The Hubbis/CREALOGIX Survey on Conversational Banking – Wealth Management in the New World

Sep 21, 2020

Are we emerging, albeit extremely tentatively, from global lockdown, or are many of the leading economies on the cusp of new lockdowns? In Asia, will some semblance of normality return by the end of 2020, or, as appears more likely, will we all need to wait until sometime in 2021, or until workable vaccines materialise? Those are imponderables, but what is becoming clearer is that, in practical terms, conducting the wealth management business will likely not be the same for some time to come, and a new normal could well mean that remote communication and transacting with Asia’s private clients – from the mass affluent to the ultra-high-net-worth – is here to stay for the foreseeable future. Hubbis, along with our exclusive partner for this endeavour, CREALOGIX, recently conducted a survey titled ‘Wealth Management in the New World’ to explore the current and potential post-pandemic environment, gauging the digital health of the incumbent private banks and other financial institutions to determine their ability to survive and thrive in wealth management in the years ahead. Has the use of digital identity applications eased and speeded up the remote KYC/onboarding process for clients? And at the same time, is it meeting practical cyber-security and privacy challenges, as well as compliance requirements? Has the wealth community embraced and absorbed digital tolls and enhancements well enough to really enable them to truly deliver products, solutions and advice remotely, and what needs to be done amidst the ongoing social distancing demands to adapt platforms to the potential landscape of the post-pandemic world? Are the wealth management providers coping best with the wealthiest clients who are already embedded in relationships, while perhaps struggling to win new wealthy clients and new mass affluent customers?

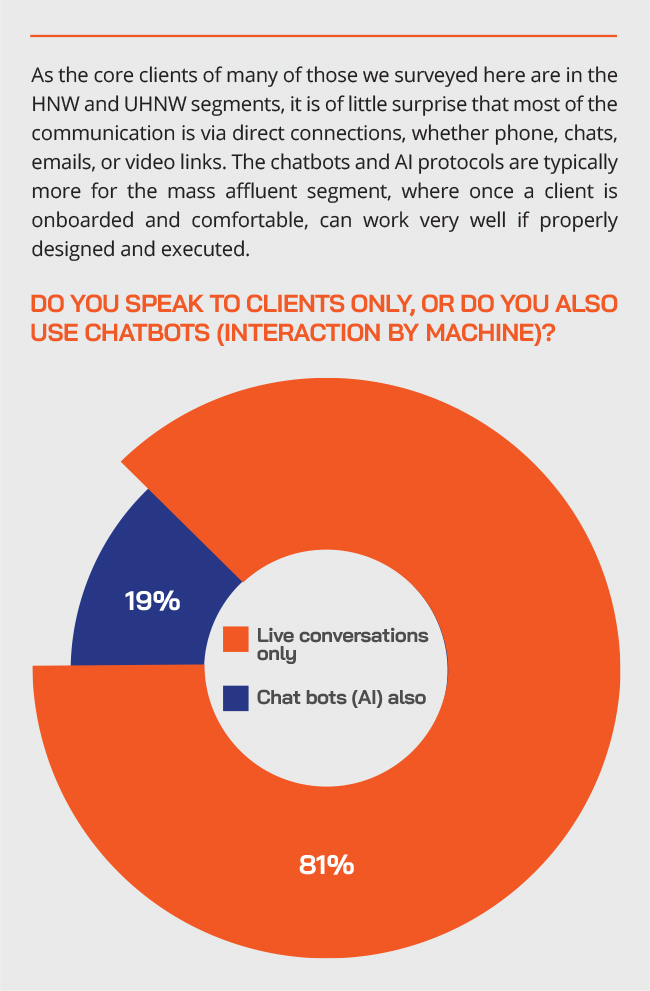

The Covid-19 crisis has and will continue to impact and change the way the wealth management process is conducted, not just for retail clients, but the full spectrum of client segments, including UHNW. Clearly, like most industries, digital and particularly cloud solutions will be prerequisites. However, the investment and advice workflows will also need to change significantly with both the end client and the RM being given more tools to support the advice process.

Step one – get it right from the start

As the world will not be the same after the pandemic, the right digital strategy is even more crucial to the survival of businesses. Financial institutions and banks must be innovative and accelerate their digital transformation to enhance their end customer proposition and stay ahead of their competitors.

There is a well-acknowledged Asia-wide acceleration of digital solutions. This is, or at least it should be, a further evolution and acceleration along the digital journeys already underway, it should not be actually a sudden or entirely unexpected revolution. The path towards digitisation has been clear for some years already; it is simply a question of the pace and effectiveness with which this is embraced.

Refining the mission(s)

The question today is certainly no longer if digital is top of every wealth manager’s strategic agenda, but rather how far can digital tools be leveraged to strengthen their value proposition and deliver the optimal customer experience to their clients.

Where precisely along this chain will digital solutions be in even greater demand in the months and years ahead? How are the banks improving their digital platform and capabilities? How can banks and wealth managers serve the mass-affluent segment better and improve the proposition? How must they evolve their operating model? What’s their strategy to build the wealth business? How can they increase profitability and reduce cost? How can they build digital solutions that see the clients’ needs first and then work backwards from there to implement the optimal outcomes for all parties? Can the local players, boosted by digital, compete more effectively against leading international banks and firms?

The current immersion in remote working, virtual events in the form of webinars, and socially distant connections to colleagues and clients are, many would argue, an expedited version of a trend to a new norm that had pre-existed this virus, as financial institutions adapted to deliver financial services to as broad a demographic as possible, and as seamlessly as they can, focusing both on internal efficiencies and the end-user experience.

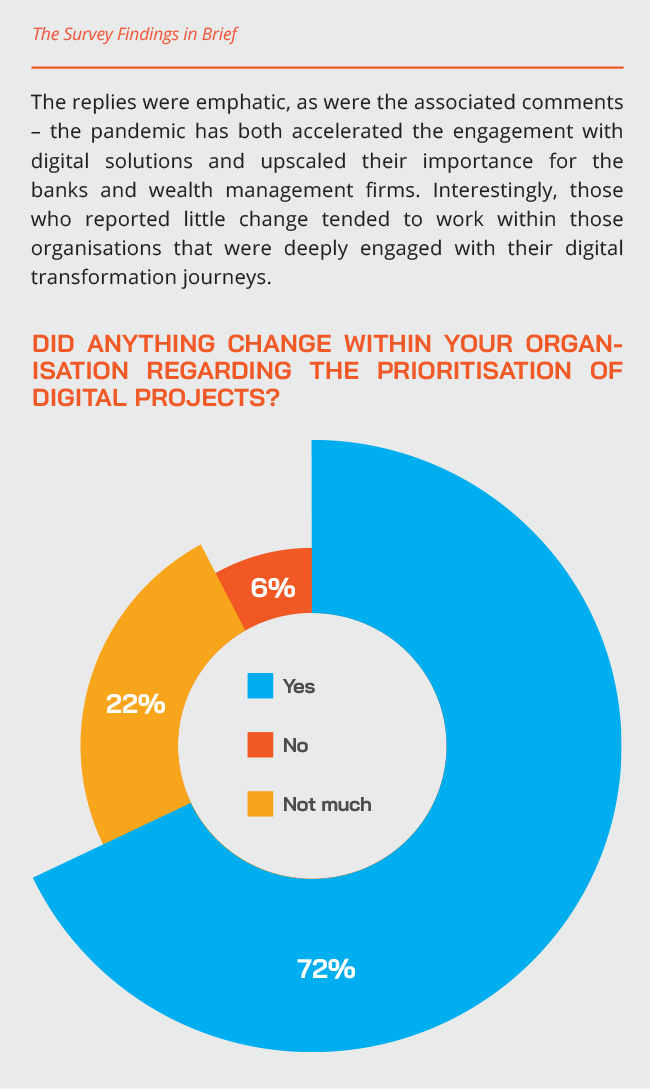

The Survey Findings in Brief

There are several underlying necessities that can be considered crucial in this new norm and vital as part of the digitalisation agenda. One need is around driving the mobility of communication to customers, whilst another is about allowing the financial institutions the flexibility and predictability they need to operate in an ecosystem and thereby providing the ability to interact and to achieve full interoperability.

Bringing the new normal to the door

What the pandemic has done is, therefore, to bring a new normal nearer by accelerating what has already been ongoing from the transformational and technological perspective. And it is not just about adopting technology, it is also about the cultures and mindsets of institutions, to ensure that the industry understands what they are trying to achieve and that they are able to fully operate in the forthcoming environment, by constantly digitalising for the future.

In other words, a vital key is the corporate culture and mentality - suddenly the leaders of the private banks have been forced almost overnight to more clearly see the challenges in full focus for themselves, and as a result are more clearly realising the true value to be attained at the end of this process, even if it is still painful to reach that point.

Seeing the opportunities

Then it becomes more about how to capitalise on the virus-enforced environment today and to make sure that once we all advance into what will be the new normal of the post-pandemic environment, that they do not go back to the old normal, that they make sure they continue to build their digital infrastructure, keep focusing on internal enhancements of processes, skills and capabilities, and keep a laser-guided focus on the end client and their evolving needs and expectations.

To achieve some or all of these goals, the banks must have the infrastructure required to support a digital transformation of the scale required, and also a clear vision in place for the journey, which cannot take place overnight, it takes time. Many of those we pooled here also believe that there had, in any case, long been a huge need to accelerate and broaden digital transformation.

Leaders by example

Some were well advanced, well before the pandemic hit. Those banks and organisations that have been systematically upgrading their infrastructure, their API layers, their database systems, creating microservices that can be reused much more effectively, no matter what the form factor, whether it is on the phone, whether it is on a smart-watch or whatever the form factor might be, it is those organisations that have been consistently investing in the modernisation of the technology stack, so it is they who when the virus struck had a greater ability to accelerate their digital transformation than any organisations starting late, or worse still, starting right now.

Your battle to win or lose

Technology architecture is a long-term build; it is far from a quick fix. For anyone that is well behind the curve, this crisis has been a real wake-up call. For any of the incumbent banks who are behind the curve, they must be ready for the new age; the battle is essentially theirs to lose.

Expert viewpoint: Karsten Kemna, Asia-Pacific Managing Director, CREALOGIX:

Hubbis: What kind of digital projects are now a priority? And why?

“The role of RMs is changing (less direct interaction, more processes require digital automation), and therefore the RMs need stronger digital tools to manage relationships and drive engagement. At the same time, end customers expect a better mobile-first experience due to the mobile phone being the main tool for interaction.”

Hubbis: When you consider how wealth management services are delivered to your clients, what will be some of the permanent changes as a result of Covid-19?

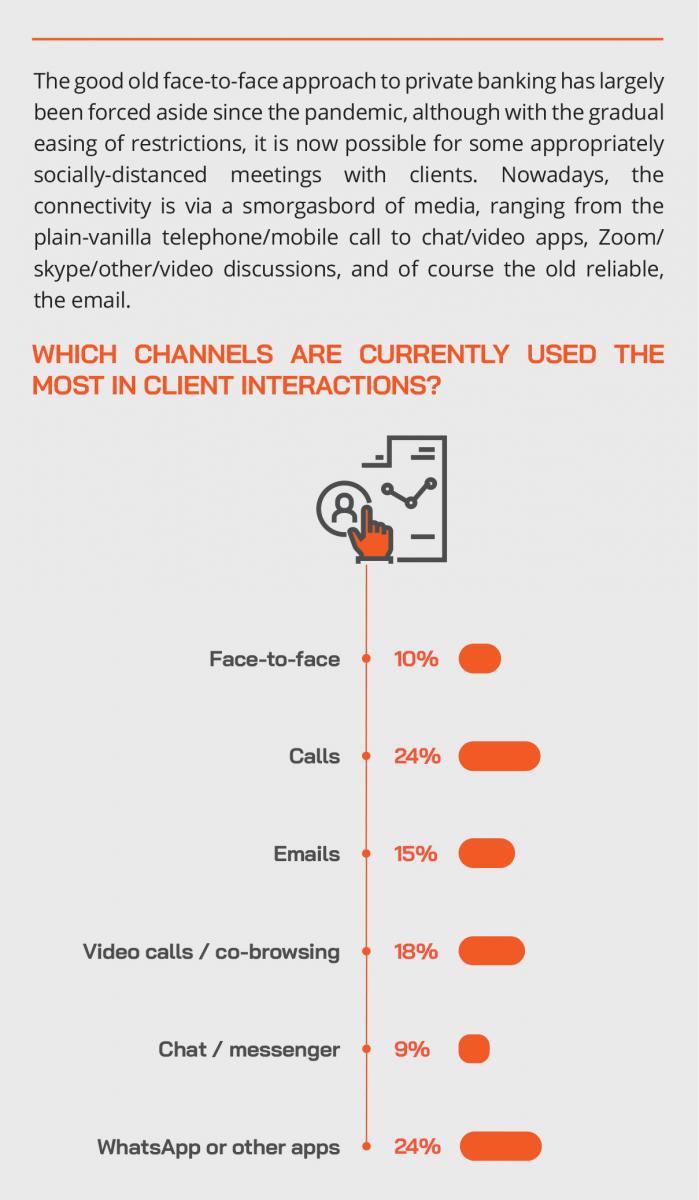

“It is more important to have the right mix between digital and face-to-face interaction with your customers, considering that personal meetings are still difficult to facilitate, but people have gained various new experiences with overall digital solutions during the crisis time.”

Yet for those who are ahead of the game of true digital transformation, they have been able to dramatically upscale digital connectivity, remote advisory and remote transactions across the board for all categories of their private clients.

The agility of some of these forward-thinking incumbent players, their ability to continually boost their digital offerings and expertise has been years in the making. There have been large banks in Singapore that have been showing their peers the way forward, with a deep embrace of innovation and a profound cultural engagement of digitisation throughout every nook and cranny of their infrastructure and DNA.

Seeing the continuum of wealth management

The digital revolution also needs to take place right from the start of the client relationship. Digital identity solutions, for example, help significantly with remote onboarding without the need for people to walk into an office. There are or course hurdles and pitfalls on the road to achieving this seamlessly, but as long as the financial institutions adjust to this new reality, with very rigorous rules around digital signatures, remote onboarding can take place.

Due to Covid-19 hindering the face-to-face aspect of the wealth management experience, an effective all-in-one platform for easy access by clients is an absolute must. As such, these banks will need to adjust their corporate mindset to cope with a smooth transition to a digital focus. It is vital to enable end to end digital processes, if not already implemented. Firms should also try to understand the needs of its end clients/employees before implementing new digital enhancements; this will help to ensure the new technology will not turn into a white elephant in the room.

Views from the Wealth Management Market

Hubbis also asked those we surveyed here to offer some brief insights into the new world of digital transformation amidst the pandemic. We have summarised some of those insights here.

Hubbis: What opportunities and challenges has the Covid-19 pandemic highlighted for you?

- “Opportunities: More time to spend on investment product research. Challenges: Getting face time with clients and potential clients. Challenges include the difficulty of seeing clients in person.”

- “After Covid-19, banking will be much different than it was pre-pandemic. The change in the way people bank, the future of work, the use of modern technology and the value of brands will all depend greatly on the time it takes to settle on a 'new normal'. A look into the future provides a good foundation for what needs to be done today.”

- “We will see more working from home, smaller offices, more hotdesks, continued compression of fees, faster digital evolution, and a rise of e-solutions for clients. More virtual meetings and presentations.”

- “We have been learning how to better connect with others in virtual situations.”

- “I would like to think and hope with lessons and new things learnt that are workable digitally during this period, and management would be able to streamline processes and procedures more efficiently and digitally.”

- “We have embraced digitalisation and done well, but it has been very challenging to access new talent due to the lack of personal interaction.”

- “The contact with clients has clearly changed, with client servicing now much more digital than personal.”

- “Looking at the business from the client’s perspective, customers see interest rates so low now that they are encouraged to seek more investment opportunities. Although the news out there dampens the spirits, the global QE measures and the US markets’ strength have led to a vibrant, active wealth management market, with digital and remote working, advice and execution possible throughout this situation.”

- “Challenges include limited face to face meetings, real concerns amongst clients about their investments falling again due to the pandemic, adjusting to overuse of Zoom/Teams/Webinars as a way to connect, a lack of opportunities to host presentations with clients and potential new clients. Opportunities include wider audiences for webinar presentations, digital processes have significantly improved for account opening and other transactions.”

- “Working out of the office has been a change, and it was all rather sudden. We had to learn new processes for non-Face2Face meetings, but video conferences are quite efficient, even if they don't feel the same.”

- “Being in client-facing roles while managing the operations, Covid-19 has forced a new perspective on how things can be done. Gone, perhaps are the times when competition drives you to make physical trips to meet clients, use technology for communication instead. Many clients, at least from our end, have seen the advantages, for example, as we are able to showcase a lot more data and information including Bloomberg screens to illustrate situations and ideas to them. This may change or accelerate a lot of trends.”

- “Opportunities include digital banking, online trading systems/protocols, and virtual conferences are amongst the growing opportunities during this pandemic. But of course, challenges include the travel ban and social activities which affects the client relationship enhancement.”

- “I think this pandemic has made the impossible possible, especially evolving the working environment to go online/digital, instead of having to be physically in the office. We definitely see the increase in online business and also the creativity of people.”

- “We see greater awareness of the need of the value of wealth management.”

- “We see the opportunity to accelerate digitalisation, which was moving at a slower pace before Covid-19. As to challenges, it is very difficult to get all stakeholders together speedily and building coherence.”

- “Remote contact with the client creates difficulties, especially in new relationships and building new clients, although for the existing client relationships, they appear willing to spend more time for discussions, so it is positive for mature relationships. I can see more revenues generation by senior bankers this year.”

- “Clients are encouraged to sign up to online banking access but some older clients are rejecting or not comfortable with digital technologies.”

- “As to opportunities, this hiatus has created time for clients and prospects to think about their investments and their future lifestyle and needs, as these are so important to the way we are going to live the rest of our lives. The world is becoming less stable so there are needs and opportunities to build some more security closer to home, rather than more offshore money and wealth management.”

- “It is now easier to communicate with people digitally, but wealthy people are still very wary of authorities tapping lines, internet usage, and so forth, so this is not an ideal situation. However, people are getting used to the idea of receiving digital information (or looking for information themselves).”

- “We see more frequent communication with clients, as clients have more time and do not travel really, so they have time and inclination for our conversations.”

- “For the clients, it is easier to reach leaders of the banks and wealth management firms via remote means. But it is harder to build new or deeper relationships as ‘you cannot Zoom a handshake’.”

- “Whilst we see opportunities to enhance our existing WFH arrangements, it is challenging to maintain regular, scheduled patterns of behaviour.”

- “There is a major opportunity to expedite the digital transformation such as digitisation of manual processes so that much more can be done remotely. However, the challenge is to implement 100% remote working and monitoring of employee performance. Another big challenge is for IT Security, especially mitigating in data breaches for employees working remotely.”

- “At the moment, the business is good as clients have been re-analysing and re-calibrating their portfolios. The challenges are that face to face meetings have decreased, although online meetings has increased and have created some opportunities for more online conversations and meetings.”

- “It is difficult to overcome the need to obtain signatures on documents, arrange in-person client meetings and travel within the region.”

- “The opportunity is greater ability to meet client conveniently online anytime, anywhere, and the positive availability of products to be sold remotely/online. But challenges include the IT technology gaps, and grossly reduced social interaction.”

- “It is difficult to connect to colleagues, particularly when aiming for idea generation sessions. Difficult to building relationships with prospective clients. But opportunities include becoming more adept at social media.”

Hubbis: What kind of digital projects are now a priority? And why?

- “Real-time, up to date and on-demand client portfolio generation (especially for clients with multiple asset custodians).”

- “Video conferencing.”

- “Signature verification and authenticity, very important for domestic and international clients.”

- “Customer Onboarding and KYC are essentials.”

- “We began digitalisation our internal processes before the pandemic, but this is now accelerated.”

- “We are focusing on robo-advisory.”

- “We have a greater focus on budgeting and savings advice via AI to help grow investible assets.”

- “We need to work on improved documentation for account opening and all the relevant servicing needs via digital. We need more relevant webinar briefings to attract larger audiences and to reduce costs.”

- “We are working on CRM, financial planning tools, process improvement; all these areas are more relevant since we are working separately.”

- “The online trading system has risen to a critical level, and there are ‘must’ projects required that help resolve the inconvenience caused by WFH and to help keep the business running as smoothly as possible, with the least interruption.”

- “We are focused on the online signature of documents.”

- “Cybersecurity is a vital factor.”

- “Online access and digital banking are top priorities for most of the banks, especially related to order placement and statement access.”

- “We want to boost market view on-the-go via the website and market view on mobile apps.”

- “Process digitalisation remains the number one priority, and all other efficiencies stem from this, in particular addressing skill/resource scarcity, so digitalising a highly personalised communication process is the next priority.”

- “Our areas of focus include mobile Apps for clients, IT security solutions, workflow and RPA implementation, the digitisation of documents and signatures.”

- “We focus on new online onboarding, new e-service, and the new mobile platform mainly to help convert clients to transacting online.”

- “Key areas as non-face to face advisory and sales of financial products, so we need to be able to have a digital mode to communicate with our clients, and that mode needs to be efficient and effective.”

- “We focus on online client engagement and advisory tools, both a priority as we are conducting more online meetings.”

- “We are using Microsoft Teams more extensively to maintain a collaborative approach.”

As products are nowadays the simple fix, it is fair to assume that banks would be looking to enhance their platform’s functionality during this pandemic period. Local banks and wealth management organisations in Asia are also adopting digitalisation at an ever-faster pace. These local firms are already quite advanced in terms of capabilities and their digital journeys, but to more effectively compete against international banks and firms, local players will need to focus on how to better monetise their new technology.

Keeping things secure

Security is also a key consideration. The working from home (WFH) environment creates new challenges, creates new threat vectors, creates new abilities for fraud, unfortunately. Yet there are the means today to digitally detect patterns and anomalies, so for any organisation in the business of managing other people’s money, this is also a critical area.

Regarding this absolute necessity for security and privacy, the basics of hygiene factors demand that an institution needs to have technologies and processes in place to ensure that the data that they collect is properly safeguarded, properly used and that then is essential for building the trust with the customers, so they see that value in releasing the data and sees that the institution is trustworthy in its handling of the information. Then you move into the landscape of being able to collect more information, provide better insights to the customers and better and deeper relationships ensue.

Stay ahead of the pack

It is also entirely up to the incumbents to be competitive, to stay ahead of the chasing pack of new entrants, many of them digital native companies or empowered predominantly by technology. As these new and future competitors come in, so it is essential for the incumbent wealth management competitors to be relevant, stay competitive and to constantly identify the opportunities and capitalise on them.

Banks can most certainly improve their customer service by adopting innovative digital technologies. With new competition on the rise, an enhanced digital journey leading to greater customer engagement seems to be the most powerful strategy to win the race.

The challenger banks are leading the way in reducing the number of steps required for many aspects of their service yet still maintaining compliance and rigorous risk controls. Similarly, with the HNW space digitisation still has a considerable way to go. For example, the standard approach for execution across all asset classes in the institutional space globally for many years should be more widely adopted by the private banks in Asia. More energy and time should be spent by those private banks on servicing clients and not paperwork and antiquated manual execution and order management methods which can so often lead to slippage, time-wasting, errors and ultimately cost to the client.

Client first and last

Undoubtedly the pandemic has greatly accelerated the adoption of or engagement with digital solutions for the region’s wealth management community. he replies to our survey showed clearly that there is no doubt that putting the client at the forefront of the digital journey will produce the best results.

We know from the many reports Hubbis has researched and produced and the numerous live and remote discussion events we have hosted that most HNWIs in this region would prioritise innovation, improvement in services, and their client experience, while the majority of the private banks have been digital a high priority. So, the question is no longer whether digital is on top of the strategic agenda, but rather how can digital tools be leveraged to strengthen their value proposition and deliver basically the customer experience that their clients need and really require.

The digitalisation taking place and the resulting accessibility across the board will likely increase the offering for both mass affluent and HNW clients so that they are on equal footing. From there, it will be up to the individual firms to differentiate and allow their HNW and UHNW clients to feel special.

Transparency and accessibility

With digitisation, the provision of information and products will be more transparent and accessible to a broader range of clients. The growth of mass affluent individuals has been very significant, especially in Asia Pacific, and firms have increased their product offerings and services to better cater to this targeted segment, including robo-advisory delivery.

The players also need to make sure there are enough good quality RMs around and to make use of these RMs remotely for the clients that really have money to invest in order to make more money for the institution. That means for mass affluent clients the delivery must be more on a robo-advisory level, to be able to automate as much as possible, while the institutions focuses its quality people where the big AUM is. With technology, the banks can indeed create a good mix there between the mass affluent delivery and the HNW and upper-end personalised delivery.

The final word

Finally, we all know there is no magic formula to wealth management or to the challenges of digitisation. We also know that whatever digital advances are available and grasped by the industry, that is it the old values of relationship, of advice and consistency that remain of paramount importance. Those who are most deeply engaged with digital transformation know that wealth management will continue to revolve around the client relationship, the dynamics of client interactions, personalised content and insights, but in the new world ahead, all these elements of the business will be enabled and enhanced by digital solutions, without which any incumbent or any would-be competitor will simply fall away.

The CREALOGIX Group – a brief introduction

The CREALOGIX Group is a multinational digital transformation specialist and a Swiss FinTech Top 100 company, as well as one of the market leaders in digital banking. The firm develops and implements innovative FinTech solutions for the digital bank of tomorrow and while its roots are coming from the wealth management industry, it also offers digital solutions for both retail banking as well as corporate banking/SME type environments. The firm’s focus is on the evolving needs of banks and end customers’ needs for digitalisation in a secure and personalised way within a comprehensive user experience.

The CREALOGIX Group is among the global market leaders in digital banking in Europe, Asia and beyond. According to its literature, banks can use their solutions to react to evolving customer needs in the area of digitalisation, enabling them to hold their own in a very demanding and dynamic market, and to remain one step ahead of their competitors.

And CREALOGIX has a broad suite of state-of-the-art solutions for not only wealth management, its traditional business, an area in which the firm believes it will be able to compete highly effectively in Asia, but also with a stronger push for retail banking and corporate banking solutions going forward. Starting from a small but healthy customer base in Asia, with Kemna on board, the company is aiming to expand rapidly.

The group, founded in 1996, has around 700 employees worldwide. CREALOGIX Holding AG (CLXN) shares are traded on the SIX Swiss Exchange. The company counts more than 550 banks worldwide as customers in countries such as Switzerland, Germany, Austria, the UK, Spain, Singapore, Hong Kong, Thailand and Saudi Arabia, and CREALOGIX has carried out more than 1,200 installations for its customers and has a wealth of valuable experience. Offices are located in most of the key countries where the firm has an extensive client base.

“We provide banks and other financial organisations with reliable, and forward-looking support for their digital transformation journey, and we empower them to successfully master the inevitable digitisation of their business as well as offer opportunities and perspectives that actively shape the digital future of the financial world,” says Karsten Kemna, Asia Pacific Managing Director of the firm. “With the firm’s many years of experience and our unique, innovative solutions, we are your trustworthy partner for secure digital transformation.”

CREALOGIX considers Asia-Pacific to be one of its strategic key markets globally, and although only with a relatively small team of ten people on the ground thus far and a number of clients in hand, the firm is making far-reaching investments in order to strengthen the local organisation on a sustainable basis. Together with its vast partner network, the Swiss software company is addressing the growing demand for digital products in wealth management, retail banking and corporate banking in the vast Asia-Pacific region, where the firm sees huge opportunity ahead.

CREALOGIX offers a variety of FinTech solutions. The CREALOGIX Digital Banking Hub provides open architecture for open banking, the firm’s website explaining that its scalable, secure and highly modular software solutions and products enable banks to implement their digital banking strategy effectively, quickly and cost-effectively.

“When we talk about digital solutions,” Kemna explains, “we talk mostly about the front-end, for example, the mobile banking app or e-banking solution. We compete in two areas, the end customer using, for example, a mobile banking transaction, and also the advisory side, specifically in a wealth management situation, the relationship manager and what he would have on his hands in an advisory both face to face or remotely ‘virtual’, such as has been the necessity since this pandemic.”

Kemna clearly believes that CREALOGIX is optimally positioned for the challenges ahead. “Wealth management customers have high expectations of their bank’s products and services,” he observes. “At the same time, legal regulations and documentation requirements are becoming increasingly important for banks, while internationalisation and increased competition are reducing margins. On top, especially in certain parts of Asia, with a growing middle class and more mass affluent people coming up, the banks have to reconsider their strategy for these type of client groups.”

For wealth management, CREALOGIX offers a variety of products for online banking and brokerage, advisory and financial planning, client compliance enabling, RM dashboard, and hybrid advisory, with a target audience of both the end customers of the banks as well as the relationship managers.

An innovative software solution for the relationship manager of the bank which is designed for a digital wealth platform with standardised client service processes in a set of configurable, fully paperless workflows for face-to-face or telephonic advice or hybrid omnichannel consultation and sales of financial products. Client CRM-type data is combined with investor profiling and can be used for ongoing advisory and discretionary wealth management services.

And CREALOGIX Financial Advisory helps wealth management advisors to perform better, improves quality of service for end clients and reduces costs by benefiting from one standard paperless set of processes and information flow.

Managing Director Asia Pacific at CREALOGIX

More from Karsten Kemna, CREALOGIX

Publications & Thought Leadership

Digital Convenience in Wealth Management – Driving an Innovative and Personalised Client Experience

Latest Articles