The Private Wealth Management Market in Indonesia – a Mid-2021 Update

Jun 25, 2021

Indonesia’s huge population is growing fast, and so too has the country’s private wealth been expanding apace, albeit slowed by the pandemic. Money has in recent years flowed back onshore following the government’s tax amnesty, and the regulators are keen to keep that onshore and boost the onshore proposition. A panel of experts assembled for a virtual Digital Dialogue discussion on June 15 to present delegates with their views on the evolution of the wealth management industry and what needs to be done for it to develop more robustly. Greater regulatory creativity is certainly needed, with the regulators working more closely with the private sector, and perhaps taking a more proactive position in terms of liberalisation of the financial sector. There is a huge conservatism amongst those with money, with deposits still the preferred option for an estimated 90%-plus of the investible money available, which is little surprise given that interest rates in a global context remain relatively high, even though they have dropped sharply in recent years. The 10-year government bond, for example is over 6.5% and the one-year rate is over 3.1% still today. And although equities on the Jakarta Stock Exchange Composite Index are up some 32% since March 2020, investors remain wary, as that recovery is from a more than 40% fall in only a matter of weeks in January and February last year. And of course, access to foreign equities in the onshore market remains sorely limited. Set against this backdrop, the panel offered some very valuable insights into the evolutionary path of the wealth management market in Indonesia.

Panel Members

- Ivan Kusuma, Senior Vice President, Investment & Liabilities Dept Head, Commonwealth Bank

- Damien Piper, Regional Director, Asia, InvestCloud

- Vincent Magnenat, Chief Executive Officer, Asia, Lombard Odier

- Samdarshi Sumit, President Director & CEO, PFI Mega Life Insurance

- Patrick Donaldson, Head of Proposition Sales, ASEAN, Refinitiv

- Meru Arumdalu, Head of Wealth Management, Standard Chartered Bank

A banker opened by commenting that within SE Asia, Indonesia ranks highly in terms of market potential as it is immensely populous, is full of growth (albeit stifled by the pandemic) and replete with entrepreneurs and dynamism, with more and more joining the ranks of the mass affluent, wealthy and uber-rich, and in all segments needing a greater array of products and different levels of advice.

Positioning for the great opportunity Indonesia offers

He explained that their private bank’s partnership with a major domestic financial group is designed to combine the strengths of two organisations and align a very international expertise with remarkable local knowledge and reach.

He remarked that to build the proposition, they had concentrated on building a deep understanding of the clients, their needs and expectations, and then offering a holistic approach to their investments and associated advice. He reported that there had been gradual progress in the country towards liberalisation, allowing a greater range of offshore assets to be bought locally, but that the pace of change remains relatively slow. “We are investing time and effort to build relationships for the long-term,” he reported. “We look far ahead to the future generations as well.”

Still waiting and hoping for more liberalisation

Another panellist explained that the market is still waiting and hoping for the arrival of conventional offshore mutual funds, although Shariah compliant funds had been approved by the regulator some five years ago.

“It means that any diversification for Indonesian investors is limited mostly to the Indonesian equity market, stocks and funds, and bonds, which means mostly Indonesian government paper,” he reported. “This means severe limitations, especially for the very wealthy investors. If those wealthy clients have access to foreign wealth management services, they tend to buy directly from overseas, so there is good reason for the regulator to liberalise, as the demand is certainly there.”

However, he acknowledged that one of the understandable concerns of the regulators and government is the risk of capital flight because if everyone opts for offshore investments, then the local markets will suffer a dearth of investment capital. “It is true that the local market needs to be properly supported,” he said, “so the regulators appear to feel they still need time to observe and see what's the best way of developing the Indonesian market. It is simply a question of the pace of liberalisation.”

Mutual fund growth onshore, but progress is also slow

He added that domestic appetite for local mutual funds had continued to rise, but with customers numbering only about 4 million nationwide, compared to the population of some 276 million, the penetration rate remains very low.

“But the growth from this low level is some 80% in 2020 alone,” he reported, “driven by increased awareness and digitalisation, making it easier to transact. Education is certainly a key to progress; hence the wealth industry stakeholders are now increasingly distributing information and education through social media, in the absence of much direct contact with actual or potential customers.”

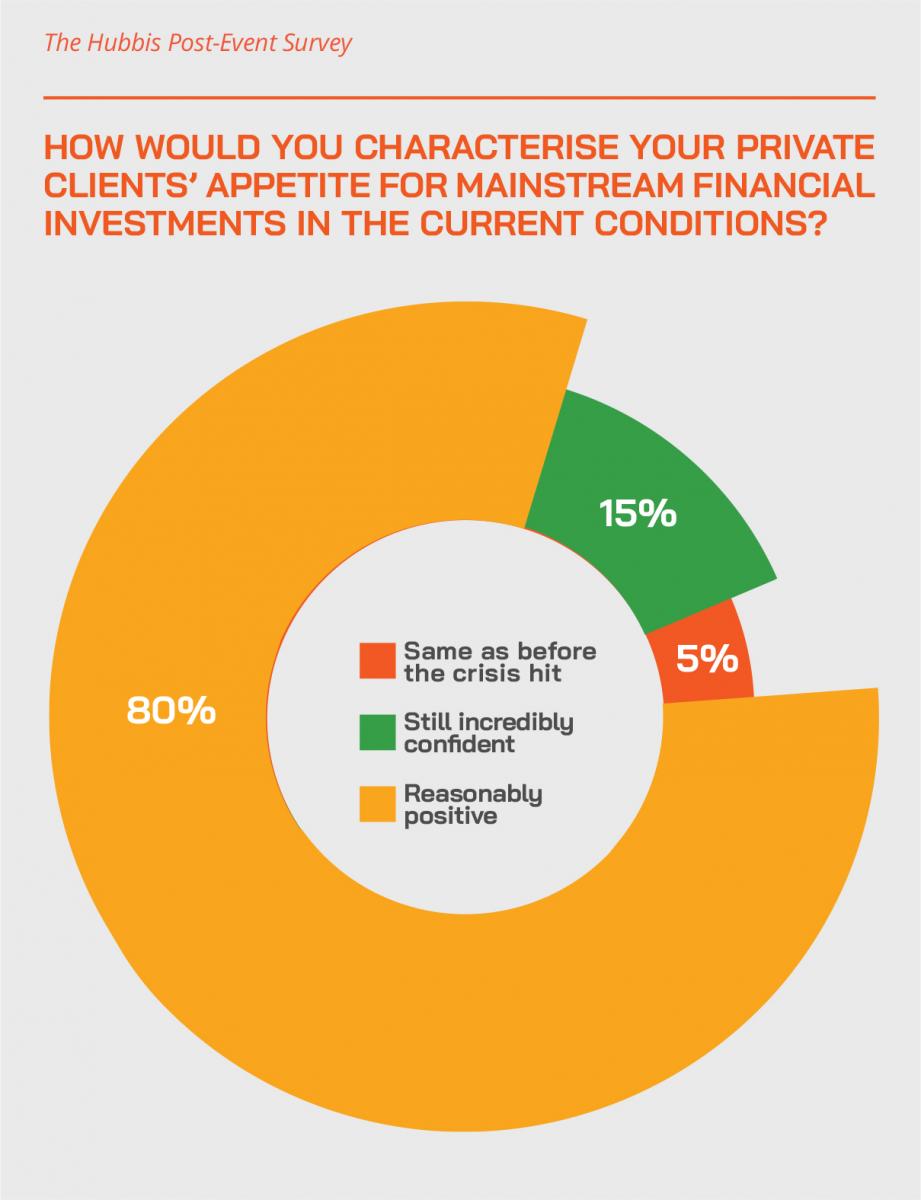

He also explained that the Indonesian markets had still not fully recovered from the very sharp Covid-19 induced collapse early in 2020, and as a large chunk of AUM domestically relates to equity investments, this meant customers are still wary over equities. “But with better news and the vaccination programme, we are on the right track forward,” he reported.

Keeping on top of clients and their portfolios

Another guest agreed that thus far in 2021 in Indonesia there is not any noticeable pick-up in either economic activity or indeed sentiment, although on a more positive note, there is some progress being made in terms of vaccinations and their rollout across the vast country.

“Accordingly, we are really emphasising the importance of the portfolio reviews with our clients, to make sure that they are properly diversified and well positioned in anticipation of the recovery in the wider economy once the vaccinations are well advanced and there is recovery also taking place across the world,” they explained. “Rebalancing, refocusing, and reshaping the portfolios are therefore key priorities for our interaction with clients today.”

Helping clients see the big picture and re-shape portfolios

Another central mission for the bank at this time is also to help clients understand the value of insurance for protection of the portfolios and also of the individuals in face of potential crises. “It is important that clients look more broadly at the whole picture than just investments, as insurance is remarkably important these days,” they explained. “And in a similar manner, we are also trying to encourage more forward planning for retirement, as it is well known in the country that there is a significant shortfall in pension planning here.”

As to the products themselves, they also reported that many clients need help overcoming some of the difficulties they might be facing in the current environment, so, for example, improving the yield on their portfolios if they need more cashflow. “And if they are concerned about their retirement plans, then we offer the right advice and solutions for that,” they elucidated. “It is really down to having the right conversations depending on what we identify as the client needs and expectations.”

Digitisation for connectivity and capability

Digitisation, another expert observed, is advancing apace in the country, offering customers greater capabilities in terms of remote onboarding, then managing their own transactions online or through smartphones or tablets, and with the banks and others able to deliver advice, research, and ideas remotely. Interactivity through some of the apps on offer allow clients to then engage remotely with their RMs, and to obtain more tailored advice based on their risk profiles, that are created for the RMs from customer information, thereby helping them tailor relevant conversations and ideas.

“And aside from the digitisation amongst the banks and major players, there are a lot of FinTechs offering their own platforms,” he added. “However, they are competing on low price, lower fees, and not offering advice really, or a wide range of products and services. The major players cannot follow that route; we have to focus on proper wealth management services, including access to the RMs. We want to combine the technology, the digital capability to transact, and the expertise and experience from the seasoned wealth management players in the industry.”

Building the digital connectivity

A senior banker agreed, remarking that the pandemic had, of course, significantly changed the dynamics of their own engagement with clients, and also naturally across the industry. “Specifically for Indonesia, we certainly have more digitally savvy clients today than for example in early 2020, but in reality, in the field of wealth management, most of our investors still really prefer face-to-face engagement,” they explained. “We have therefore been working hard to help improve the education of our clients as to how they can engage with us, how they can use our services and expertise, on investment products and insurance, on how they can adjust their portfolios, on how they can invest with us and so forth.”

Clients, this same expert reported, have had their eyes opened as to just how much can be achieved via the digital platform their banks offer, assuming they have grasped the digitisation nettle.

“And this is because we, for example, not only offer a very advanced platform, but we have also put a huge amount of effort into communication with our clients,” they explained. “Accordingly, we are doing everything we can to ensure they are educated in all of this, and so that they are fully aware of what can be achieved remotely. Indeed, as a result, we have seen a good shift of penetration and activity to the digital platform.”

Multi-channelling the solutions, personalising the offering

A digital solutions expert observed that more of their clients are working with them in a very collaborative manner to effectively build channel-based solutions. He explained that the channels might be direct to customer, such as a robo-style proposition that doesn't involve a relationship manager, or perhaps at the other end of the spectrum for high-touch, very personalised advice, targeted very personally at very affluent clients. He said that building this type of multi-channel flexibility is where a lot of the ‘smarter’ banks and wealth management players, including insurers, are differentiating themselves across Asia.

On top of that, he observed it becomes all about personalisation, which is a challenge on a country as vast and populous as Indonesia, so you can now use some technology that's already quite mature, like AI and ML, to help pinpoint the right piece of content in relation to the right customer, and then with the right call to action. “There is a lot that can be achieved in terms of personalisation,” he stated.

Driving the RM’s capability and freeing up their capacity

Additionally, the RM needs to be supported and empowered through digital solutions. “Often the RM has to log into seven different systems and piece together information, just to give a piece of advice to a customer, then they have to worry about the regulatory challenge of all that,” he reported. “We therefore help a lot of our customers bring all that together into a cohesive sort of environment to help make those RMs a lot more capable and efficient.”

That led him on to comment on client engagement as a driver for building AUM and revenues. “For our large global Swiss customers, the game and focus are often around productivity and efficiency to achieve growth within the existing customer base, but also by bringing on new customers. When you focus more on personalisation and better interaction digitally, these banks experience a much better situation for cross-selling.”

An ‘arms race’ towards digitisation and smart data

Another technology and data expert commented that digitalisation had moved on in leaps and bounds, becoming almost like an arms race for who can provide the most engaging technology solution to capture more client attention and interest, and thereby ultimately to capture more of the clients’ business and activities.

“We've seen a real demand from wealth customers in Indonesia and across Asia in trying to put more investment tools into the hands of their clients, whether those clients have an advisor or not because often clients I think like to do a little bit of their own work and little bit of their own research,” he explained. “But then they also have an advisor they can go to bounce ideas off or get a bit of help on something more complicated. And personalisation now is closer to the hyper-personalisation stage where information has to be very specific to the individual.”

To cater to these needs, there is a growing demand for global data and information, global investment ideas, global news, following markets and trends such as the rise of ESG, and in countries such as Malaysia and Indonesia, providing more data on Sharia-compliant information and investment ideas.

Expert Opinion - Samdarshi Sumit, President Director & CEO, PFI Mega Life Insurance: “The rise of digitalisation has led to significant increase in the number of new opening of Mutual Fund accounts in Indonesia, with almost 80% increase in 2020 alone – based on data from Indonesia Central Securities Depository (KSEI) . This new trend has changed the investment landscape in Indonesia, with selling agents accelerating their digitalization journey and expediting online offering. Bank Commonwealth is one of the first to embrace wealth management digitalization in Indonesia through CommBank SmartWealth.”

Convergence between advisors and investors

He also observed the interesting phenomenon of greater convergence between the advisor and the investor. “This is to a large extent driven by technology, but also by information, as private investors can get access to information and tools that 10 years ago, they wouldn't have dreamt of,” he explained. “It makes life difficult for the advisor to stay a step ahead and add value, but I think they can do that through bringing new products and new services into the market, as well as demonstrating their duty of care really to help the investor understand what their objectives are and how they might differ from other investors.”

Insurance – growth for protection and investment

A panellist took up the baton of insurance that a fellow panellist had alluded to earlier. “For insurance companies, this is a challenging time, because the pandemic directly impacts the claim books, and in the mass segments there is some attrition, people not paying their renewal premiums and other challenges because of the impact on the economy of the pandemic,” he reported.

“But,” he added, “we do really strongly feel that it's a great time for us from a longer-term perspective, because more people are seeing how protection plays out and is increasingly a critical part of the wealth planning, as these ideas sit well with customers in difficult times like this. Accordingly, the pure protection element of our book is growing reasonably well.”

Tailoring the right unit-linked insurance – a major opportunity

As to investment-led insurance or the unit-linked insurance propositions, he said that as the Jakarta Composite Index has been a weak performer, clients are keener on products with an underlying offshore opportunity.

He reported that they had launched an investment-led insurance product on an underlying asset pool of some USD1.5 trillion, creating a feeder fund off that and which helped them grow their assets more than 30%. “That is a great achievement,” he said. “The drop in the regular onshore products has been offset by a much stronger growth in this segment.”

Expert Opinion - Samdarshi Sumit, President Director & CEO, PFI Mega Life Insurance: “The digital platform is critical for insurance awareness and education as young customers would like to understand and study about product and proposition on their own before meeting an advisor. They also prefer to start their insurance journey through smaller and simpler products.”

“The pandemic poses challenges for the insurance industry, but this is also a great opportunity for insurers to live out their real purpose. Near and dear ones and advisors of those affected today value the importance of protection products and life insurance even more than ever before.”

A major challenge for everyone today – identifying and winning new clients

Across the wealth industry, one major challenge since the pandemic hit has been identifying and converting potential new clients. A banker reported that their bank had been very active through social media and has an acquisition team, specialists who are well versed in wealth management and who can follow up on leads.

“We have been successful in these endeavours,” they explained, “and have been growing our AUM despite the headwinds, which is not easy to do in this situation. It boils down to finding the right prospects, then engaging with the right conversations, and offering the right product proposition to help them identify and overcome the challenges they face in terms of investments and wealth planning. So, we make sure the acquisition team is fully up to date on how they should approach such people and what they should offer them and why.”

Looking to the future – educating the RMs and clients

A banker then declined the opportunity of reporting on their exact AUM number for their private bank in Indonesia itself, but they confirmed that it had been growing at a reasonably satisfactory pace.

“We have focused intently on building the customer base amongst people whom we term ‘new-to-wealth’ who can thereby join our priority banking clientele,” they explained. “Additionally, we have been intent on winning over more of the share of wallet of our active clients, and further building on those established relationships. Accordingly, all of the conversations, all of the product propositions, all of the portfolio review discussions, our campaigns, the education effort we make with our customers, and our RM education and training, all these contribute to these drives, and the results are really showing through.”

Expert Opinion - Ivan Kusuma, Senior Vice President, Investment & Liabilities Dept Head, Commonwealth Bank: “With registered number of investors in Indonesia at around 1.5% from population, focus on the stakeholders will be financial education series to help improving financial literacy. Social media has been widely used to boost education for wider audience.”

Putting things in context – retirement issues to focus the minds and hearts

Expanding on the issue of client education, they observed that discussions around retirement planning are ideal for capturing the attention of these individuals, aiming to offer them a different perspective from the normal mindset of building or buying their houses, their children’s’ education, healthcare and so forth.

“Retirement and legacy planning discussions help focus their minds on the future and provide an ideal context for discussions on investments, insurance and general estate planning,” this expert reported. “And as data shows that less than 10% of Indonesians are organised properly for retirement, there is immense opportunity. With plenty of evidence that lifestyles fall for most people when they retire, we also educate our RMs to help them manage these discussions and propose the right solutions and products.”

Helping RMs and advisors drive their conversations around the future

They elaborated on these comments, explaining that the bank has been offering online training and webinars for clients, as well as classes for the RMs to help them manage the conversations, handle the client objections, in fact to handle all forms of their communication. “We aim to make all this as interesting and pleasant as we possibly can for the clients and the RMs,” she concludes. “We need something that is a little ‘jolly’ at this time of considerable concern for so many people.”

Another banker offered their views on the subject of education and training, explaining that most of that centres on existing customers, offering them regular market updates, offering them insights into alternative investments and newer ideas, such as for example bancassurance, and estate and legacy planning. And to build new customers, social media is central to this effort.

Looking to the future – and that future is young

“If we look at the demographics of our investors, based on the data that we take from the Central Depository in Indonesia, almost 40% are actually below 30 years old. “We try to support with a wider variety of options and ideas for them, with infographics and short videos, sometimes collaborating with key opinion leaders, working with actors to help get the attention from these customers,” he reported.

With these younger demographics as background, the final comment went to a digital solutions expert who reported that from what he has been seeing in more advanced markets in the region, there is a powerful shift to open banking.

Expert Opinion - Ivan Kusuma, Senior Vice President, Investment & Liabilities Dept Head, Commonwealth Bank: “Newcomer FinTech companies usually come with similar proposition: lower transaction fees while established Wealth Management providers can provide affordable fees and excel in value added advisory solutions from experienced Wealth Advisors.”

“Singapore has only just switched on open banking for wealth and insurance products, and I believe that will lead to other regulators following suit in other markets,” he explained. “Open banking is a super exciting proposition such that you can automatically have a holistic view of your customer straightaway and see their total wealth and total protection, thereby helping you to find the right solutions for them. We have also been injecting behavioural science and decision theory into some of our customer projects to make that experience a lot more fun and engaging.”

“Agreed,” concluded another expert, “we are seeing massive demand for value added content. On the educational side, we've got some great videos that people like to watch to help them learn on choosing investment theme, whether on ESG or Sharia-compliant products, and so forth. It is about connecting investors to their advisors in their specific markets.”

And with a young, fast-growing and tech-savvy population and an economy that the OECD currently reported should soon resume growth at around 5% annually (presuming the vaccination programme and other measures are effective), the potential for the wealth market in Indonesia is enormous. Those who best position themselves during this time, will surely reap the rewards in the years ahead, especially if, as had been projected, Indonesia will be within the top five largest economies in the world by 2050.