Rising to the Opportunity in Digital Assets & Tokenisation in Asia’s Wealth Management Markets

Dec 7, 2022

Setting the Scene

The universe of digital assets is evolving apace, with what appears to be constantly and rapidly

Expanding numbers of cryptocurrencies, digital coins and stablecoins, non-fungible tokens, security tokens, commodity tokens, ‘meme’ coins, smart payments, so on and so forth.

In Asia, private clients have been dabbling their toes into the Bitcoin and Ether seas, or perhaps taking a bigger and more diverse plunge into the choppy waters of other exotic cryptocurrencies, or using stablecoins for instant settlements, or perhaps trying out a host of the other tokenised assets and maybe even entering the expanding universe of Decentralised Finance (DeFI).

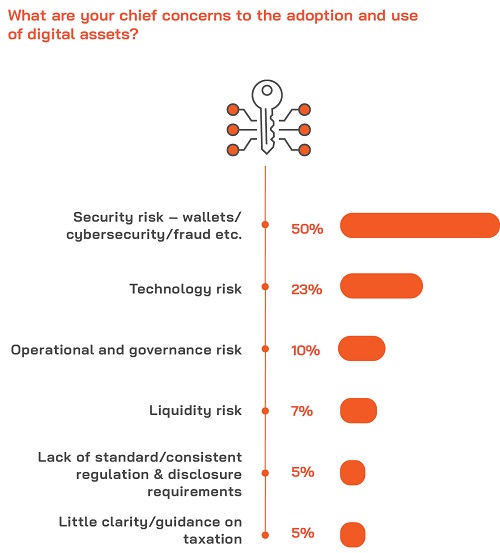

A picture with many tints and hues

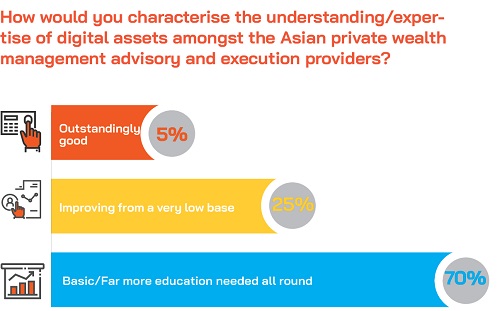

The big picture painted from the different colour of the survey highlights how the wealth industry as a whole is still somewhat unsure of how to seize the opportunities in digital assets, given the market volatility, regulatory uncertainty, a lack of clarity over which intermediaries, brokerages and others ‘experts’ to trust, as well as the lack of understanding around blockchain initiatives and uses, confusing over what DeFi really means, and also concerns over security protocols and the right technologies.

And that indeed was the core premise of this Mini Survey, presented by Hubbis and sponsored by Swiss digital assets specialist METACO. Hubbis directed all the questions at Asia-based respondents from the private banks, independent wealth management firms (EAMs, IAMs, and Multi-Family Offices), Single-Family Offices and fund/asset management companies.

Many questions to address

We questioned, for example, whether these wealth industry experts believe digital assets of various types are here to stay as an asset class, we asked to what extent they see this as a major opportunity, and then if, and also how they will enhance their knowledge, their capabilities, their advisory and execution propositions, and their associated risk management, custody, compliance and security protocols to participate in this nascent yet rapidly growing business.

Finding the right paths

The survey highlights clearly how although there is continuing uncertainty over the right ways to advance in these markets, there is already significant interest, will and commitment to improving knowledge of these assets, and in enhancing the capabilities around collaborating with private clients on these assets.

This survey is therefore our modest attempt to gauge the state of thinking in the wealth industry in Asia. How are private wealth managers approaching the digital asset space? What are the factors leading to crypto and digital asset adoption in Asia? How do you build the infrastructure to compete in the Digital Asset Economy?

In short, there are no definitive answers, but the overall impression we gained is that the momentum towards an enhanced and scaled up involvement by the private banks and wealth management firms in Asia is on its way.

Increasing Digital Asset Adoption in Asia

Coming into sharper focus

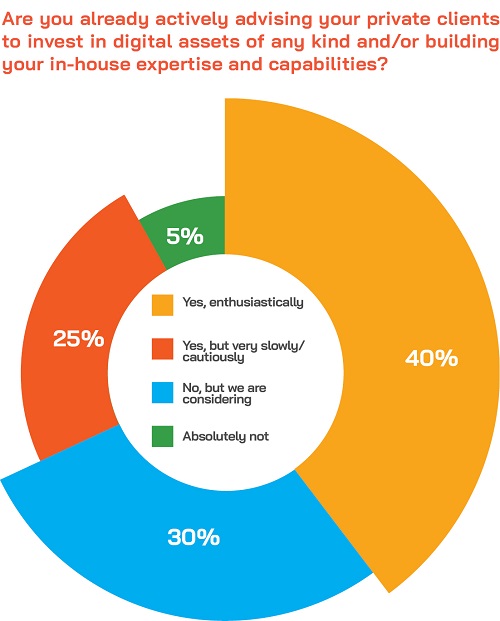

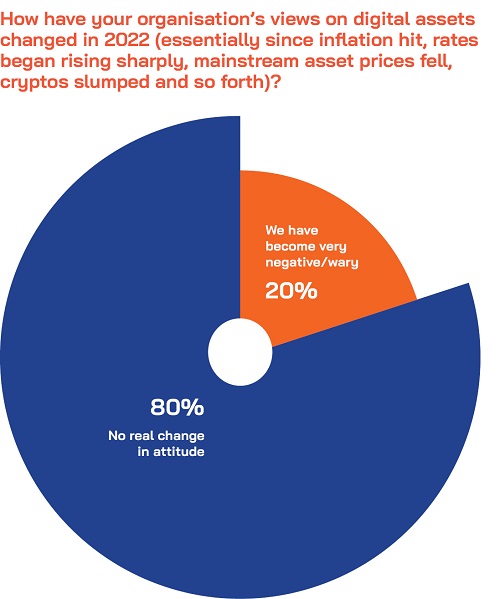

The 76 replies to our survey from the experts and decision makers we canvassed from the wealth industry in Asia indicated clearly that there appears to be a significant and growing opportunity for banks and others in the wealth industry to leverage this new ecosystem and become active in this field, irrespective of the troubling times the market is facing currently. Yes, crypto prices are well down on the highs to which many surged by late 2021, but many believe that after the crypto winter, a new spring will come and an even brighter future. And even more importantly, after the dust settles on the current scandals such as FTX, the bad players will be weed out, creating the opportunity for trusted, established institutions to step in and service the market.

So too at the same time, the more optimistic amongst them anticipate rapid expansion and greater involvement across the wider universe of digital assets. These assets include those whose value is founded on utility and adoption (such as cryptocurrencies like Bitcoin or Ethereum, smart contracts, and cryptocurrency payment coins).

A diversifying digital asset landscape

And these assets also include ever more tokenised representations of real-world assets – stablecoins such as Tether, representing specific fiat currencies and designed to facilitate instant payments and settlement, or Non-Fungible Tokens (NFTs) as tokenised fractions of value of specific tangible assets, or Security or Commodity Tokens that represent real-world financial assets.

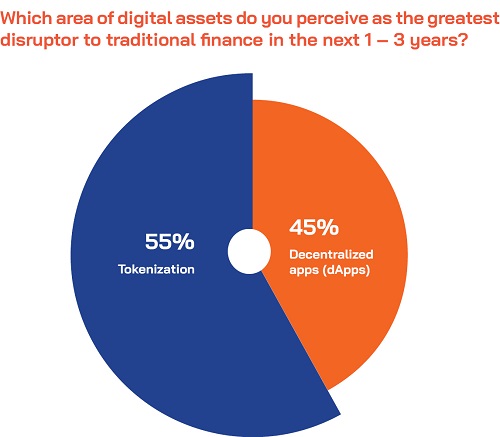

The securitisation, or tokenisation of real-world assets or non-bankable assets, is certainly a key area of expansion that the wealth management community are eager to see develop, as there are much clearer valuation parameters potentially than for many, or some would say all, of the cryptocurrencies. Accordingly, the fractionalisation of underlying assets such as real estate, collectables, fine wines, even luxury yachts and so forth is of considerable appeal, bringing such investments within the remit of mass affluent and HNW clients.

Growing confidence in the digital investment future

Financial institutions are increasingly aware that faced with all these dramatic changes and opportunities, and the growing swell of interest and demand from institutional and from private investors, they need to consider forward-looking business strategies and position themselves appropriately in the digital asset markets & economy.

And as more of them become more convinced, or perhaps less sceptical, that digital assets are part of our collective futures, they are grasping the reality that they themselves and their private clients should not only understand more about digital assets, but they should actively participate by building some exposures in order to understand more about buying, storing, custody, and, of course, the vicissitudes of market pricing and volatility.

Building knowledge, expanding capabilities

Accordingly, many such banks and advisory or asset management firms are taking significant strides forward in their knowledge and capabilities around digital assets, as the market evolves a more professional, more institutional level market infrastructure and ecosystem. Some even hold out hope that regulators around the globe might gradually come together to provide a more comprehensive regulatory vision for the future of digital assets in all their forms.

Indeed, wealth management and other financial institutions now know that they need to play in the digital assets market, for both offensive and defensive reasons. They recognise that the scepticism and the misgivings have been steadily dissolving.

The threat of disruption is simply too big and investing in this emerging ecosystem is really the only way to protect their existing roles - as custodians, exchanges, issuers, intermediaries, advisors, and trusted partners for their private clients. Moreover, they increasingly realise that they should or perhaps need to stake their claim in a market that will boom as tokenisation opens up a much larger pool of assets.

Choosing the right path forward

But knowing that your bank or firm should invest in its capabilities and digital assets infrastructure is not the same thing as knowing exactly what its proposition or business model should be.

Like any nascent market, the digital asset market is evolving and changing quickly. Investment cases are changing. So, the key for any financial institution will be to be keep its options open, which to a great extent will be synonymous with adopting the right protocols and the right technology.

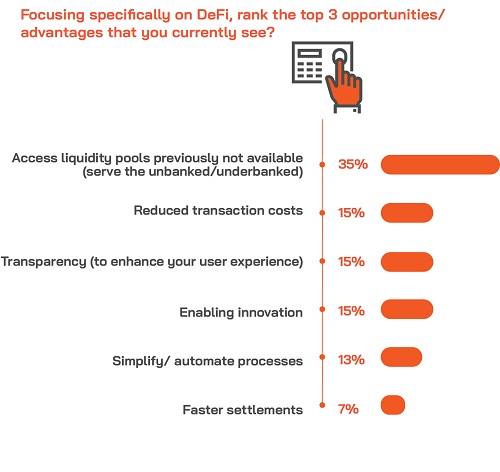

To participate, if indeed they wish to, these banks and other firms first need to decide which assets and which services they will promote, and then work out how they can build the capability and infrastructure to support those digital assets including self-custody, sub-custody, tokenisation, trading, securitisation, the management of smart contracts and embracing the new world of Decentralised Finance (DeFi) more broadly.

Leveraging the right expertise and jurisdictions

In short, they will need access to specialists within the rapidly expanding cryptos and digital assets ecosystem. They will also need to select jurisdictions through which to offer such capabilities and services. Singapore, for example, is highly regarded due to its progressive regulator, robust and rapidly expanding retail, and institutional demand for digital assets, rising participation amongst major institutions and the expanding array of specialist digital asset brokerages and custodians.

As these banks and other operators look at this diversifying digital assets universe, they will be trying to understand what they need to do to develop or to enhance their capabilities, focusing on processes, technology and of course advice across the entire digital asset value chain, from execution to trading to custody to DeFi, and to how they can project genuine expertise in both crypto/blockchain as well as banking and banking software, and how they can interface with the digital/crypto exchanges.

The Digital Asset Markets Continue to Evolve

Not even 15 years old

The cryptocurrency and wider digital assets markets have moved rapidly and remarkably forward since 2008, when the mysterious Satoshi Nakamoto issued the first Bitcoin white paper. From around 2008 to around 2018, there was a phase of inflated expectation but minimal professionalisation of the ecosystem.

However, in the latter part of that phase and in the more recent four to five years, we have witnessed the expansion of the infrastructure and the entire ecosystem around digital asset investing, trading, lending, and significant advances in security protocols and custody.

Remarkable innovation is taking place

Accordingly, we have witnessed the launch of what seems to be a plethora of digital assets exchanges and platforms, brokerages, custody platforms, all to accommodate the significant and ongoing adoption of digital assets for investment and trading (Bitcoin is the bellwether cryptocurrency) or indeed for utility (Tether is the most heavily traded stablecoin, essentially representing digital US dollars).

The scale of the potential is simply vast. Beyond cryptos, there is truly enormous potential to fractionalise and digitalise vast trillions of dollars of illiquid assets around the globe and make those liquid those the sale and trading of tokens of many types.

Tens of trillions at stake

Estimates from the World Economic Forum indicate there are over USD24 trillion of assets that could be tokenised within the next five years alone, but many think the market is many times larger than that, in short as big as the total value of the world’s stock markets combined (the US listed equity market capitalisation, for example, hovers around USD47 trillion currently).

We have also seen the emergence of the decentralised finance space, better known as DeFi, which is essentially the blockchain-enabled virtual world of finance rather than the central bank-controlled Ce-Fi, standing for centralised finance.

The age of enlightenment

The past five years or so can accordingly be considered a phase of enlightenment during which digital assets have really started to come of age, moving well beyond all that earlier negativity and scepticism and into a more complete ecosystem, with licensed brokerages, futures, adoption by global asset management brands such as Fidelity in the US, or in the Philippines by names such as Union Bank of the Philippines, or in Singapore by leading names such as DBS, and so on and so forth.

The big names are joining in

Indeed, there is little doubt that the even as the world’s equity and digital assets prices have fallen – sometimes dramatically – since late 2021, the digital asset market infrastructure continues to evolve apace around the world, with big names and serious players joining the fray, including leading commercial and investment banks, leading national and private pension funds, and even central banks, all seeking to gain exposure to and possibly some degree of control of this asset class.

These major institutional centralised finance brands and names are all trusted and regulated, and have been in business for a long, long time. Being risk-adverse institutions, the fact that they are moving into this market means that the opportunity is real, and massive, to be worth the investment.

The banks and other wealth industry players are gearing up

Momentum gathers

While all of these – any many, many more – developments are taking place, at the same time, demand amongst private clients is rising across the world, and this is evidently the case in Asia, driven to some extent by demand from HNW and UHNW clients that are wanting to get exposure to this space, and also by younger mass affluent and retail investors who are more digitally savvy and far more optimistic about the long-term future and impact of digital assets on all our lives.

Unlocking opportunities with the right keys

Accordingly, the private banks must respond, and other wealth managers must respond to be able to capture this market and unlock the opportunity.

But where do you start? The reality is banks and other institutions, and firms must walk before they can run. The reality is that private banks and other market participants need to get their involvement right from the outset, with the right technologies, the right strategies and of course, the right levels of compliance and security, including being able to manage and store the assets for their clients themselves, or partnering with secure external platforms to achieve those goals.

For example, there seems to be a myth that security is only important for global tier one multi-jurisdiction financial institutions. But the reality is very different – the wealth management industry advises on, looks after and helps secure people's private wealth and assets in the traditional finance space. That does not change in the digital asset world. In short, it is of paramount importance to secure any and all assets for private clients.

In a digital world, technology is of supreme importance

Technology and decisions around that will be central to banks and other firms getting their approaches right. Financial institutions spend more money on technology than any other industry. Part of the explanation lies in the fact that financial services is an information intensive industry: its product is both digital in its manufacture and increasingly in its distribution.

But the other reason is that financial firms spend so much money maintaining and updating legacy systems; an outcome of bad historical decisions to invest in proprietary and overlapping solutions.

Rebuilding for a new future

Digital assets give firms the chance to start afresh; to rebuild the future of their businesses without the legacy. However, it means not repeating the same mistakes – jumping into technology decisions that will cultivate the same expensive legacy IT estate.

Get it right from day one, but stay flexible

Adrien Treccani, CEO of METACO, explained this in an article he penned for Hubbis earlier in 2022.

He said that if a financial institution moves into the digital assets market, it will immediately be faced with choices such as whether to adopt self-custody (meaning to remain in charge of storing the private keys that secure the digital assets) and then work out how to do it, or whether to outsource that function to a bank or custodian. Should they leverage public distributed ledger technology (DLT) or permissioned ledgers? Should they run their solutions on their physical premises or in the cloud?

And he remarked that it is essential to get each one of these decisions right, as each road taken might close down other viable routes, and create hefty, unwieldy legacy infrastructure.

Orchestrating an agile future

His own conclusion was that the solution lies in financial institutions choosing orchestration systems to offer them maximum efficiency and effectiveness today, but to also provide them to adapt with agility to the rapidly evolving world ahead, which any of us can only imagine, extrapolating from today’s evidence, but which will no doubt prove quite different in reality.

And he articulated this rather vividly as follows: “If, looking around at the pace of change, you think your institution may be like the proverbial frog [in the pot], oblivious until now about the rising temperature, it is not too late. Many of your competitors that acted earlier, led by industrial-age procurement team and processes, made the classic mistake of selecting monolithic applications. By choosing orchestration instead, you can introduce the flexibility that will enable your firm to navigate this fast-changing space more successfully – allowing you in time to leapfrog them.”

Knowledge must be spread far and wide

But we digress, because the exact technology applications and decisions are not the core subject of this Mini Survey and Report, which is essentially to highlight the opportunities, the challenges and to gauge the state of play in Asia’s wealth management community, and to highlight the very important areas of knowledge and education required, as well as optimisation around strategy and then implementation.

And there is no doubt from this survey and from the body of work that Hubbis conducts in this nascent digital asset space that there is a virtuous circle of demand and capability enhancement that is evolving. In the private client sphere, private banks are moving into the digital asset arena as demand from HNWIs and UHNWIs increases and as they see that crypto custody and trading will pay for their expansion and investment in this universe.

Taking it step by step

That is why they are moving, often step by step towards greater capabilities and knowledge. Take BBVA Switzerland, for example, which is part of the giant Spanish financial group. It started with Bitcoin custody and trading for HNWIs only and in Switzerland alone, and then set about developing an integrated crypto service into a newly built challenger-bank brand named New Gen with global outreach across Europe, Latin America and also in APAC, and targeting mass affluent and higher wealth customers.

They are one of the growing number of banks and brand-name financial institutions that are developing the necessary platform to scale their digital asset business technically and commercially, and at the same time making sure they are compliant with whatever regulations exist in the different jurisdictions in which they might operate.

A long journey ahead

But let’s also be realistic. The digital assets markets, the infrastructure and the overall ecosystem are relatively immature, and those who wish to provide services in these areas are struggling to keep pace with the rapid adoption amongst investors, and especially amongst institutions. Nevertheless, as digital assets move gradually more mainstream, there is somewhat of a domino effect, a virtuous circle of adoption leading to more activity and further expansion of the ecosystem.

For example, in the Philippines, there are literally millions of retail and mass affluent customers – most of them young and digital natives – who are buying, trading, and holding cryptos or indeed other digital assets such as NFTs. Union Bank of the Philippines (UBP) is one major bank that has been dramatically boosting its execution and custody capabilities in these areas, at the same time as elevating its governance and workflow protocols, and risk management to ensure the right policies and processes are adhered to, including for KYC and AML.

The Final Word – Tomorrow’s World Beckons

Taken as a whole, the survey very clearly underscores how the stage is set for the ongoing rapid and remarkable expansion of the universe of digital assets. However, the replies also highlight how in order to take things to the next stage, the colossal dynamism of key advocates of these digital assets must be aligned to a deeper and more professional ecosystem, greater security, better regulatory oversight, and more ‘comfortable’ compliance and risk management protocols for the private banks and other intermediaries.

Assuming progress continues and the right roads are followed, the participation of the leading banks and wealth management firms looks more assured today than at any time before. The road ahead might be paved with digital gold, but unless the banks, advisory firms and intermediaries work out how to travel that road safely, smoothly, and confidently, they will never reap the vast rewards that could – and more and more believe really do – lie ahead.

A brief introduction to METACO

METACO is a Swiss company

that provides mission-critical software infrastructure enabling large financial institutions, banks, asset managers, and corporates to build their digital asset operations.

The company launched its APAC headquarters in Singapore in October 2021, attracted to those shores by its existing clients and by the island republic’s stability, the solid history for financial innovation, access to great technology talent and partners, and the rapidly increasing activity in the digital asset and crypto space, as well as the strong regulatory and other support for the digital assets revolution in Singapore.

METACO provides technology infrastructure to help clients manage and support digital assets including, self-custody, sub-custody, tokenisation, trading, securitisation, and a bridge to DeFi through seamless management of smart contracts.

A harmonised future

The firm’s ‘Harmonize’ platform has been specifically designed in partnership with Tier 1 custodian banks and market infrastructure players, and acts as a single point of connectivity or integration for either non-financial or financial institutions to manage a digital asset business and a digital asset offering.

Singapore was chosen as the ideal location for METACO’s Asia operations, being a technology hub for the APAC region, with the right type of regulatory support, strong talent available, and a rapidly expanding digital asset and financial sector ecosystem.

Richard Swainston, APAC Business Development Director for METACO, points to Singapore as having become the focal point in the region for digital assets and cryptocurrencies and attracting more and more of the clients that METACO either works with or hopes to partner with for the future. He explains that there are several key facets to the proposition METACO brings to the Singapore and the wider Asian markets.

Working with the global majors

The firm entered this space early on in 2015, focusing on technology for the entire digital asset value chain, from custody to DeFi, and with strong expertise in both crypto/blockchain as well as banking and banking software. METACO also brings a solid track record and clientele with it, having been working with some of the largest Tier 1 banks across the world for several years and already with some leading Singapore institutions.

METACO has clients regulated by a broad array of jurisdictions, such as the Monetary Authority of Singapore, the Central bank of the Philippines, Finma in Switzerland, FCA in the UK, BaFin in Germany, Banco de Espana, Liechtenstein, and others.

Knowledge, experience and trust

Swainston says: “We bring a solid track record and clientele with it, having been working with some of the largest Tier 1 banks across the world for several years and already with some leading Singapore institutions. In short, we bring knowledge, experience, and trust, and that is why we are able to work so extensively with the major banks, the leading custodians and private banks, the well-known asset managers and both traditional as well as digital/crypto exchanges.”

He adds that the METACO platform is therefore a one-stop gateway to secure participation in the expanding universe of digital assets, delivering a solution that is infinitely scalable with the highest possible security so you can get a fast go-to market through something like a fully managed cloud infrastructure solution.

Agility and efficiency

“The platform is future-proof,” he states. “METACO offers ‘Agile’ orchestration capabilities to manage complexity and growth, both now and as the industry develops their clients are in control over a fully extendible platform, and both compliance and multi-jurisdictional governance are managed so they can scale globally. You want to capture the opportunity that is out there. We are here to help. And that is what we are doing by working closely with important names in Asia, for example in the Philippines with UnionBank.

He adds that in the Philippines as a whole, there is an estimated 23% of the population in the country that have held cryptocurrency of some form. He says the younger generations – and there are billions in Asia - are digital generations, and their adoption is accelerating. “It is all growing exponentially and is a huge opportunity,” he reports.

Defensive and offensive plays

And he explains that they are now also expanding more broadly to banks of all sizes and a wider realm of wealth managers, challenger banks, hedge funds, brokers, and crypto native start-ups. In short, we work right across the spectrum of organisations wanting to operate a digital assets business .

“To see the speed and scale of expansion in this arena, look at the arrival of the DBS Exchange in Singapore, for example,” Swainston observes. “That alone has been a major step forward and paving the way to bring digital assets more mainstream. We are seeing a domino effect, a virtuous circle of adoption leading to more activity and expansion of the ecosystem. And behind it all, there are more and more opportunities for technology providers such as us, as more players come in, and as they expand the range of options and services on offer. It is a snowball effect.”

Building from the ground up

Noting that some banks are more proactive, whilst others are more on the reactive side, Richard says everyone is carefully watching the evolution of the market.

He explains that the simpler first steps centre on digital asset custody and trading as the foundation, with more complexity down the line in the form of tokenisation, DeFi (or decentralised finance), lending, borrowing, and staking.

“But the core is the custody and trading as the starting point, as those capabilities are needed throughout the evolving ecosystem,” he says, concluding his comments. “We are a leader across the entire value chain. We span seamlessly across simple use cases such as custody and trading to the complex functionalities such as tokenisation, smart contract management, and bridging the worlds of CeFi and DeFi. And through our Singapore office, we now bring a lot of knowledge and trust at the intersection of Swiss quality and experience, and Asian innovation and demand.”