is, stocks are still expensive, so growth stocks trading at 50 times are still ridiculously expensive.

Delegate: How do you apply ESG criteria to the quality growth strategy?

GMO/Mayer: ESG are critical and yes, we certainly integrate ESG criteria as we build that portfolio. Firstly, companies that have sound ESG practices are most likely to be those companies that are going to be relevant, durable, and sustainable into the future. And companies that are on the other side of that, that have poor environmental records, poor governance, those tend to get screened out. And then as we're fundamentally vetting the output of our quant models to build the highest conviction quality universe that we can, and again as we're doing the valuation work, so if we're going to look at a company that has poor social practices, tobacco for example, we impose draconian terminal valuation assumptions into our DCF models, because of the effect that they obviously have on their customer base over time.

I would not hold all this up to be an ESG strategy, but instead a strategy that has always integrated ESG practices and that has very, very strong third-party metrics in terms of the ESG scores of the individual companies in the portfolio as well as overall at the portfolio level as well.

Delegate: What are your views on the bond market, the steepening of the curve, and the impact on stocks?

GMO/Friedman: The common narrative is growth stocks have more of their earnings in future years, so a lower discount rate benefits those future earnings, therefore I can pay a higher multiple and we've certainly seen in this cycle, groups of growth stocks that have benefitted as interest rates have gone lower. Yet the irony now is if rates are down, it is because we're in a low growth world, and everything's going to be stagnant for a while, therefore so too are your growth rates. Our view is we do not try to invest based on kind of the shift of the yield curve, either the steepening or the actual level.

GMO/Kim Mayer: It's kind of a conundrum. It is also tough to think about historical precedents when we're looking at real interest rates potentially rising from negative levels. We do however know that as discount rates rise, it should, at least in theory, penalise growth companies that have a slightly longer duration than value companies. And so, the way we try to sort of mitigate those risks is to find those companies that do have long-term secular growth rates in front of them, that have proven track records in being able to manage their companies successfully through a number of different environments, including a number of different interest rate environments.

And we have moved the portfolio deliberately away from some of those bond proxy companies, those that are very much still a part of our quality universe but that got very expensive four or five years ago as people chased yield. That is how we mitigate that type of risk in our portfolio.

Delegate: Out here in Asia, when we look at portfolios with 50% to 60% still in US equities, why not reorient a portfolio much more strongly towards the emerging markets, which of course includes China, likely to be the biggest economy in the world, in about five years from now?

GMO/Mayer: We do not deliberately practice any kind of home country bias in any of the portfolios in our group, but yes our Quality Strategy is primarily invested in companies that are domiciled in the US, and that's because there's an interesting phenomenon in the quality universe itself, which is that quality companies are not significantly cheaper in Europe, or in Asia than they are in the United States, they tend to all trade at pretty similar valuations to each other. I can say it is their ‘quality-ness’ that drives where they're trading and it's a pretty global phenomenon.

But there is slightly higher risk in some emerging economies than there is in the US economy, so that keeps us positioned more within the US. If valuations were lower outside the US, we would absolutely move the portfolio that way.

The other portfolios that I mentioned, the resource equity portfolio, the climate change portfolio, these are substantially underweight their global indices to the US. And that's because these are much more pure value plays, and we're finding much better opportunities, because we're not constrained by operating just within the quality universe. So, you can see clearly that we absolutely are taking advantage of some of those compelling valuation opportunities and materials companies, metals companies, energy companies that are in developing economies as well around the world.

Delegate: Do you see inflation ahead and what is the impact of inflation or possibly deflation on the Quality Portfolio?

GMO/Friedman: We have not managed the portfolio in a major deflation driven correction, we have however managed the quality portfolio during something that nearly approached that through the financial crisis of 2007-2008. This is a portfolio that because it is invested in companies that have strong fundamentals, that have proven track records of being able to deliver profitability that is much less economically sensitive than the average market.

It did of course drop in 2008 but relatively outperformed significantly to the benchmarks. Our expectation is that technology would fare best, so too healthcare, but back-to-normal allocations would suffer. Overall, our expectation would be that this would be a portfolio that at least in relative terms, would deliver much better results than broad markets.

Delegate: Are we likely to see a significant correction in the equity markets in the US or globally this year?

GMO/Friedman: We are not in the business of predicting indices. Our orientation is to say, we think long enough in the future, if the underlying drivers ever return there, what can we expect? Our forecasts are our best guess, and they show we don't think that a likelihood of a 30% to 40% drawdown is imminent. Could you see a 20% drawdown? Yes, that could absolutely happen tomorrow because the thing with these types of situations is, while it's going up, it's great, it pulls in new money willing to buy an asset that is absolutely overvalued relative to its fair or intrinsic value, but these are tantamount to market Ponzi schemes drawing in new money all the time. But when it turns, it can all unwind very quickly, like we saw with GameStop, and many other instances in the past.

I would certainly be prepared for more volatility, perhaps the image of inflation is transitory, hard to say, but it may spook the market and if selling begets selling, the passive money that flooded in might flood out. All in all, however, I don't think the 40% drawdown is ahead, especially with the amount of stimulus and conditioned buying on the dips we have seen.

GMO/Mayer: When is the world going to return to normal? The vaccines are rolling out, but we are not expecting a significant return to normal in 2021, it will continue to be a year of transition. Perhaps 2022 will be the year when things start to resemble what we knew before.

Disclaimer

The views expressed are the views of GMO through the period ending March 3, 2021, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Product Strategist, Asset Allocation at GMO

More from Rick Friedman, GMO

Latest Articles