Wealth Management in the Philippines: The Quest to Fulfil the Country’s Immense Potential

Oct 29, 2021

A group of local Manila-based and also regional/international wealth management experts assembled for the virtual Hubbis Digital Dialogue of October 19 to consider how and where the Philippines’ wealth management market is developing, set against the backdrop of other ASEAN countries. They analysed where there needs to be more progress and what blocks need to be put into place in order to facilitate such progress, such as regulatory liberalisation, greater investment by the local and international players, more trendsetting by the new JV partnerships between onshore and offshore partners, and so forth. Understanding the key drivers and current competitive environment is vital for the positioning of the local and international players as they jostle for prominence in what is certainly a market of huge potential, as the population keeps growing and as the economy and private wealth creation keep expanding. Even amidst the havoc of the pandemic, the Asian Development Bank is anticipating GDP growth of 4.5% in 2021 and 5.5% in 2022, and with inflation rates expected of 4.1% in 2021 and 3.5% in 2022 and declining interest rates, there are good reasons for the country’s mass affluent and HNWIs to take more cash out of deposits and to invest in the financial markets. Moreover, the demographics are very encouraging - the Philippines has both a huge and a very young and fast-expanding population, the third youngest in Asia. But the Philippines has always been one of those economies and markets that has perhaps promised more than it has delivered. So how does the country fulfil its immense potential? The panel of experts offered their insights and advice.

Panel Members

- Stella Cabalatungan, Executive Vice President, Head of Wealth Management Group, BDO Private Bank

- Patrick Cheng, Executive Vice President and Chief Financial Officer, China Banking Corporation

- Scott Moore, IMCM, Director - Private Clients, Head of Philippines Office, Henley & Partners

- Abhra Roy, Head, Finacle Wealth Management Solution, Infosys Finacle

- Vincent Magnenat, Chief Executive Officer, Asia, Lombard Odier

- Michael Oliver Manuel, Chief Market Development Officer, Sun Life Financial

There is today mounting optimism that the private sector, the regulators and the government are more aligned than ever in wanting to promote the financial sectors as the country’s population grows so rapidly, as the mass affluent are rising fast and as the government seeks to bring more of the massive offshore wealth of the rich and super-wealthy back onshore.

The result is a gradually more diversified range of products and solutions onshore and a broader range of private banks and independent wealth firms, some of the alliances between international names and powerful local financial institutions with the reach across the country’s vast lands and many thousands of islands. Moreover, there is rising interest amongst the wealthy in estate and legacy planning, in alternative assets, in globalising their investment portfolios and in generally enhancing both the risk management and also allocation strategies they adopt. And the wealth management proposition has become more encompassing, especially since the pandemic hit.

Since the pandemic hit…

A local expert opened the discussion by commenting that the virtual connectivity with clients will likely persist well beyond the pandemic, as it is efficient and time saving, especially when it comes to dealing with families in different locations. What has changed is the willingness of the older generation to consider earlier and more structured transfer of wealth.

“They more readily see the value of what we offer in trust structures and estate planning,” they remarked. “When you're in the private banking business, you're not just talking about liquid assets or securities, you are also talking about other services. When you talk about transferring your legacy to your next generation, it's can also be about giving them a second home or citizenship elsewhere to keep them safe. We can also look at alternative investments, such as precious metals. So, we are here to help and assist our customers to offer different types of services, and not necessarily making money out of it, but being the one-stop shop, to be able to help and assist our customers. We offer our open architecture platform, but it is not only about investments, as we offer strong support and guidance and value to them, and their generations to come.”

As to domestic assets and investments, this expert said they specialise onshore, while the offshore institutions are clearly experts in the international markets and structures. “We consider ourselves more partners with those banks than competitors. I think we can enhance each other's value by working together also with offshore companies and banks, so that we can both offer a holistic approach and better cater to the needs of our customers.”

A robust market for wealth management

An expert on the panel reported how the private banking and general wealth business domestically had been performing extremely doing well, driven by rising higher end wealth and demand and elevating their bank’s value proposition, helping boost the realisation among their target market that there really is a need to engage in the services of a private bank.

“We have not changed our targets, we did very well last year, and we have some really very aggressive targets that we hope to achieve by year end,” they told delegates. “We have a five-year plan; we will stick to it. The focus will be more for the non-traditional investments as far as investments are concerned, and also conversions to more personal management and trust, instead of just selling products. There will be no product pushing, it's really the value proposition that we will provide, and whatever products and services that they avail of, will be to complement the advice that we give for the long-term plans of our clients.”

Boosting the Philippines Wealth Management Market in the Post-Pandemic era

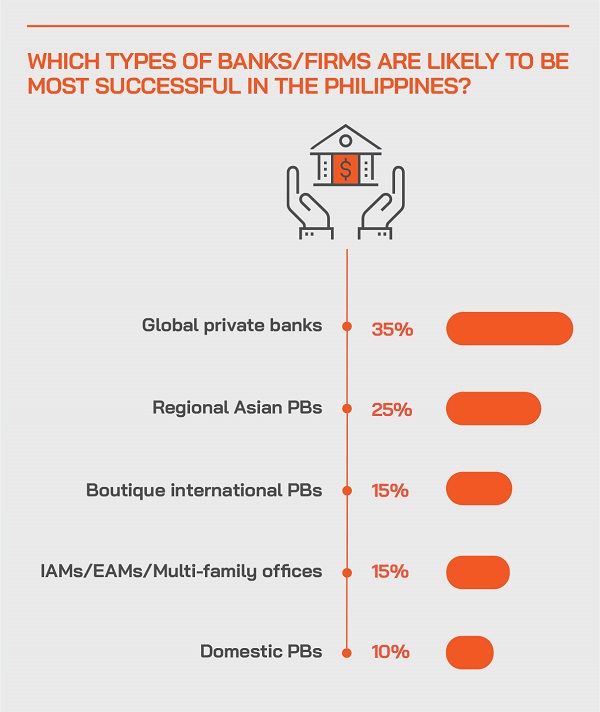

For anyone practicing wealth management in the Philippines, or indeed considering entering the competitive arena, the replies to the questions we asked delegates are remarkably emphatic and incredibly encouraging.

There is a multi-coloured picture of a market in which clients are positive about investments, where they are diversifying their onshore assets including into alternative assets, where they are buying into more global investments, where they are comfortable combining both active and passive funds, where they are seriously interested in exploring more of the potential regarding DPM, in which they are organising their estate and legacy planning more actively and effectively, where the thrust to digitisation is ongoing, active and well-embraced by clients, and where there is demand for products and services from a wide range of banks, firms and providers.

We seldom witness such positivity from our surveys and such support for the development of wealth management in-country. Now it is up to the incumbents and the new entrants to fulfil this great potential.

The song remains the same

Demand for investment products has remained strong throughout, especially with interest rates falling to lows, and very quickly. Clients continue to look for yield enhancing products. The Philippine client normally veers towards Fixed Income products and there continues be an emphasis on this. Of course, there is also a segment or a pool of money that is trying to take advantage of market dislocations, especially at the start of the pandemic.

By and large, banks remain the dominant wealth management players. Clients continue to trust banks and their long-standing financial advisors to help them navigate this volatile market environment. In addition, banks are a source of strength during this pandemic. Unlike in past crisis, when it could be said that some banks were the source of weakness.

Insurance – mortality in a stark light, planning needed

Turning to insurance, especially in the HNW segment and above, a guest reported that for deals of USD1 million and above, the numbers keep growing on a yearly basis, and the ranks of advisors as well. “It is not uncommon for clients to actually seek for about USD60 million of coverage here in Manila, which used to be few and far between way back, but it is very common nowadays that proposals will land on my table for USD30 to USD60 million of coverage. However, our retention limits for insurance are very low locally and our insurance coverage is certainly low as well, with retention limits of about 150 million Pesos, and that's the biggest in the industry. However, with international policies and working on referral arrangements with private banks, we can get our clients covered for USD60 million or so.”

He explained that there is a significant increase nowadays for protection and wealth transfer, particularly for families who have been in the business for such a long time and who were not really a fan of insurance, and who used to look at insurance before as an expense.

Proactivity amongst clients

“But nowadays, they actually knock on your door and say, can you set up a protection policy for us? They ask how we use this as a wealth transfer mechanism. And another trend is certainly that they are looking at traditional life insurance policies, particularly because of the guaranteed cash payouts or the dividend payouts that traditional life insurance policies typically give instead of being exposed to variable unit-linked in the market, where the uncertainties of economies make it move up and down. In short, they want the certainties of traditional policies, they want protection, they want wealth transfer mechanisms, and certainly they are now going for global diversification.”

He added that for many clients, the last two years from a Philippines perspective has been somewhat frustrating for many of them with equity markets moving up and down and bond markets as well. “They prefer global exposures today,” he reported.

The specifics of demand

As to particular policies, he also reported that the demand today is typically for term life, the simple traditional life insurance policies and variable unit link. “These are typically far from the type of demand internationally, where clients favour universal life and whole of life products,” he explained. “But it is very hard to develop products like whole of life product and universal life down here in Manila, because as a third world country and therefore using the third world mortality tables, the costs would be too high due to default assumptions being much higher. Accordingly, in developing UL or developing whole of life product we are squeezed from the asset perspective because default assumptions are much higher and therefore, we need to provide more margin for that. This means we have to leave it to the international side to actually offer those products to high-net-worth clients.”

Tough to finance premiums locally

Another factor, he reported, is premium financing, which is very tough to provide in the Philippines. “The combinations of other products, premium financing, the white glove service is certainly much easier to do from a Hong Kong or Singapore perspective,” he said. “So, rather than take the whole route of developing products, setting up white glove service here, looking for premium financing partners, it is easier to go the referral route, and we can serve the clients well by doing that.”

As to distribution, naturally during a pandemic it is tough for agents to walk into people’s offices and homes, forbidden actually in most cases. “Our calling card before was that our 20,000 agents were 20,000 walking branches that go to your houses and work with you, but the reality is today we must of course go digital. Additionally, 20% of the agents produce 80% or more of the business, and they tend to be the more experienced and older agents, but they are not so comfortable with digital. Accordingly, if you really look at most of the deliveries over the past two years, the biggest branches are really coming from millennial branches who are doing digital very, very well. In fact, for the last 10 years, we had one big branch, which has been number one year in and year out, they have become a branch populated with about 1500 advisors whose branch manager is 29 years old, and the average age at the branch is 23. And they're producing a much bigger business for us than the top brands for the last 10 years.”

He added that they had also seen over the past year or so, that even if you have everything digital in place and working well at this point, if you don't have the right products for the market it doesn't translate to sales numbers. He noted that many clients have been looking for global investment diversification, alongside the typically stable returns of the local money market and other onshore funds. Accordingly, product development has been very key for us in terms of things that had to improve,” he said.

Taking the global assets road

Another guest agreed that fears over mortality have driven significant changes in attitudes locally. And as to investments, poor and volatile local performance is in stark contrast to the incredible surge in prices in major markets.

“The market here has changed significantly and for the better,” he said, “with eyes wide open to global opportunities. A key driver is the change in mindset. This encourages the local players here to have some kind of a tie-up in the case of multinational institutions that have overseas offices, or for those who have the scale here to tie up with product partners, I think that is very much the way to go right now. So, players here are looking for some partnerships, some alliances in order to grow to where their potential should be.” And that means more international coverage and access to products and ideas.

Another expert agreed and highlighted the value of international/local partnerships, bringing global experience and standards to the local market through well-known domestic financial institution brands. “We want to deliver local access to the global market, and to make sure the clients obtain the same quality of service that you can get from traditional offshore centres,” he reported. I think of course, that this is a journey, especially on the investment side, and also on the education side and the knowledge about the global market. And this is what we are doing together with our friends here and in other Asian countries for several years.”

He stressed that for investment performance, so much of the success relates to asset allocations, maintaining that some 80% of the performance is generally derived from the right approach. He remarked how the local capital market had under-performed in recent years, whilst the global markets had raced ahead. “But what does that mean for the future?”, he pondered. “Diversification is very important, and we offer that to clients locally through our partnerships.”

He explained that the opportunity is huge onshore, with the next five years set to see an increase of 35% in UHNW wealth in the Philippines and 36% for HNWIs. “Clearly there is growth and potential in these segments,” he reported. “We see also new generations of clients, that are, I think, very sophisticated in the sense of their needs of investment and diversification of investment. So, on top of that, with the right partner to work with us in the Philippines, which makes the country one of our priority markets in the region.”

He explained that the pandemic had meant naturally little travel potential, but to exploit the great potential, investments in technology had helped significantly. He explained that to impart the right advice to clients and to their partners to disburse to their clients was extremely important at these times, as there remain so many anomalies and uncertainties domestically and globally, including the threats of inflation, rising rates, high asset prices and geopolitical anxieties.

Sustainable approaches

He also pointed to the value of ESG in investments, something that he said is very close to the core of their bank, noting mounting evidence that adherence to ESG results in lower volatility in portfolios and improved performance.

Embracing digital

Turning to digital evolution locally, an expert commented that there had certainly been acceleration of digitisation, driven by the pandemic, the rise of younger generations and transfer of wealth and improving internet and other connectivity. “There is no way to slow the progress into a digital world, it has already started, many of the banks who are working with us have already started this journey of digital, and especially around client onboarding, client communication, and it is all much more efficient, bringing different parties into calls rather than struggling through Manila traffic and so forth. Communication media are certainly changing, it's going to change or revolutionise the way onboarding into happens, how you manage the portfolios and how you advise the customers. The roadmap, I think is very clear, I think, it's just a question of how fast it is going to be and taking into account the local regulations.”

An expert observed that there are two ways to approach digital evolution. Top-down means right from starting from your client, and you go down to your front office, your middle office and your back office, he said, and you cover the entire gamut of technology changes that are required. Or customers can look at it the other way around where you do it bottom-up, where you start from your core engines, like the operations and make it very digital, API driven, which could connect to any system and then you connect back through the middle office, front office and finally reach the customer.

From the core and up

“Now,” he said, “there is no right or wrong way of approaching this technology approach. Because what happens is many of the banks or the institutions do have very old legacy applications that are in play. And when you put that digital layer or cosmetic layer over that, it does not help in the long run. So, what happens typically is down the line in future, you get stuck again, where you're stuck with a very legacy application, and you have just applied some cosmetics on top in terms of maybe digital onboarding, some plugins you’ve certainly managed.”

Accordingly, he stated that the correct way down the line for future for all banks is to enhance and upgrade the digital core engine, providing a digital hub for the wealth management, operations business, the product factory, the open architecture, and where they can bring in all types of products into it, be it wealth, insurance, unit linked products into it. “And then they distribute all this through various services, APIs, to the customer channels, and work with FinTechs, many of whom can achieve value-added solutions in small, very niche areas, but where you need those to be pluggable seamlessly into your entire ecosystem.

“The biggest learning that we have from across this region is that you just don't change the top layer for customer communication, it doesn't hold good for the future,” he stated. “You need to start at the bottom and look at your entire ecosystem, how you change it for the better.”

Step by step

Of course, it is also well established that a step-by-step approach is needed to evolving data mining and management to enhance the offering. There are really perhaps three steps to consider. The first is you can identify quick wins, you can find quick tech-based remedies that get you further ahead, these are not revolutionary changes, they are the quick steps that help build confidence. The second step is aligning data, which is useless on its own, with the right analytic tools to allow better targeted client engagements, and actionable with the RMs for example for targeted campaigns with individuals. This is not replacing the RMs, it is making them bionic. And the third step, once these series of these gradual shifts have been achieved, is reinvesting all that knowledge so that the clients repeat, test, learn and iterate.

It is vital to take all that knowledge and continue on your journey, because then you can then compete more effectively in a very competitive landscape. With the right technologies, the smaller and mid-sized players are able to compete on a more level footing with the bigger players at a similar cost.

Reporting and transparency

Another guest commented that one of the major areas to improve is around reporting and digital tools to help that. “I think when we talk about advice, when we talk about asset allocations is really to make sure that clients understand the asset allocation, the risk allocation that they have behind that, what are the expected shortfalls, expected returns that they may face,” he explained. And reporting accurately and in real time is central to the communication of that information and the associated insights.

“I think it's fair to summarise on behalf of all the panellists that there is a growing need and the importance of technology in the entire space, and the last one year has just accelerated that pace to a different level,” another expert concluded, on the subject of technology and digital evolution. “We do not expect technology to replace the human touch but it's going to play a very key part in how this entire business grows, whether you have onshore or offshore, everything finally comes down to how you're going to play out on technology.”

Expert Opinion - Scott Moore, IMCM, Director - Private Clients, Head of Philippines Office, Henley & Partners: “Filipino investors are jumping at the opportunity to expand their overseas real estate portfolios along with obtaining an additional citizenship or residence. They recognise the benefit of not only the real estate investment, but also having diversified access to healthcare, education, alternate business markets, and greatly global mobility.”

Investment migration – strong demand for alternatives

An expert observed how important alternative citizenship and residence can be for UHNW and HNW clients in the Philippines, and that the country ranks highly in the region as a source of business. Clients tend to be rich but short of time, they don't necessarily want to relocate themselves and their entire family to earn a status in another country, so instead, seek advice and expertise to allow them to stay in the Philippines, with their families, running and growing their businesses, but at the same time obtaining an alternative residence or citizenship, which can really open doors in terms of greater global mobility, better visa free travel access, opening doors for their children in the future in terms of studying or settlement freedom, an potentially even access to better healthcare, an important element for all today.

He also highlighted stability and security, pointing to the relative advantages of countries such as Singapore, or Canada, his home base originally. “A lot of our clients are looking to build a portfolio of diversified domiciles, whether that's in another passport or whether that's in another residence and use this as a tool to hedge against future calamities, whether it's natural environmental disasters or whether it's political or economic turmoil,” he reported.

Expert Opinion - Scott Moore, IMCM, Director - Private Clients, Head of Philippines Office, Henley & Partners: “Wealthy investors and entrepreneurs are expanding their portfolios of citizenships and residences. They’re looking to overcome the political, corporate, and financial risks of being limited to only a single jurisdiction.”

A harsh light on weaknesses

He explained the pandemic has really created an unprecedented increase in inquiries, not just in the Philippines, but around the world. The pandemic, he observed, had really brought to surface a lot of the inefficiencies of healthcare, of governments, not just in the Philippines, but all around the world. “It is an opportune time to invest in an alternative for families while the situation is not necessarily as serious as it could have been. For example, one could imagine an even more detrimental scenario, a disease with a higher death rate. In short, wealthy families in the Philippines are really looking at the options that we offer.”

He cited Portugal, for example, where for investment migration, applicants can invest in real estate and the potential is not just access to Portugal but later to the entire EU. Others might be looking at Canada or Australia, more expensive options but highly desired. Some might consider the Caribbean countries, where applicants can invest to bypass naturalisation and get an immediate passport.

The need to boost skills and expertise

Talent is another issue that must be addressed, however, before the wealth market can really advance. There is a shortage of wealth management expertise in every market in Asia, and this is especially true in the Philippines. How are the main competitors handling this shortage of talent, and is enough being done by them and by the regulator to encourage the industry’s development? A guest highlighted the significant efforts their institution had been making to boost education of clients and team members and to enhance training.

“Time and again, we always have seminars, webinars, and also training on sales-related activities and enhance their skills, as well as refresher courses in economics,” hey reported. “We've started seminars and trainings on virtual presentations for our customers.”

The Philippine client has gotten used to the technology connectivity tools (Zoom, MS Teams) that are being used. It also saves bankers and RMs a lot of travel time. The younger clients have also adapted to this technology very quickly. At the same time, seminars can reach a larger group of people in an efficient and cost-effective manner.

Moreover, they reported their bank had been spending a lot of time improving the platform. “We are also actually developing the client portal for customers, because now we know that they're more open to the digital way of communicating,” they explained. “So, we're developing that soon so that they don't have to depend so much on us on a simple increase. But having said that, we still recognise the fact that in a private banking business, customers would want to talk to you, see you even virtually for advice. This is not a retail bank that we are running, so handholding, personal approach is still key to developing your business.”

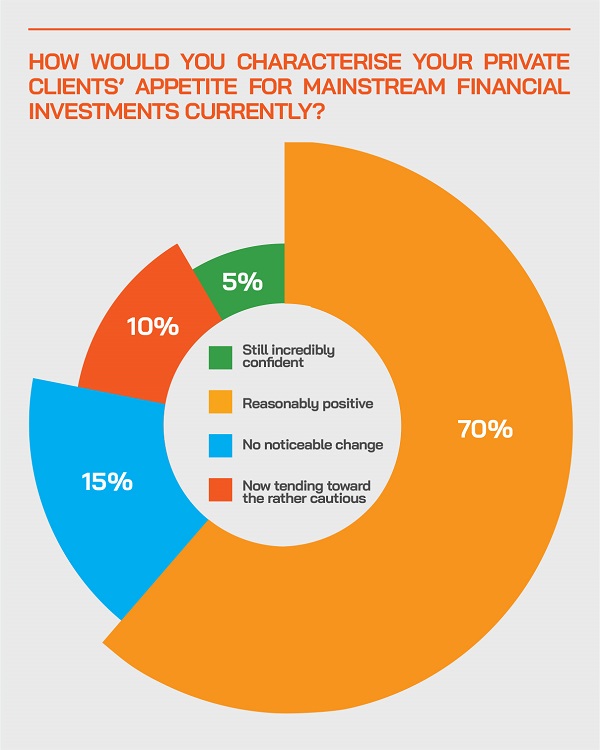

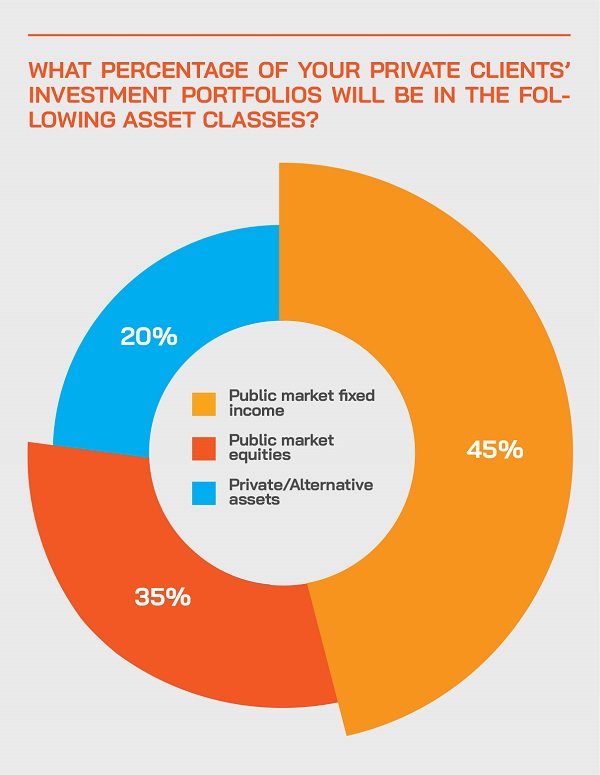

We discovered that the mood is generally resilient regarding the appetite amongst private clients for mainstream portfolio investments. We discovered that fixed income is likely to dominate, which is not surprising at 10-year government bonds yield just over 3% currently.

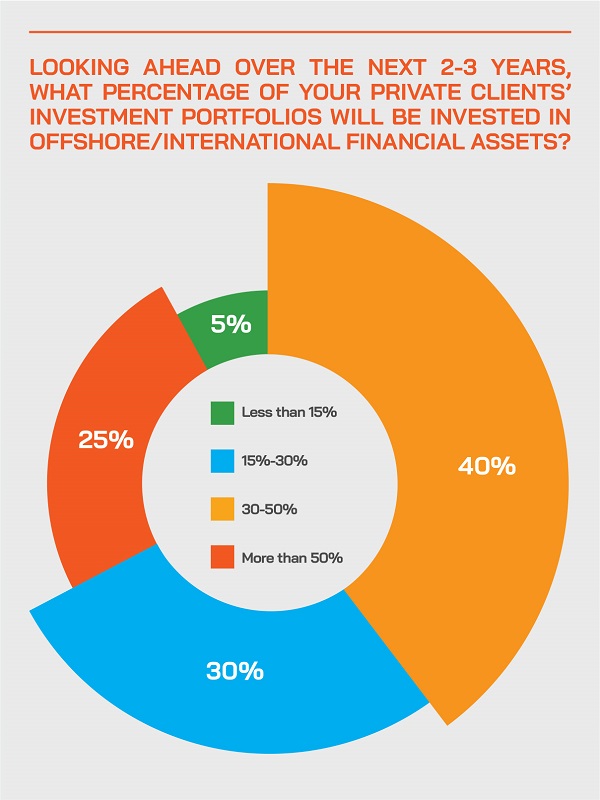

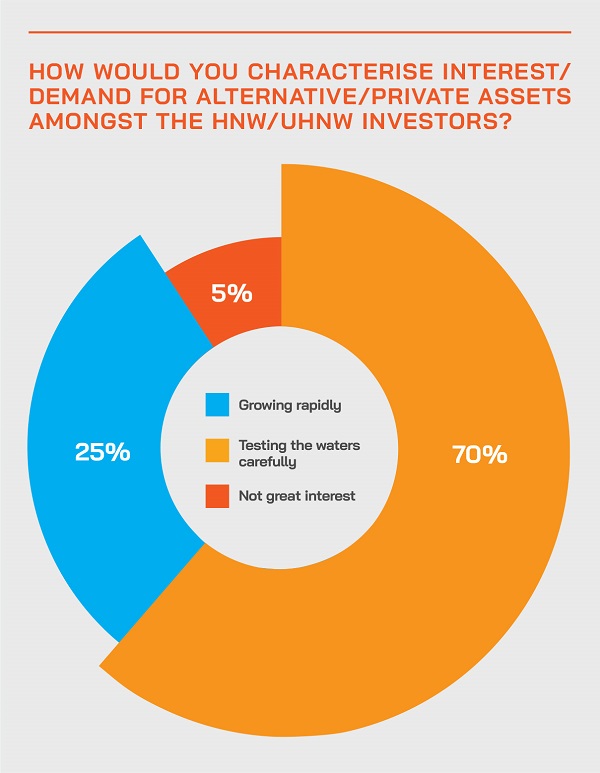

It was also reported that there is a greatly increasing appetite for offshore or international assets, partly due to the growth of feeder funds, partly due to the limited opportunities in the local market. And international private banks are well positioned to benefit from these trends, as well as some of the JVs or partnerships between major local institutions and boutique overseas private banks.

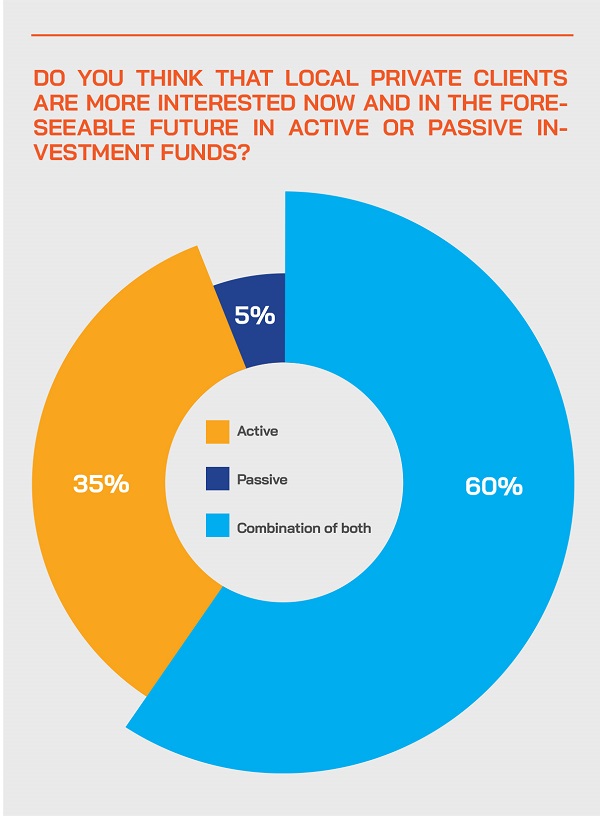

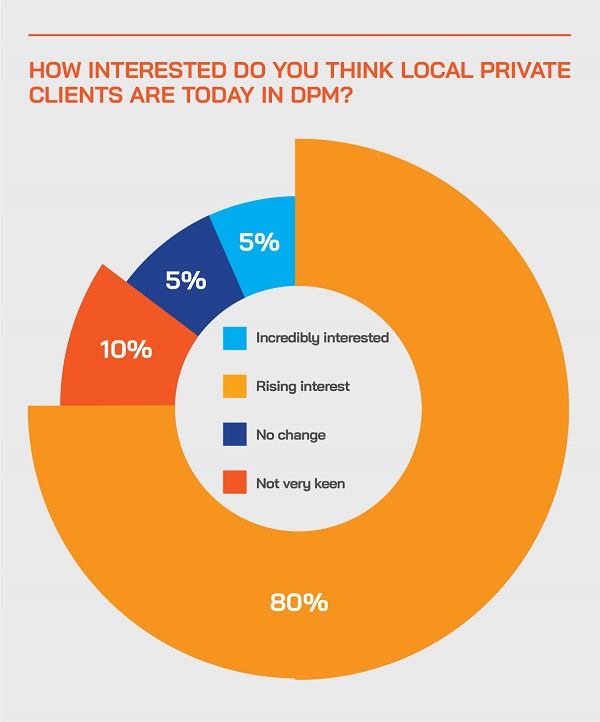

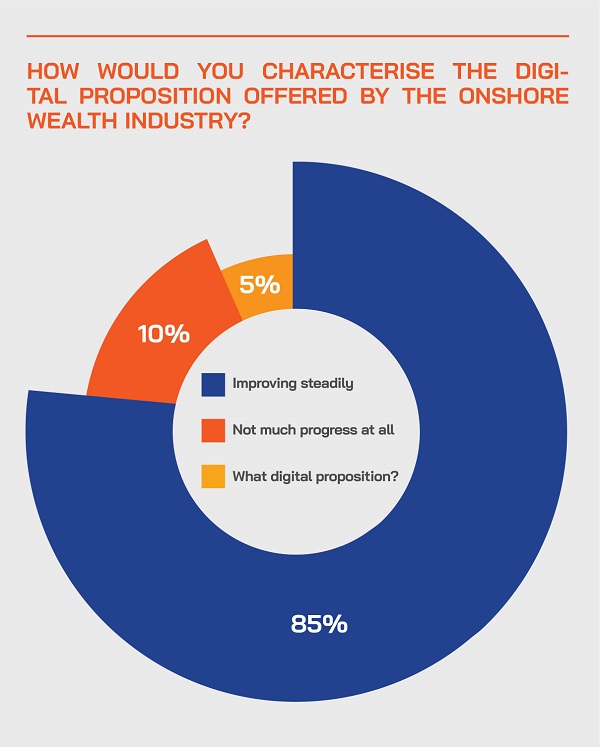

We saw that there is a strong rise in demand or at least interest in DPM and advisory, partly due to the difficulty of predicting market movement at this time of such local and worldwide uncertainty. And we heard that the digital proposition in improving broadly across the industry.