Publications & Thought Leadership

The Growing Universe of Digital Assets – Are they Relevant to Asia\'s Private Wealth Clients?

Mar 2, 2021

The archetypal retired private banker in Asia would perhaps be seeing red over any suggestion that one of his or her wealthy private clients should today be investing in cryptocurrencies or other forms of digital assets, for example, stable coins or token offerings. But the digital asset industry is rapidly moving mainstream, with specialist trading, execution and digital asset custody firms rising up and also becoming recognised and regulated by leading authorities in many key jurisdictions, thereby lending the industry an ever more visible air of legitimacy. In the Hubbis Digital Dialogue of February 25, a panel of experts looked beneath the hood of the nascent global digital assets market to look at the evolution and diversification, even proliferation, of the digital assets themselves, at the evolution of regulation in this \'virtual\' world, and at the development of increasingly professional market infrastructure and a more diverse ecosystem.

Panellists:

- Henri Arslanian, FinTech & Crypto Leader, Asia, PwC

- James Quinn, Managing Director, Q9 Capital

- Joshua Foo, Regional Director of the ASEAN Region, Chainalysis

- Steve Knabl, Chief Operating Officer & Managing Partner, Swiss-Asia Financial Services

While it is still early days in the expansion of the universe of cryptocurrencies and indeed of other forms of digital assets – for example, digitised tokens representing businesses, shares, real estate, wine collections and more - the increased awareness around the world, the increasing uptake amongst investors, improving understanding, better regulation, a more professional type of infrastructure and better guidance are all combining to build a more robust platform for the market's expansion in the years ahead. And all these elements are, of course, turbocharged by investors seeing the incredible performance of Bitcoin in recent months as it has recovered its momentum and surged past all-time highs, even if it has fallen back somewhat in recent days.

In the February 25 discussion, our panel of experts addressed many questions. How do cryptocurrencies work, and what relationship do they have to blockchain or other confirmatory protocols? What are their investment characteristics? What are stable coins? What are the initial coin offerings? What other forms of digitised assets are already in existence, and what is likely to emerge in the foreseeable future? Which investors from which regions have been driving the remarkable performance of Bitcoin in recent months, as it has surged to new all-time highs after a year or two in the doldrums? Why are investors flooding into Bitcoin and some other cryptos such as Ethereum? Are cryptos seen as a hedge against economic meltdown and financial chaos in the fiat currency universe or as a hedge against the spectre of rampant inflation?

And how are investors buying into digital assets – through specialist intermediaries, through brokers, through exchanges, through funds? How are digital asset brokerages evolving, and are they being properly regulated, are they secure, and are they achieving the growth they expected? How do the institutional-grade offline ('cold') and online ('warm') custody/storage solutions for digital assets work and who is providing these services and why? Will the mainstream private banks and leading independent wealth management firms increasingly promote digital assets to their private clients?

And specifically, for the world of Hubbis readers and clients, will more wealthy Asian private clients buy into the digital asset markets, and if so, why and how? What should be a typical portfolio allocation? And what next for digitised assets, and will they make a major contribution to transactions across many more types of assets, for example, from real estate to collectable art?

An expert opened the discussion by remarking how although there had been so much talk of digital currencies and digital assets in recent year, mainstream wealth managers shied away from them. But in recent times, there had been a more mainstream interest, and some of the innovative companies such as Tesla had entered the fray buying Bitcoin very publicly. He observed that so many investors still struggle with the concept, and therefore that the wealth industry had to ensure they have the sophistication to understand this market and its nuances in order to offer appropriate levels of advice.

True diversification

“For true diversification, you need a slice of all asset classes, whether real estate, commodities, precious metals, equities, bonds and now cryptocurrencies and other digital assets are becoming an asset class of their own, and there are nowadays many ways by which to invest, whether through funds, ETFs, structured products, or even via private equity and venture capital investments.”

Another guest remarked that education is vital, and there are numerous YouTube and other videos explaining how Bitcoin works, what the blockchain is, and so forth. He said he often tells people to begin by buying a small amount of Bitcoin, experiment, learn more, and gradually become much more familiar with how they work and their price movements.

Expert Opinion - Steve Knabl, Chief Operating Officer & Managing Partner, Swiss-Asia Financial Services: “Digital Assets are a key diversifier in a portfolio and hence has a place in all portfolios. The only major issue is to choose the right manager and ensure that you understand the risks – both investment risks and security.”

Expert Opinion - Joshua Foo, Regional Director of the ASEAN Region, Chainalysis: “Our firm is committed to building trust in blockchains and ensuring a safe ecosystem for all investors. As cryptocurrency continues to see widespread adoption, the company will continue to provide top-of-the-line compliance and investigatory solutions to emerging markets, businesses and regulators.”

Expert Opinion - James Quinn, Managing Director, Q9 Capital: "When making your first steps into crypto - start simple. We have found that, once onboarded, 80% of our new clients buy Bitcoin in spot as their first investment. They want to understand how it all works: wallet management, the systems, how the asset works. With Q9, we actually do all the wallet and key management. Then after that our clients start to look at other assets like Ethereum. I’m actually surprised just how quickly our clients get up to speed and start investing in other coins.”

Demystifying digital assets

He explained that the crypto ecosystem comprises somewhere north of 8000 different coins in the market, and the total valuation is over USD1.5 trillion, with Bitcoin accounting for roughly two-thirds of that total. He remarked that it is important to understand Bitcoin was created on Halloween in 2008, six weeks after the crash of Lehman Brothers, and it solved one very simple problem - it allowed two parties to present value to each other without any traditional intermediary and with absolute certainty of exchange and no 'double spend' or possible replication.

“The market has evolved dramatically since then,” he reported, “The main reason we see activity is often for portfolio diversification, especially in the era of quantitative easing, where there's the risk of hyperinflation and potentially of currency devaluation. As part of a diversified portfolio, Bitcoin and other cryptocurrencies can often play a role these days.”

Taking the first steps

He explained the other question that comes up is how to invest, observing that the industry is in its infancy, much like the world of hedge funds, venture capital and private equity were several decades ago. “To put things in perspective today, only in crypto hedge funds, leaving aside crypto VC funds, passive crypto funds, and some of the other products, the total AUM according to our last annual crypto hedge fund report is around USD2 billion of AUM only. And the median ticket, by the way, in these hedge funds is around USD200,000. In short, it's a lot of high net worth tickets and family office tickets coming into this space.” But with massive potential for growth.

He explained that there are many other ways to invest, however, with specialist platforms such as the Q9 platform, sponsor of the event. “These new and sophisticated platforms enable investors to access the digital assets ecosystem in a way that is user friendly, with all the usual facilities included, including simple buying and selling, monthly statements and so forth,” he said.

Mirroring mainstream finance

Another expert agreed, commenting that the Q9 platform provides a platform for a variety of digital asset investments, much in the same manner as a traditional premium broker. He explained investors could trade, switching easily between fiat and cryptos and vice versa, or crypto to crypto; they can store, custody, and even earn interest on their digital assets or cryptocurrencies. A big target market is the substantial individual private wealth, including family offices and wealth managers who want to offer relevant access to their private wealth clients.

Building the comfort factor

He explained that some 80% of clients trade in Bitcoin as the first thing they do in this space and build from there. This helps them understand how it all works, how the 'wallet' systems work, how the 'smart keys' work and so forth. “And then when they become comfortable, they might move to Ethereum or other assets,” he reported. “Honestly, I've been pretty surprised about how quickly they can get up to speed and start asking about what I consider pretty alternative coins or different types of assets or types of digital assets in which to invest.”

He explained that spot market investing in cryptos is therefore easy these days. “They buyers hold their digital bearer assets on the platform, but from their customer experience standpoint, it is simply like opening a brokerage account and buying stocks; it doesn't feel too much different, and we just try to take the best of what's been developed in that space and make it really easy for our clients to start investing in this space,” he reported.

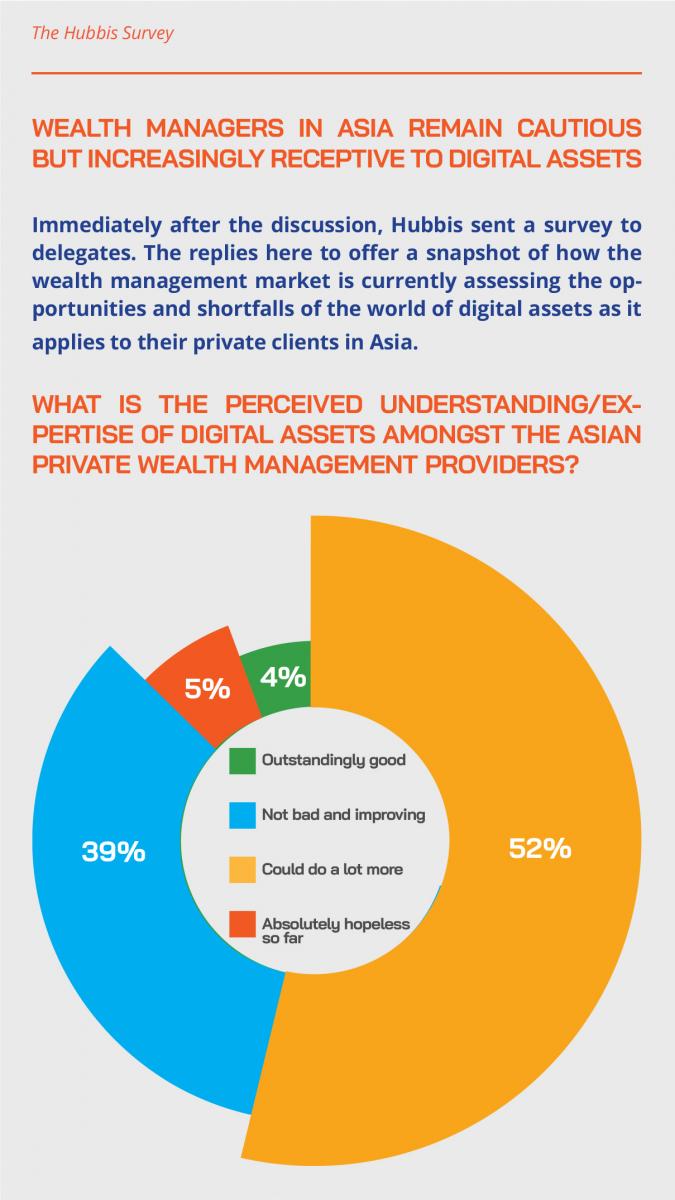

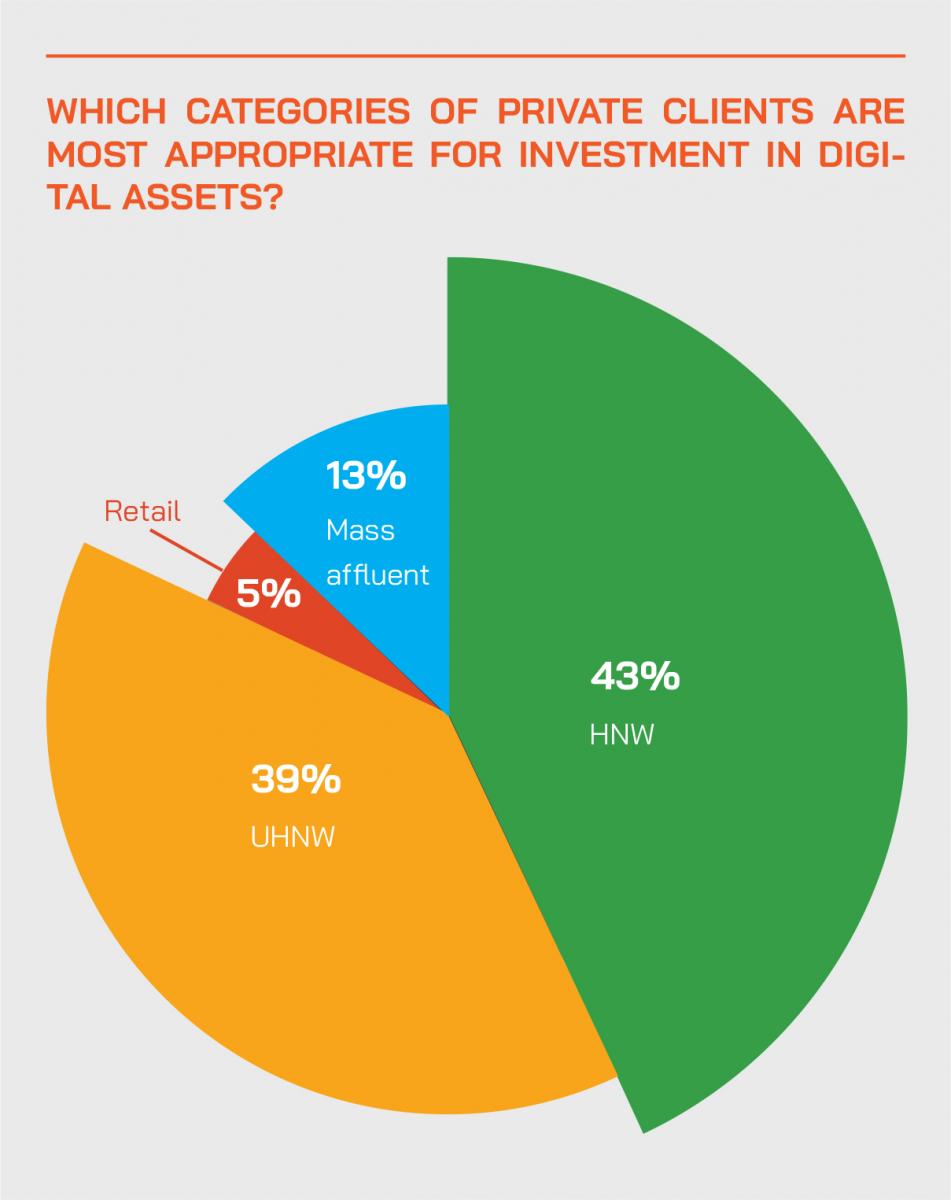

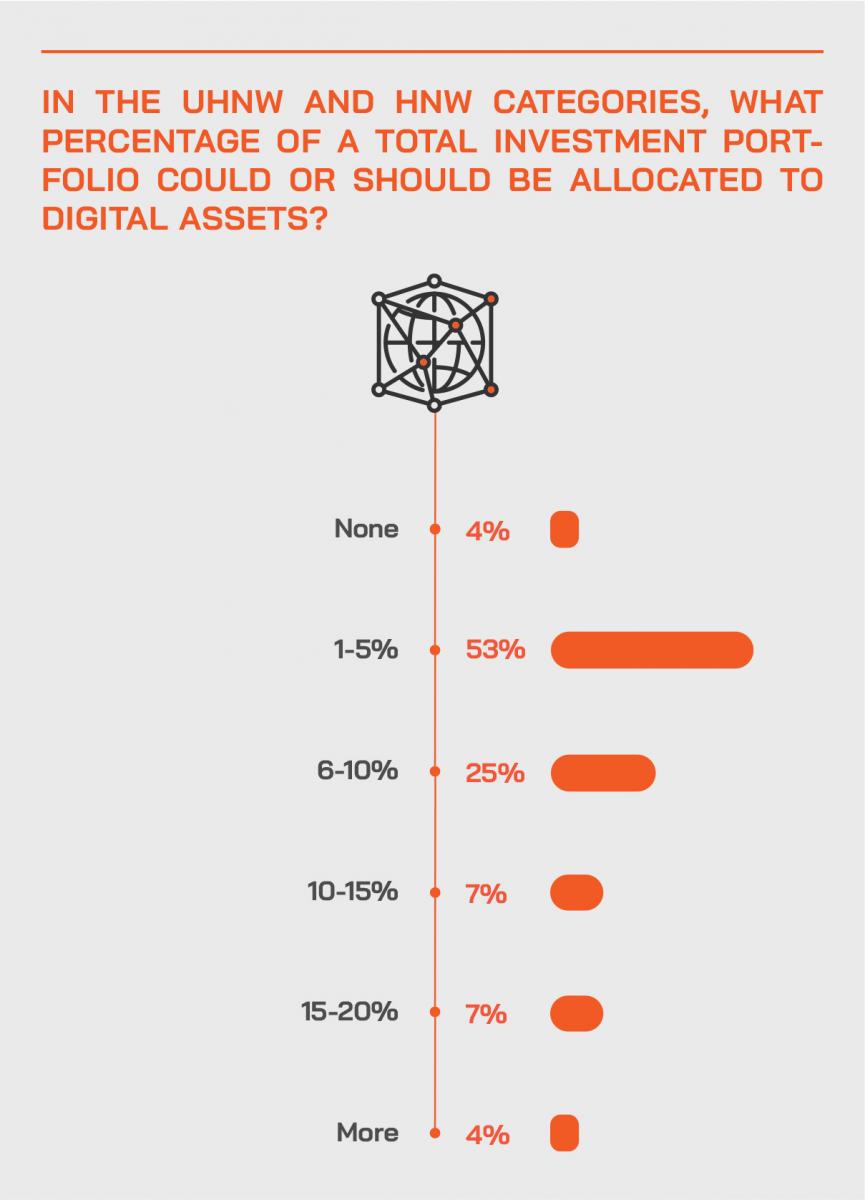

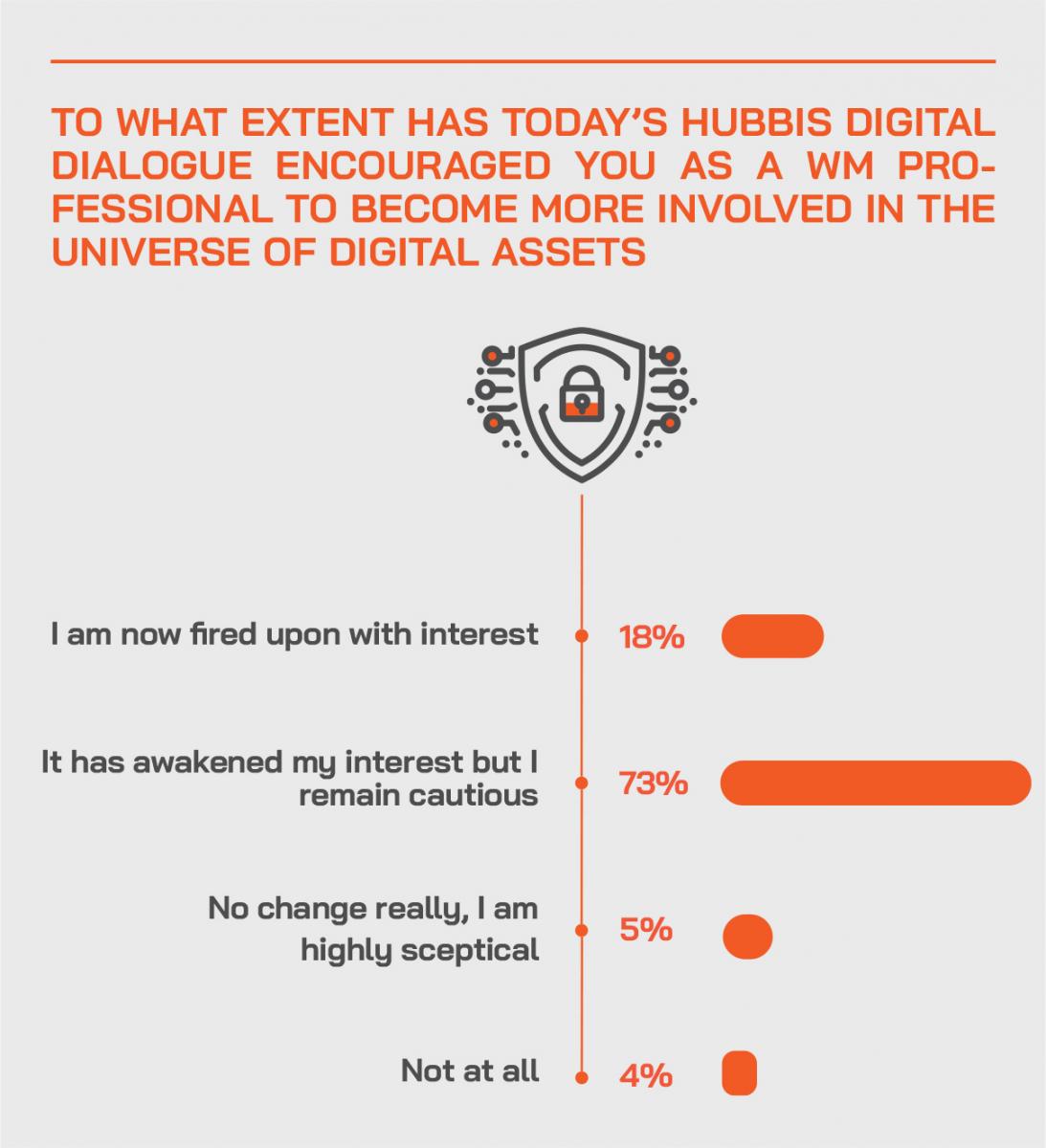

The Hubbis Post-Event Survey

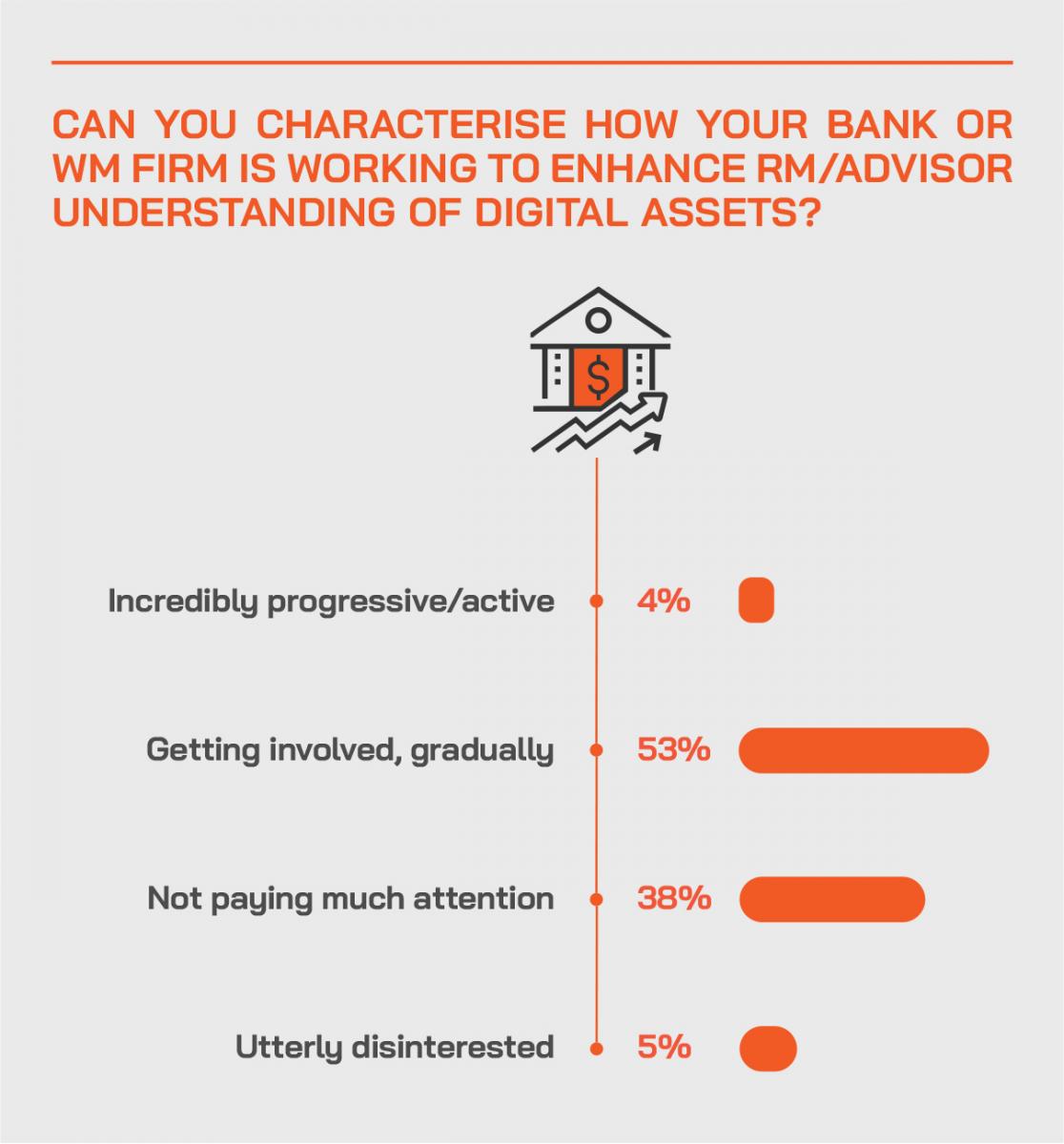

Immediately after the event, Hubbis sent out a survey asking delegates to offer their views privately and off the record as to their views on the development of digital assets and investing amongst Asia's private wealth clients. This straw poll indicates clearly that the industry is far from embracing these assets, with comfortably 80% or more saying no to this question:

Hubbis: Has your bank or WM firm been promoting digital assets with your private clients? Why or why not?

The 'No' replies were in the great majority. In brief, they gave the following reasons:

- Lack of effective, comprehensive regulation.

- Too early.

- No direct access.

- Top management not yet considering.

- No expertise in-house and therefore we cannot offer effective advice.

- Not yet, we are awaiting approval from the Monetary Authority of Singapore.

- Still not convinced about valuations and fundamentals.

- We do not have the necessary license.

- Highly volatile and a limited asset class.

- In-house compliance restrictions.

- Too risky.

- Not preparing for this from our platform; it's not a good service for our HNW clients for our firm as an EAM to provide.

- No, the bank in general, looks at digital assets in a negative light and indicates this should never be discussed with clients out in the open. It is increasingly difficult to justify or to get an account approved, since crypto easily now makes anyone's partial or even full SOW at the account opening stage. At the WM firm, as partners to our clients in an advisory role, anything under the sun is up for discussion, which keeps the relationship in perspective and interesting in relation to investing.

- Our view is that buying Bitcoin and others remains more speculation than investing.

- There is no legal guideline for promoting digital assets to clients.

- Unfortunately, not yet. I am on the constant lookout for colleagues in the sector who have the heavily coveted regulatory licenses to help us truly take advantage of and promote Digital Assets.

- Not yet - the bank is reviewing it as there is still no proper regulatory framework for digital assets.

- We have little knowledge of the valuation of digital assets.

- No confidence or expertise

- Primarily no, because we see digital assets at the very initial stages of their development.

However, there were also some 'Yes' replies, for example:

- Yes, for diversification.

- Yes, but not quite yet. We have been active in looking at this 'asset class', to invest via funds or ETFs.

- It is not essential, but a conversation with the client on these topics helps not only in deepening the relationship, but it shows we are relevant, forward-looking and open-minded to explore 'alternatives'.

- Yes, based on demand, but we need credible service partners to work with.

- Yes, digital Assets are the future, and the market trend is clear. In order to advance and move forward, one has to keep abreast with the trends.

- Yes, digital assets have grown so much that it is very difficult to totally ignore this market.

- Yes, as when Tesla hints at car purchases with Bitcoin, the idea seems to be far less farfetched.

What are the key hurdles to overcome for your bank or WM firm to guide private clients effectively in the universe of digital assets?

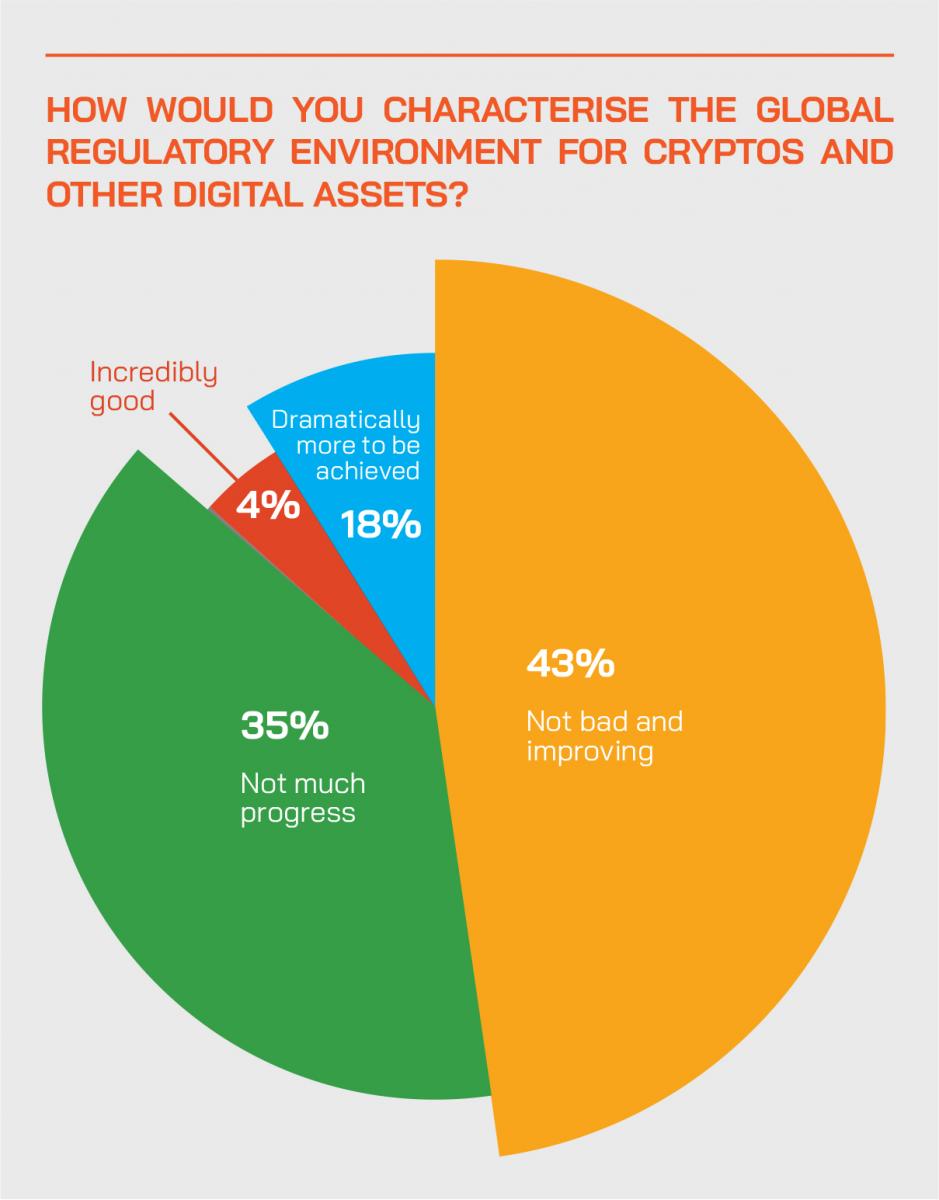

- Poor or inconsistent regulations that are more local than global.

- Lack of client willingness to invest in these asset classes, no track record in which to form rational decisions.

- The first step is to clear compliance. We are not comfortable to accept clients that derive their wealth through cryptocurrencies. We need to be able to evaluate the day to day change in values.

- More client demand needed.

- Lack of experience, lack of systems, lack of effective monitoring as they are not authorised products at our bank.

- Lack of know-how and infrastructure.

- The panellists hit the nail right on the head; it is all about education.

- We are not sure of the credibility of the assets, their value and safe storage.

- Not for us, most of our HNW client are in their 60s and older and do not warm to these assets; they want to protect wealth.

- We are restricted by the lack of a house view.

- Basically the non-acceptance of cryptocurrencies on a general level by the banks is due to it being tough to gain client acceptance, especially if the clients are first or second generations or are traditional business owners. These clients usually have high trusts placed in their banks and notably takes the advice of their bankers on traditional assets far more willingly.

- This is rather new and unfamiliar with it. Also, the infrastructure does not appear robust at this point.

- It is not simply a key hurdle we need to overcome. We will need to build infrastructure from the ground up should the leaders of the banks and WM firms be interested in these digital assets. At this point. We are ill-equipped to guide our clients in this universe and need vast amounts of time and resources to compensate.

- We need a better regulatory environment for investors to be more willing to accept this new asset class. Generally, investors shun away because they lack understanding and technology expertise, hence, so they will not risk investing if they have little knowledge. To promote the market, education of the technological aspects and communication of the benefits and how to access online are key areas to build up. Clients need to be educated and feel comfortable on the risk and rewards so they are fully prepared the way to go forward on the benefits of investing in the universe of digital assets.

- The market requires better transparency on pricing mechanisms and liquidity in the trading platform. A longer track record and much clearer regulations required.

Do you believe that digital assets will become more mainstream and institutionalised and why or why not?

- Yes, with the growing affluence of younger investors.

- For the new generation of clients this maybe an increase of interest in digital assets.

- Although digital assets are gaining in popularity, as long as it is not properly regulated, it is too risky.

- Absolutely, because traditional market discipline has been distorted by arbitrary intervention by central banks since 2008.

- Probably yes, due to the continuing obsession with technology.

- Yes, simply due to growing demand from institutional and retail investors. Wealth managers

- either adapt or miss out on the business.

- Yes, I believe so as digital assets is just a part of the bigger digital evolution process.

- Yes, simply because they are becoming highly publicised so client demand/interest will naturally increase.

- Yes although it might evolve to a different form from currently available. With regulated activities in digital assets increasing, clients and institutions will become more comfortable in dealing with digital assets.

- I feel that it will. Both my young adult children are lawyers, a litigator and a corporate lawyer specialising in digital, payment systems and financial regulations, and flooded with work!

- Digital currencies can become mainstream only for transactions but may not be a store value as there is no logic as to intrinsic value.

- Yes, they will become more mainstream. Lots of innovation coming through will help the process.

- Yes, classic disruption to inefficient processes.

- Yes, due to the rise in the level of sophistication in the digital asset industry that has run in parallel with the increase in institutional participation. Digitisation is now fully underway, and accelerating.

- Financial instruments will become fully digitised. Digital assets are increasingly being adopted by investors globally.

- Yes, gradually. Even our governmental agencies are encouraging the use of digital platforms for payments. One good example is the e-Ang Pows [seasonal monetary gifts] for our Chinese New Year!

- Yes. Not only is there a great deal of interest and “hype” not only within the industry but the general public as well. Furthermore, we can see a lot of exchanges figuring out ways to make digital assets more regulated. Even if they have yet to succeed, regulators will likely sort out the nuances shortly due to increasing demand.

- Digital Assets will become more mainstream and institutionalised in tomorrow's digital world. This can be improved and executed with blockchain technology, a way of structuring data that increases security, ensures traceability and decentralise the control of assets/shares. In particular, in the case of digital assets, a lot of work is going into tokenisation, a process within blockchain that allows an asset to be replaced by a code. It is more secured and hassle-free.

- Tokenisation is a new approach. Digital assets use a central entity that brings confidence. Digital assets are tokenised assets and can be handled in a distributed or decentralised way, improving efficiency and speed; they are cost-efficient and offer a good user experience. For sustainability-related markets, it would make a lot of sense to use tokenised digital assets in this space. Tokenised money will help eliminate money laundering and terrorist financing.

If your bank/firm has been promoting investment in cryptos, which names are most in favour/demand?

Few answers here extended beyond Bitcoin. Some replies mentioned Ethereum.

The digital footprint

Another guest explained that his firm is involved in countering the potential for digital assets to be used for illegal purposes, such as money laundering or terrorism funding.

“You can send these funds entirely remotely,” he explained, “and there is a significant level of pseudonymity to it. However, the reality is that with digital currency, every transaction has a digital footprint, and as a company, we analyse those digital footprints, and we are able to provide information to law enforcement, to regulators, to service providers like Q9, providing data on where these funds coming from, and the destinations. We've been very successful in helping the Department of Justice in the US and Interpol and Europol to actually catch criminals and seize these digital assets and thereby prevent such illicit activities.”

Expert Opinion - Joshua Foo, Regional Director of the ASEAN Region, Chainalysis: “The power of blockchain brings about a level of transparency and traceability that is not seen in traditional fiat currencies. We at Chainalysis are working tirelessly to educate both the public and private sector so they can make informed decisions regarding digital assets as the technology becomes ever more integrated into our daily lives.”

Expert Opinion - Steve Knabl, Chief Operating Officer & Managing Partner, Swiss-Asia Financial Services: “Many people only see the speculative aspect of the Digital Currencies and typically don't understand how the technology functions and what the case usage of the technology is.”

An expert commented that there is growing diversity in the universe of assets. He explained that Stablecoin, for example, is backed by fiat money, and therefore considerably less volatile than Bitcoin and others. “Moreover, Stablecoin, because it's backed by fiat money, can be easily used for transactions,” he said. “A year ago, there was the equivalent of USD5 billion of them, and today about USD45 billion, and we are seeing more and more people not only using it in retail transactions but also commercial transactions now, essentially for payments. And due to excellent traceability nowadays, the total amounts of funds coming from illicit purposes is incredibly low, less than 0.34% according to Chainalysis.”

Far from a token market

He reported that another area of strong interest in the growth of security tokens, which are digital representations of physical assets, for example, real estate, where a significant new development or property anywhere in the world can be split numerous times into security tokens, which have potential liquidity and can be offered to investors worldwide, in slices that suit their portfolios.

“The beauty of one of these assets is they are blockchain-based,” he explained, “and that means you know precisely who the shareholders are, and you can, for example, payout dividends easily and far more regularly, in theory daily, even hourly, based on the underlying cash flows of the asset.”

The other category is the central bank digital currency or CBDC, he reported, that he reported is equivalent to actual fiat money. “According to the Bank for International Settlements, 86% of central banks are looking at the topic including many central banks such as in Singapore, Hong Kong, the UK and so forth. This is not necessarily a key investment for WM clients but important to understand as part of the universe of digital assets. There are other digital assets emerging in the future, but for today, I think we are covering enough here.”

Many avenues available

An expert tackled the ways in which to invest, explaining that investing in spot results in holding digital bearer assets, or perhaps in funds, similar to the mainstream financial market funds, although with management fees that tend to be a little bit higher than they are like in traditional finance, because the digital space is still developing.

“You could invest into an actively managed fund as an example, which is maybe not taking a direct exposure or beta or delta exposure directly into certain cryptocurrencies, but has other strategies, and there are some great opportunities in such actively managed funds. But part and parcel of what investors are seeking is some delta or beta exposure to cryptocurrencies, and also to learn how they work now because the market is growing so quickly. You want to really start learning now, even if you're making only that first small investment.”

Expert Opinion - James Quinn, Managing Director, Q9 Capital: “There are many ways to get exposure to digital assets. This can be done by buying spot, or you can invest in derivatives such as perpetual contracts. You can also invest via a fund – but often have to pay a premium and management fees this way. The space has changed a lot in the last couple of years and the infrastructure today has been designed specifically for institutional investors.”

Platforms for choice

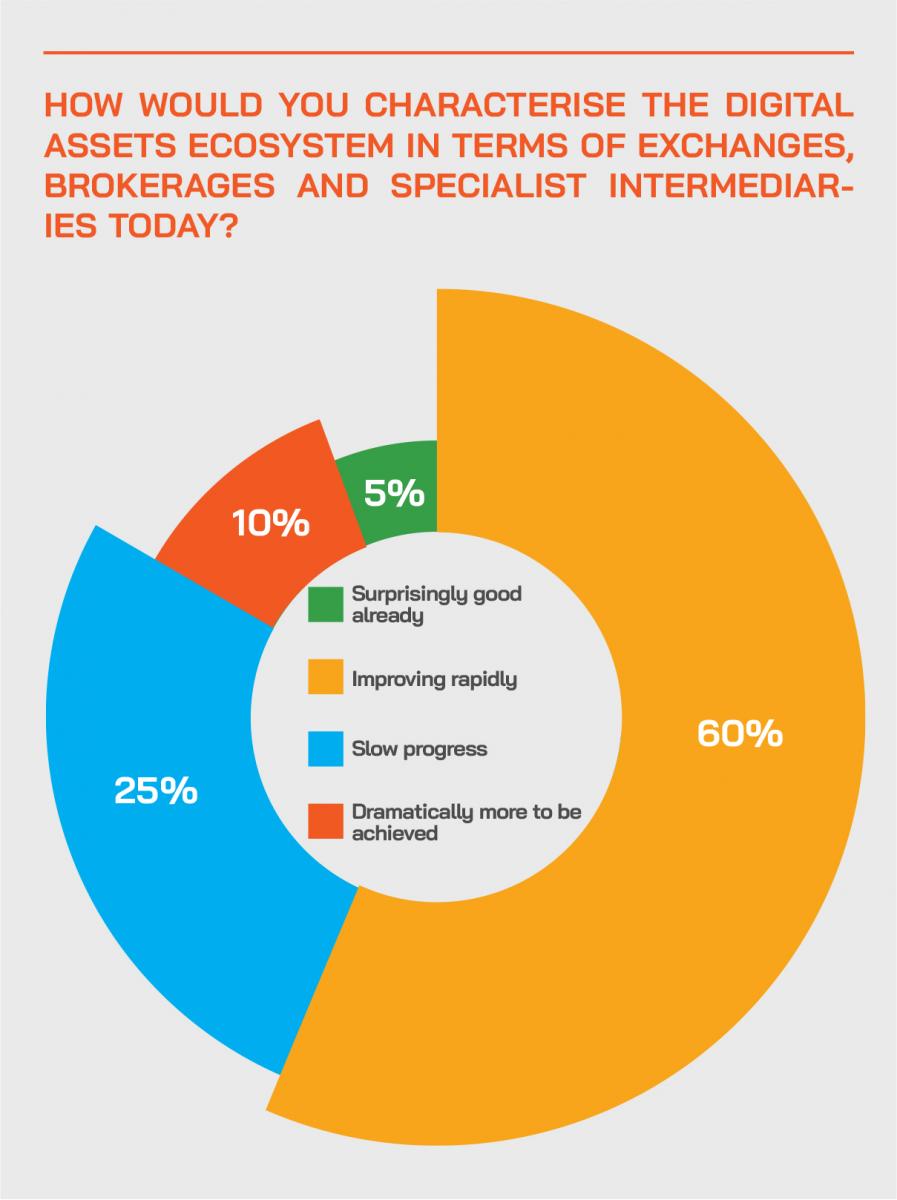

He added that the digital assets space had changed so much in the last couple of years, with all the key platforms that offer direct access very sophisticated nowadays and increasingly geared for different types of clients. Some platforms are for retail investors, with interesting products and easy access; some are more for the institutions, some of which are very active traders, with dedicated crypto specialists in-house.

“We sit in the very large space between those types of investors,” he reported, “focusing on young professionals, the mass affluent and right up to UHNWIs and family offices. They want some hands-on relationship management; they like to be able to call somebody when they have an issue, they don't want an email saying someone will contact them within 48 hours, as they might be advised if working through a retail platform. They want a really safe environment, and a really good user experience, which is precisely what we offer them.”

RMs on hand

He explained his platform provides access to several different products, including lending back the Bitcoin in which an investor invests and earning some interest from that process. “They quickly learn how fiat to crypto onramp works, they see the digital wallet in our system; they see they do not need to do anything, but become comfortable with the workings. They have a relationship manager who can handle details, answer queries, and improve the comfort of the whole process. It becomes familiar. For these clients, we offer the right type of platform for their needs and expectations.”

He explained that a number of the other platforms serving other segments of the market are also high quality. “The derivatives market has grown tenfold in recent months, driven by the big institutions but also by retail demand,” he noted, adding that the whole infrastructure and ecosystem is really expanding apace.

Skin in the game

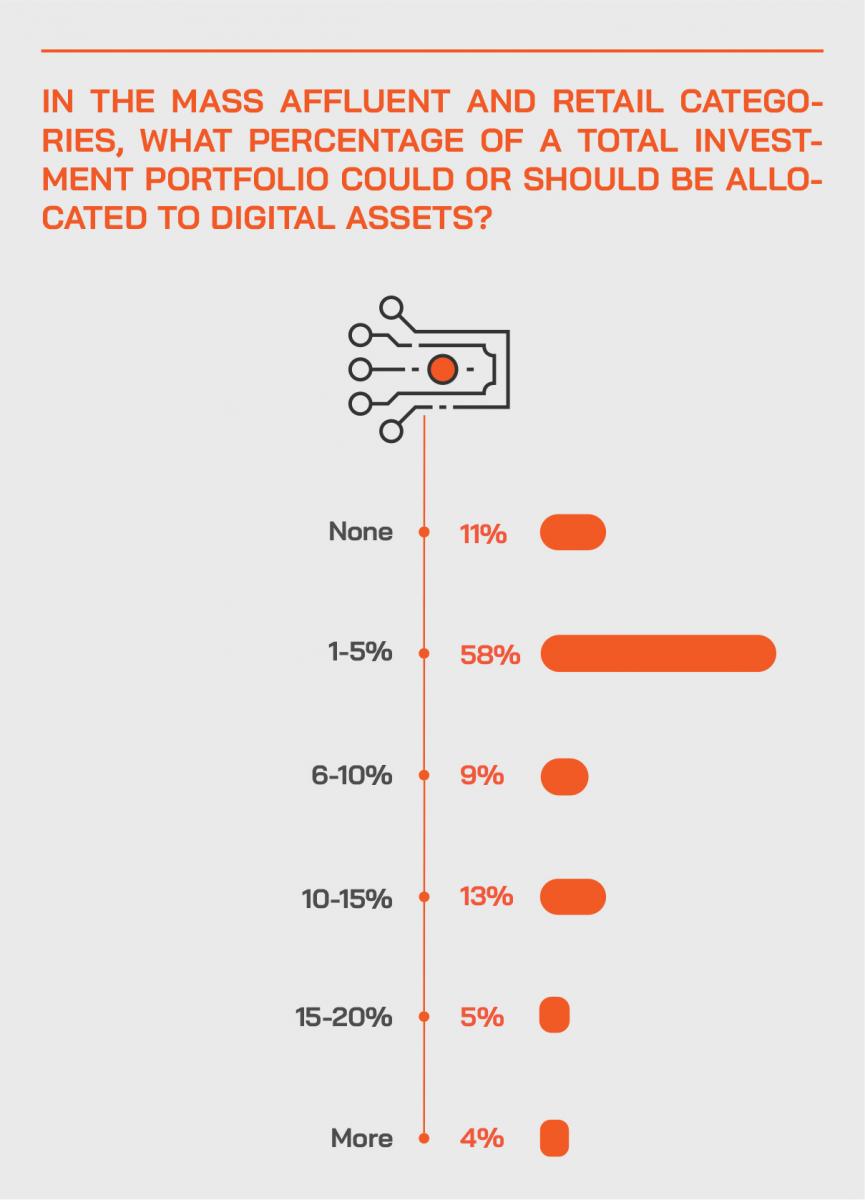

He explained that his firm does not offer advice, but if any guidance is offered, it is usually to suggest to the clients that they slow down. “They tend to become comfortable so fast, as this space has improved massively in terms of the simplicity of the client experience and people's understanding,” he reported. “Some get aggressive very quickly, depending on their risk appetite, but most settle in the 3% to 5% of allocation range. Generally, they start making the allocation that they are ok to lose. They always seem to find themselves better off for having done something than having done nothing. I haven't really found anybody that said it was a waste of time. They have skin in the game, they are educating themselves, and they can scale up if that suits them to do so.”

Get involved

Another expert commented that this is an asset class that needs to be understood by wealth managers and promoted to their clients. “If you think you've missed the train, you're going to keep missing it, because this is an industry that's moving very, very fast. Yes, Bitcoin or others can lose 50% overnight, but they can also rise and keep rising, as seen in recent months,” he said. “So, get into it within the risk appetite that your clients want; that's what I always say. Get into a fund that is maybe market neutral, like you would get into a long-short equity fund that is market neutral if that's your risk appetite, but get into it because it is de-correlated to the market. You want more assets that generate alpha in the portfolio and that are not correlated to each other. That is diversifying your portfolio. As a wealth manager, you're supposed to be offering what there is out there. And if you don't offer it to your clients, they're going to go somewhere else. If you're having problems understanding it, then take the time to understand it.”

An improving reputation

Addressing security and reputational issues, another expert reinforced the message that the blockchain provides a digital trail that, in fact, makes AML and anti-terrorism funding monitoring and policing on a global scale considerably easier than tracking cash, for example.

“My personal belief is that actually as the industry is becoming more regulated,” came another view, “and as we see central bank digital currencies come in, I think you'll see the roles of assets like 'Tether', that are unregulated, reduce in popularity over the next couple of years, and the digital currencies and tokens that are regulated will be more at the forefront. Central bankers are not stupid - they realise there are many valuable features of digital currencies, but yes, I agree with Janet Yellen when she said that transacting using Bitcoin is not efficient. However, we know that 86% of central banks are working on creating their own digital currencies, and China is years ahead of everywhere else. So, we are watching what Yellen and the Federal Reserve in the US will do with great interest.”

Innovation and increasing adoption

A guest highlighted the innovation taking place in the digital asset universe. Leveraging blockchain, leveraging cryptocurrencies, tokens, Stablecoins, STOs, the market is always moving ahead of the regulators; it is all moving incredibly fast, even though it is at the very early stage of adoption.

Expert Opinion - Joshua Foo, Regional Director of the ASEAN Region, Chainalysis: “The power brought about by cryptocurrency and blockchain technology makes data literacy and analysis more important than ever. Every industry, ranging from financial institutions, cryptocurrency businesses and public sector regulators will need actionable partners who can provide insights into this growing ecosystem.”

Expert Opinion - Steve Knabl, Chief Operating Officer & Managing Partner, Swiss-Asia Financial Services: “Digital Assets Funds are very diverse and can offer all sorts of strategies from listed Long only Trusts, fundamental trading, arbitrage, market making or volatility arbitrage. There are not many funds, but there is choice of risk allocation.”

Expert Opinion - James Quinn, Managing Director, Q9 Capital: “Our clients generally self-select into two distinctive groups quite quickly. Active traders and those that want to just buy and store cryptocurrencies. Investors often seem to feel better about doing something as opposed to doing nothing in this space and I haven’t found anyone who thought investing in these digital assets was a waste of time. Knowing something today is worth a lot tomorrow. So educating yourself about the asset class and getting set up is crucial.”

Education and experimentation

The final words went to panel members who summarised where investors, especially the wealth management community, might start. “I find the private banks and some advisors hypocritical, stating that Bitcoin, for example, has no value. One wonders if it is because they have no clear way of making money from this market. However, I firmly believe that in the coming months, more EAMs, IAMs and private banks will be moving into this space, educating themselves and catering to the rising demand. I think the whole area of asset management or private wealth in crypto has a tremendous future. Remember, private banks initially were a bit reluctant with derivatives, even on emerging markets, but look where they are today on those investments. And look at the announcements only in recent weeks, from custodians like BNY Mellon, from Visa, MasterCard, Tesla and so forth. My personal recommendation to everybody is to trust yourself. Buy into Bitcoin at modest size to start and check it out. It will make you follow the markets you've invested in it. I give my children a slice of Bitcoin as a gift, and literally, it could be the most valuable gift they ever receive. And remember, you can buy up to 8 decimal places of a Bitcoin, so it is not like you need to put up the equivalent of USD50000 or whatever one Bitcoin trades at; you can buy tiny slices of it that are called Satoshi.”

“In the Chinese world, they say if you want to learn something, you have to pay some school fees,” came another voice. “In Hong Kong, if you play mah-jong, you probably lose the first few games. In the digital world, there are many, many platforms, apps on your phone that do proper KYC, that make it all very simple. You can start with one hundred dollars. You can teach yourself, you can learn as you move along. If not, you're going to miss this train that a few of us are very happily on already. And as an industry, we welcome more and more people on the train, we believe in this industry. It is going to be here for a long time to come.”