Publications & Thought Leadership

The Rise of Thematic Investment Amongst Asia’s Private Clients: Why, How and What Next?

May 11, 2021

MSCI defines thematic investing as a top-down investment approach, designed to capitalise on opportunities created by macroeconomic, geopolitical and technological trends that are both structural and transformative in nature. This investment approach offers investors a whole new way to capture powerful global trends that may drive future stock or asset performance. MSCI observes that thematic investing is not a sector, factor or ESG strategy; nor is it bound by conventional geographic or industry classifications, such as style or market capitalisation, but is instead an investment approach that takes a long-term view of how trends can change prevailing business models and value chains while facilitating investor access and exposure to growth themes of the future. A Fidelity Viewpoints report highlighted how thematic investing strategies consider long-term trends, ideas, beliefs, and values when choosing stocks, bonds, mutual funds, ETFs, and other investments, noting that among the most popular types of thematic strategies are those focused on disruption, megatrends, ESG (environmental, social, and governance), differentiated insights, and outcomes, adding that these thematic mutual funds or ETFs can provide opportunities to invest in themes as well as offering the benefits of professional investment research and management. But how does all this apply to the Asian wealth management market, and to private clients across the generations, and what are the private banks, the IAMs and EAMs and the fund creators doing to tailor and deliver more product and solutions to meet the very clearly growing demand for thematic investing in the region? Our panel of genuine experts assembled on May 6 to debate the rise of thematic investing in Asia, discussed what themes have been in demand and what trends are now evolving, and analysed how the key intermediaries, advisors and fund houses are adapting their strategies to cater to this growing segment of the investment market.

The Panel:

Andrew Hendry, Head of Distribution – Asia Pacific, Aberdeen Standard Investments

Thomas Taw, Director, Head of iShares Investment Strategy, Asia Pacific, BlackRock

Eugenia Koh, Head, Sustainable Investing Consumer, Private and Business Banking, Standard Chartered Bank

Stephanie Leung, Director and Head of StashAway HK and Group Deputy CIO, StashAway

Haren Shah, Managing Director, Head of Investments, Taurus Wealth Advisors

The Discussion & The Key Observations

This is certainly not the first time around for thematic investment ideas

An expert opened by commenting that looking back to the 2006-2007 equity markets fever, the private banks were then hyper-focused on thematic investment ideas. And then, back in the late 1990s, the TMT themes created another bubble. In short, there is nothing new here; there are fascinating themes to focus on today, but much is driven by fear, greed and also lockdown boredom, and suddenly all sorts of ideas become exciting, and fear and greed kick in even more vigorously.

There is plenty of demand and it is across the board

A guest highlighted the strong demand from their platform for thematic-based investment products, largely focused on new technologies such as AI coming of age and being applied successfully across many different industries, including healthcare, where they remarked that the development of Covid-19 vaccines was fast-tracked with the support of AI.

Big money flowing in from the biggest investors

A guest pointed to fundamental shifts in allocation amongst major institutions, with, for example, huge sums flowing in from the Asia Pacific sovereign wealth funds to ESG and broadly sustainable investments, targeting, for example, carbon-neutral or net-zero exposures in their portfolios. The money is shifting to those companies genuinely making progress and setting ambitious targets, resulting in a lower cost of capital and higher stock prices.

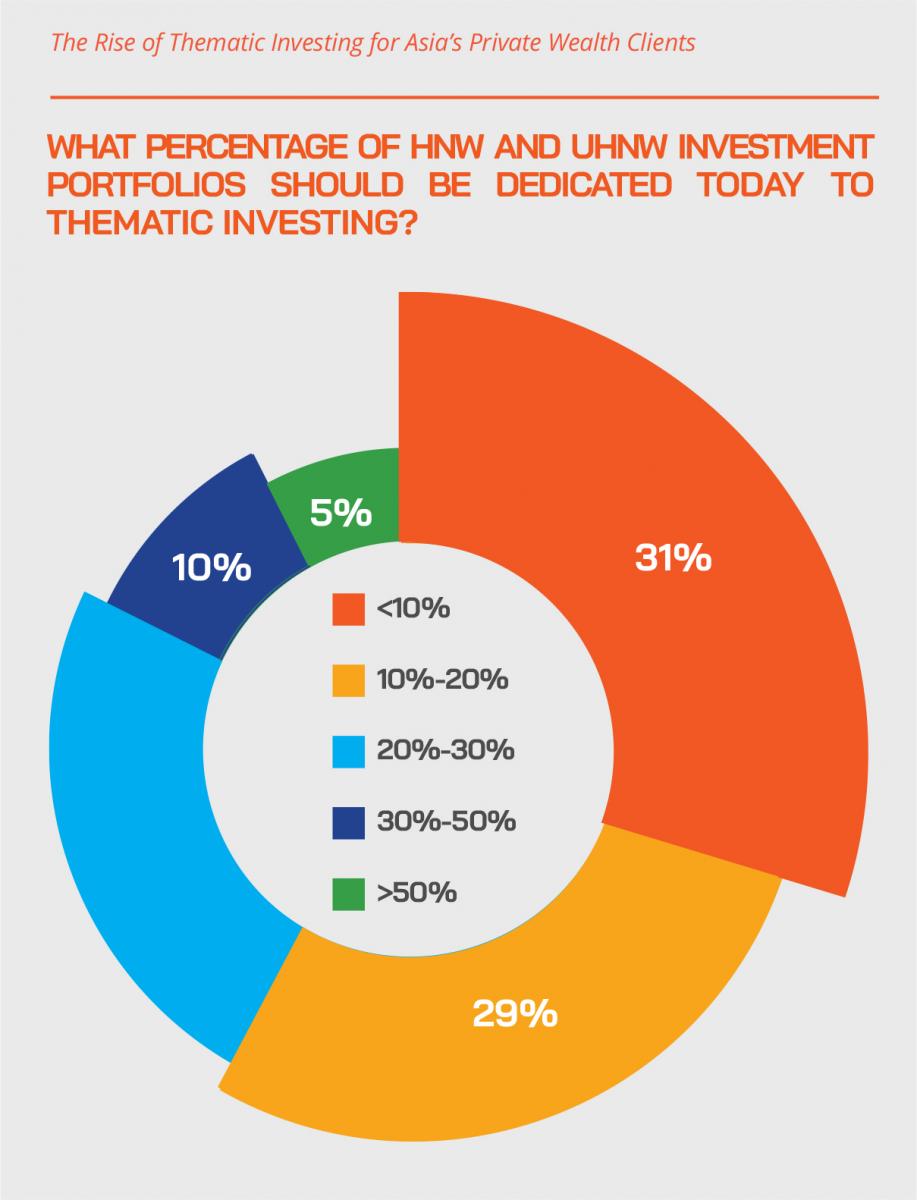

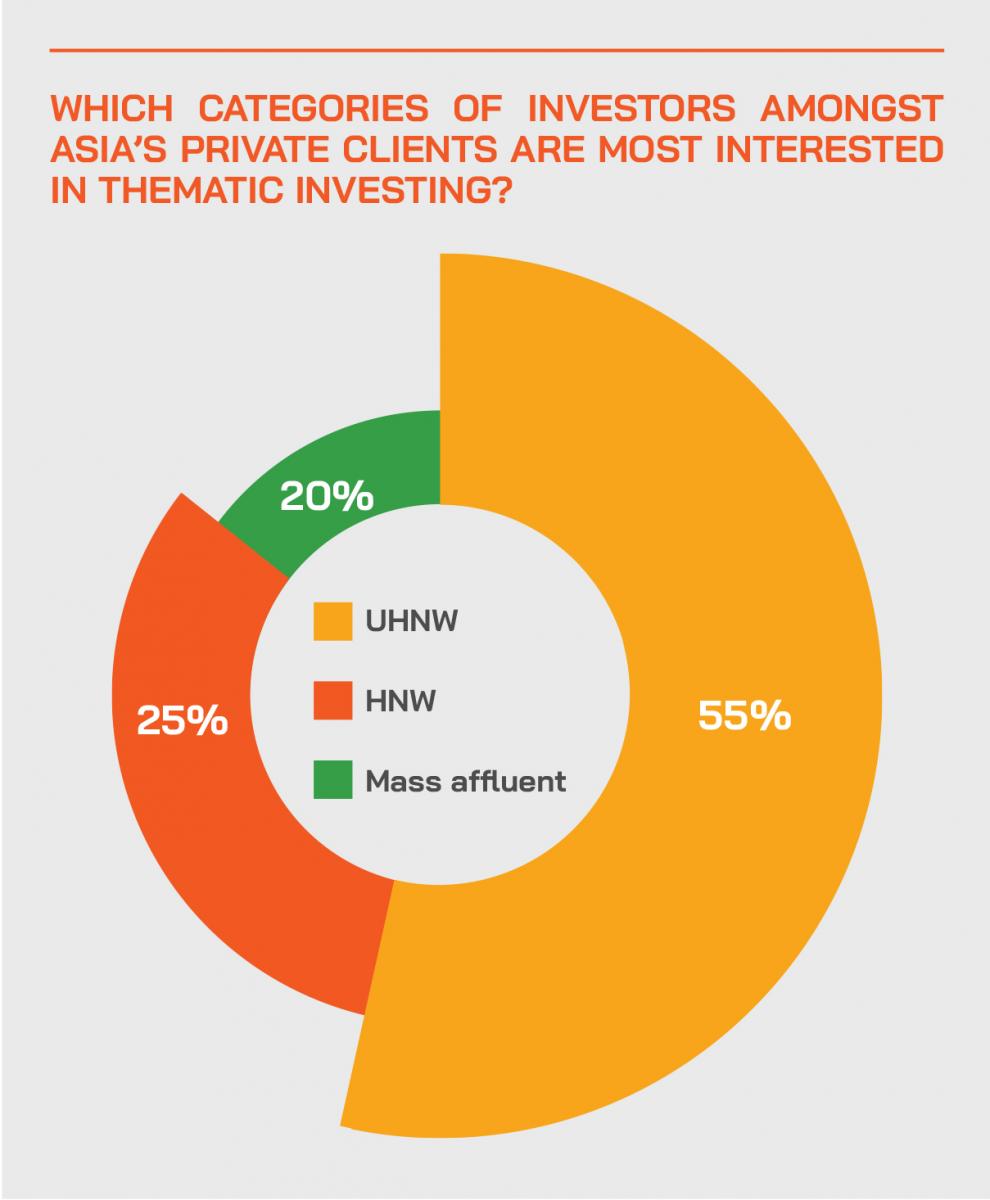

In the wealth sector, the very rich are driving change, but so too are the mass affluent

Amongst the higher categories of wealth, for example, the UHNWIs worth USD30 million and above, the clients are most driven by ESG and sustainable investments and are often expressing this interest by going into private equity impact fund. However, at the other end of the wealth spectrum, setting out on their careers or in their chosen professions, are also determined investors in this whole universe of sustainability. “The demand will continue for many years to come, in my view,” he said. “It is no flash in the pan; there is a fundamental change in the way major institutions and private investors are allocating their investment money.”

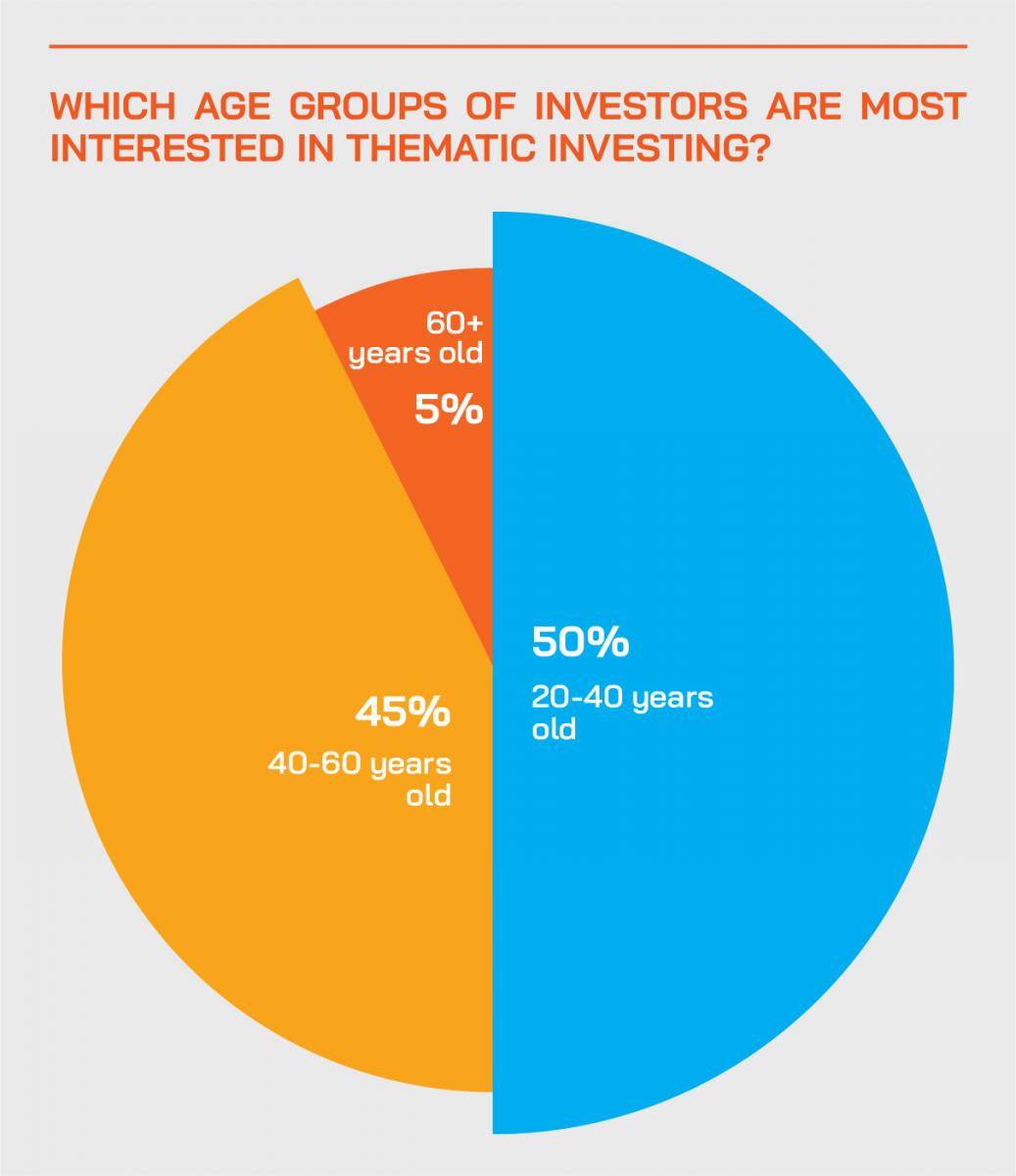

Another guest added that certain key themes, for example, AI or digital currencies tend to appeal more to the younger generations, but that the interest in thematics is broad-based and across most of the generations, except perhaps less so for the very elderly.

But beware of the speed at which markets shift and fickle investors can switch

A wealth management expert cautioned that new themes and sub-themes could come and go extremely rapidly, and therefore is firm takes a more cautious approach for their clients. Addressing the question of whether each cycle of supercycles will shorten given more retail investors flooding money into them, they observed that the speed of money inflows is much faster now than before with easy access to ETFs, but that the cycles are ultimately driven by the underlying earnings potential, although as to market performance, the cycles as they are reflected in the capital markets could be more volatile given the liquidity flows and the fickle nature of markets today.

Technology plays are only part of the far broader and expanding thematics universe

Another guest pointed out that there are several key themes his firm looks at. Technological breakthrough is one, and another is rapid urbanisation (in Asia and the developing world), the third is changing economic power (new consumers, evolving demographics and social mobility, longevity), evolving consumer habits and medicine, and also climate change and resource scarcity (clean energy, green transportation and so forth). He explained that demand is currently highly robust for thematic ETFs, and that the target is themes that will help to drive economic growth in the next 20, 30, even 40 years ahead.

Expert Opinion - Stephanie Leung, Director and Head of StashAway HK and Group Deputy CIO: “On the question of timing, actually investors should take a longer-time horizon when they invest in themes. Given most of the companies would be early stage, investors should expect many to fail, but the companies that grow out of it can be the next generation of Apple or Google, so stay the course, but mitigate risks through diversification.”

ESG – the overriding catch-all headline of the day

A guest highlighted how ESG is so popular today but that it is best to look at it from a risk management perspective and to make sure that E, S and G factors are included in any investment choice. She explained that AUM dedicated to the theme of sustainability had grown very rapidly of late – 80% in the first quarter of 2021 - but that it remained a small portion of the bank’s overall AUM. As to points of access, there are plenty of routes, mainstream capital markets assets, including ETFs, impact investments, sustainable/impact bonds and so forth.

It is the ‘E’ in ESG that drives much of the thematic investing

Another expert further refined the difference between ESG as a broad movement and specific thematic investing, noting that it is the E for Environment that drives thematics mostly. ESG, they explained, is about melding and embedding environmental, social, and governance factors into the investment process. The ‘E’, she said, is driving the governmental, sovereign wealth and other investments in clean energy, but at the same time, it is valuable to also assess whether at the same time those clean energy thematics are supported by the S and G elements as well.

The Hubbis Post-Event Survey

Hubbis: Briefly, are Asian private wealth investors increasing their allocations to thematic investing, and if so, why or why not?

Comment: The many replies produced an emphatic ‘yes’ to this question, although some observed that the uptake was gradual rather than rapid. Delegates reported that the reasons for the significantly greater adoption of thematic investments were due to:

- Support for sustainability.

- For diversification.

- Participation in the ‘New economy’.

- Government support globally for ‘green’ issues.

- Increased promotion amongst the banks and wealth management firms.

- Keen adoption by the NextGens, who are concerned over the future.

- Themes as satellite strategies for more exotic exposures.

- Alignment of macro factors with investment strategies with a long-term view.

- To capitalise on long-term economic trends.

- Helping to generate alpha at scale by focusing on investment opportunities in hot spots where a significant amount of capital can be deployed.

- Greater availability of thematic mutual funds and ETFs.

- ESG adoption at governmental, multilateral and leading institutional investors levels.

- The increased media coverage.

- Greater upside, providing the risks are managed appropriately.

- Appealing to investors’ personal values and beliefs.

- The need to find personal value as well as financial value.

Hubbis: What are some of the key themes that appeal to Asian private clients?

- ESG

- Thermal and green energy

- EV

- Technology

- Healthcare

- Cryptocurrency

- Environmental related

- New economy

- AI, ML and digitalisation

- Robotics

- Climate Change

- Tech, FinTech, BioTech, AI

- Clean energy, clean resources

- Agri-Tech

- Biotechnology/Pharma

- Greater China

Expert Opinion - Stephanie Leung, Director and Head of StashAway HK and Group Deputy CIO: “Demand is definitely on the rise for thematic investing. The convergence of technological advancement in both software (e.g. machine learning, crypto, virtual reality) and hardware (e.g. battery technologies, 5G, GPU) enables very disruptive advancement and consumer use cases across industries, and investors are looking to take advantage of the early stage in the S-curves.”

This is no marketing gimmick that will disappear before our eyes

A guest stated that this is no fleeting trend and that many of his Asian private clients are overloaded with fixed income, especially fixed maturity products or active global income funds. “But they need to look at how and where they are exposed to global growth,” he opined. “And that is where the RMs and advisors can have some meaningful discussions.” However, he added that these thematic allocations are only part of the conversations, only a portion of the portfolios.

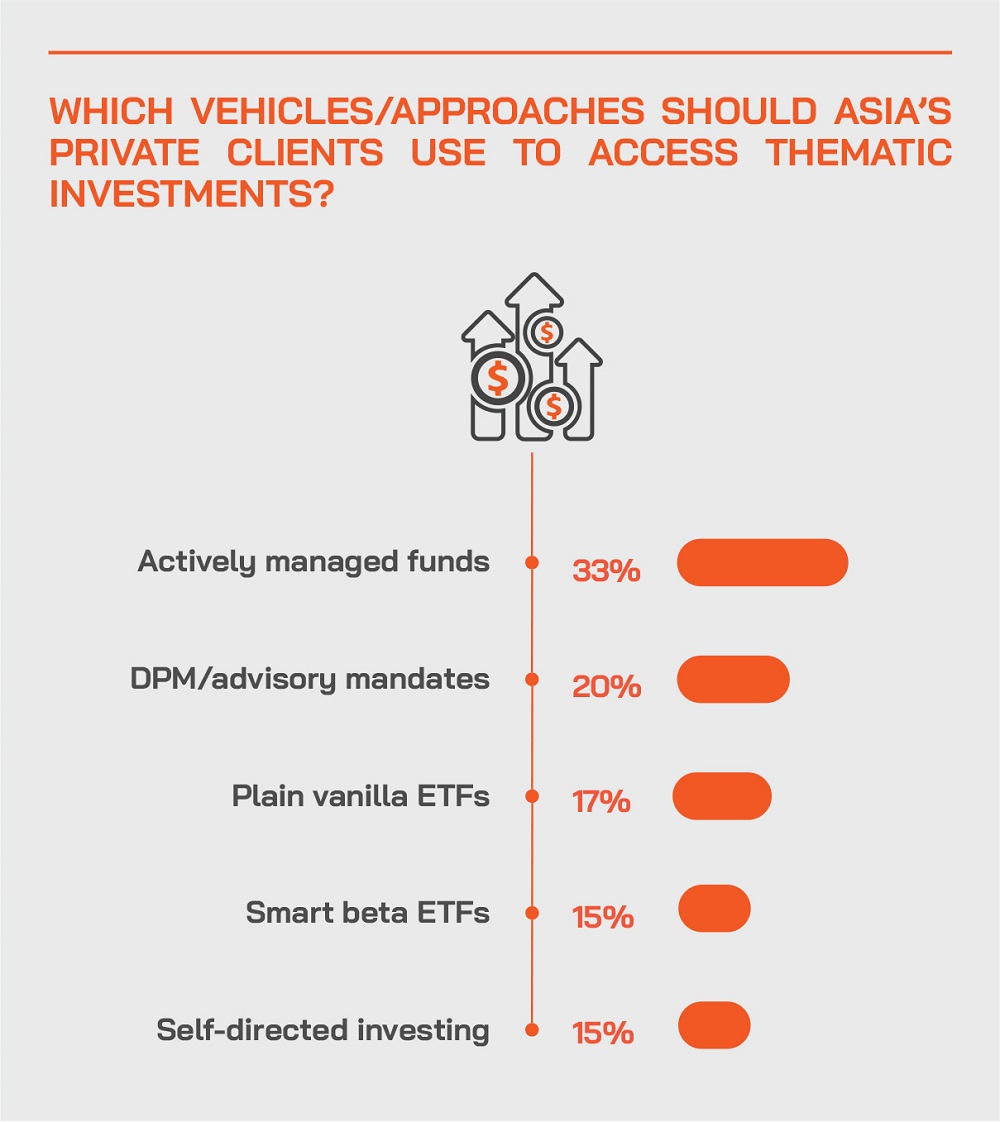

ETFs offer private clients an expressway to Theme City

ETFs, one expert reported, are ideal for private clients of all categories, but the major institutions and sovereign wealth funds driving much of the headline ESG type investing do not tend to use ETFs. He explained that thematics in terms of megatrends such as clean energy, for example, still remains relatively small as part of their vast ETF pie, at just USD35 billion roughly, a trifle compared with approaching USD9 trillion across the platform’s active and passive funds as a whole.

Another guest noted that for their core risk portfolios offered to private clients of all wealth categories, they use ETFs to gain easy and low cost and liquid access to particular asset classes and themes.

ESG versus thematics

The difference between ESG, as opposed to thematics, this same expert observed, is that thematics from his viewpoint will always be more interesting to the private banks and wealthier clients who are looking for an investment that they don't necessarily have to trade in and out of but should make economic sense over the next 20-30 years, whenever they're looking to retire. “ESG,” he explained, “is slightly different in that a lot of leading institutions, pension funds and so forth are going to be mandated to buy ESG type products, or at least have some kind of green screening when they buy equities or fixed income or whatever it might be.”

Asia’s leading funds are likely to drive ESG ahead, as has been seen in Europe

Accordingly, he added, when this is being driven by governments and leading bodies, as has been seen vividly in Europe, the trend is magnified dramatically, and this is now expected to happen in Asia. “That is yet to come out here,” he reported. “I think investors are preparing for it, banks are preparing for it, but have not necessarily pulled the trigger quite yet.”

Themes are multi-year, and often also multi-decade strategies

A guest pointed out that some of the best thematic plays crystallise supercycles such as AI, robotics, or healthcare technologies that evolve over decades. “There might be shorter-term volatility,” she commented, “but these are long-term trends and therefore, you need to assess the risks with the right time horizons.”

Adding ‘factors’ to thematics for an advanced protocol

The same expert remarked that factor investing was also fashionable some years ago, and that factors such as momentum, value, and quality could be overlaid to key themes to help investors, for example, thinking about how the macro environment would impact the factors underpinning many of the thematics, and thereby help assess risks and allocations and timeframes.

Be careful not to get carried away

A guest remarked that it is all too easy to get carried away, and that stock picking through thematics can be risky if the company in question does not achieve what everyone had hoped for, and therefore funds are a better approach. But even so, the time horizon must be considered carefully, allocations within the portfolios well judged and careful monitoring of performance and key trends should be ongoing. He explained that the private clients tending to take a longer-term view are those wealthier individuals and family office type clients, whereas other investors can tend to trade in and out, sometimes too rapidly and with too much emotion and insufficient patience.

Thematics and the active versus passive debate…

An expert explained how the passive versus active discussion where passive was winning on a fund flow basis globally has suddenly totally changed because of ESG. “Because suddenly, investing in the S&P 500 or the Russell 2000, or just broad indices totally washes over the fact that the subcomponents of these indices can include good and bad companies from perspectives such as ESG, sustainability or SDG, net neutral, and so forth. This is awesome news from an active manager’s perspective.”

Baking ESG into the institutional investment framework – a highly visible trend

Additionally, this same expert observed that determining the E and S and G impact and validity of individual companies translates into a different cost of capital for equity or debt and can create distinct advantages for carefully selected companies instead of the index type approach.

He offered the example of winning a USD500 million mandate from the Asia Infrastructure Investment Bank against 23 other managers, where the key difference was their ESG team that won the day. That, he said, is partly because for-forwarding a decade, for example, every investment process, every portfolio construction process, every workforce, every activity of a company will have to acknowledge ESG elements in

“Leap forward 10 years and ESG will be a ‘baked-in’ standard in the majority of companies, especially in the publicly listed markets,” he projected. “Bottom-line is that this is all very good for active and we are living that right now.”

But passive is still ‘winning’ in a world of easy money

Another guest pointed to the massive fiscal and monetary stimulus packages around the globe and said that money is so easy that the flows into passive strategies such as ETFs have been made so much easier, therefore helping to flood the markets with liquidity. He said that if there is a return of inflation, higher rates will emerge, and volatility will rise, creating more support for active strategies.

The materiality of ESG risks must be identified and clearly recognised

An expert highlighted how there is immense and growing materiality in terms of quantifiable ESG risks, or rather the risks of not achieving ESG principles and targets. This, she said, is why due diligence is essential, as relying solely on ESG ratings – none of which are standardised around the world - is insufficient.

“For us as a house,” she explained, “we do a lot of probing as well into really understanding, firstly, the concept of materiality, and second, the breadth and depth of which some of these ESG factors are being incorporated, and also the expertise of the partners that we work with. Do they truly understand the tension points between the different E, S and G factors?”

Learning, education, training – all essential

A guest highlighted the vital importance of training bankers, advisors and therefore the clients on all these issues and standards, noting that many clients and bankers comment that all the different terminology that comes out from the sustainable investing space is difficult to comprehend and then navigate. “We did some research last year at the height of COVID-19,” she reported, “and what was interesting that we found was that while interest levels were high, actually apprehension levels were equally high in getting kind of started in the space. We, therefore, feel it's important to help the bankers and clients obtain a very good understanding.”

Themes of the day – Life on Mars?

A guest joked that the best new thematic idea might be a new residential real estate investment on Mars, but that as yet, there was no specific strategy for that. Joking apart, he warned again about fear, greed and boredom, noting for example, that he himself had bought into ARKK Innovation Fund and that as he spoke, it was down about 25% from his purchase price.

With that said, he advised investors to have fun with thematics but “for goodness sake” to make sure they adopt them as part of a core satellite approach, with the solid core of the portfolio that they can truly rely on and then allocate a portion to themes and ideas, with sizing at the level where they are not inducing anxiety over their holdings.

Know what you are getting into, monitor and don’t make assumptions about the future

Another expert advised that whatever strategy investors buy into via ETFs, they should assess exactly what companies are included in the fund, how the ETF is rebalanced, whether there is a market cap weighting on particular stocks, what the fees are and s forth. He advises exposure to equities to express thematic plays, but also to be careful to track both the quality of the themes and the robustness of the ETFs or other vehicles used.

Plenty of opportunities in clean energy, water, foods under the banner of ‘sustainability’

A guest highlighted their preference for the sustainability space, focusing on four big long-term themes around the energy transition and electrification, water, sustainable foods and the circular economy.

The final word – keep your perspective

Thematic strategies should be included in any robust portfolio that is well-positioned for the future,” an expert said, on closing the conversation. Thematic investing, he said, is here to stay, participate, but keep a sense of perspective and do not become too preoccupied with it.”