Publications & Thought Leadership

The Evolution of Wealth Management in the Philippines in Times of Great Uncertainty

Nov 4, 2020

A group of local and international experts joined for the virtual Hubbis Digital Dialogue of October 29 to consider some of the critical changes taking place in the global and regional Asian wealth management industry, discussing in particular how the Philippines’ competitive landscape is changing, and how local firms can adapt to secure their future success, and how they will both compete with and/or partner with the international banks and even offshore IAMs/EAMs. The opportunities are certainly there to grasp – the Philippines has both a huge and a very young and fast-expanding population, the third youngest in Asia. GDP growth is robust, and the country is increasingly international. However, a key challenge for local private banks in the past has been the lack of products, which drove clients offshore, especially to nearby Hong Kong. Local private banks and the international competitors moving onshore are intent on offering an open platform and as many new products as the regulators might permit. Yet the reality is that regulation continues to lag the market’s needs, and the regulators continue to be rather cautious in opening the market to a wider array of products. This shortage of onshore investment products and solutions, as well as the shortage of onshore vehicles through which to access offshore assets are core reasons for more international banks moving onshore, either flying their own flags, or partnering with major local banks and institutions, rather than sticking to their old models of flying bankers in and out. The IAMs plying their trade out of Singapore and Hong Kong also see considerable opportunity in the Philippines and have been expanding their presence in tune with the market’s potential. Talent is another issue that must be addressed, however, before the wealth market can really advance. There is a shortage of wealth management expertise in every market in Asia, and this is especially true in the Philippines. How are the main competitors handling this shortage of talent, and is enough being done by them and by the regulator to encourage the industry’s development? Aside from investments, the life and health insurance markets are evolving there, and insurance companies diversifying their distribution models, enhancing the diversity of sales through their agents, through bank distributors, and increasingly via online FinTech companies. Technology is a major area of concern and potential, with the need to invest smartly and productively considered to be of paramount importance. Knowing what a bank or other institution is trying to achieve, and then formulating the appropriate strategies and selecting the right solutions and partners could not be more important going forward. The discussion was of course set against the backdrop of the pandemic, and a realism that it is not going away soon, yet with the hope of a more normalised world ahead. How then will the competitive environment unfold and will the wealth management community match and possibly exceed the needs and expectations of the rising tide of private wealth in the country? Our panel of experts produced a lively and engaging discussion on these topics and more.

A banker set the scene by explaining that the local wealth management market is relatively less sophisticated than many in the region, with most investors buying local products, including investment trusts, funds, investment management accounts, equities directly, and local and foreign bonds.

“The trends are simple,” he said, “with investors gradually in recent years having more interest in international investments. The major players are the big banks in the Philippines, the second key group are the asset managers, they are not affiliated with any of the banks, but they manage funds, then the insurers also offer asset management services. These three groupings dominate the local scene.”

For local Philippine peso-denominated products, the local wealth industry competes effectively, while for dollar or offshore assets, especially for the wealthier clients, there is limited product available locally, implying many of such investors then work with offshore banks and wealth managers, largely through Singapore and Hong Kong.

Collective investments

Another expert pointed to CIS, or collective investment schemes, that comprise life insurance, unit investment trust funds, and mutual funds. “CIS represent some 10% of the total pool of deposits here in the Philippines,” he reported, “and in pesos, roughly 80% of AUM. Filipinos still are in general largely conservative in their investment appetites, as fixed income bonds, money market funds, mutual funds and trusts dominate.” Another guest added that equities had performed reasonably well until 2020 and the pandemic.

Inclined to fixed income, risk appetite returning

Another expert commented that the market was developing reasonably positively when viewed from an international perspective. While the local investors have traditionally liked fixed income, there is growing appetite for equities, and some increasing demand for international equity, especially US technology and China.

He explained that depending on which scenario is taken for the Philippines, growth of between 4.5% and 7% per annum growth in wealth is anticipated, the population is young and expanding rapidly, the economy is becoming increasingly diversified, and although growth will stall due to the pandemic, there is much optimism for the future. “Maybe the biggest problem with Philippines is the national infrastructure,” he observed. “If that can improve and if the country can really be fully connected, that will be a game changer for the country.”

Rapid HNW growth

Another guest referred to a report from Credit Suisse and Wealth-X on the HNW population, noting that an estimated 30,000 individuals held at least USD1 million in AUM, and that the HNW market should grow by more than 9% by 2023 compounded growth. “Usually this kind of affluent client goes offshore to Hong Kong and Singapore for their investments, but with the growth of onshore feeder funds for international investments, there is much more opportunity for affluent investors to buy onshore.”

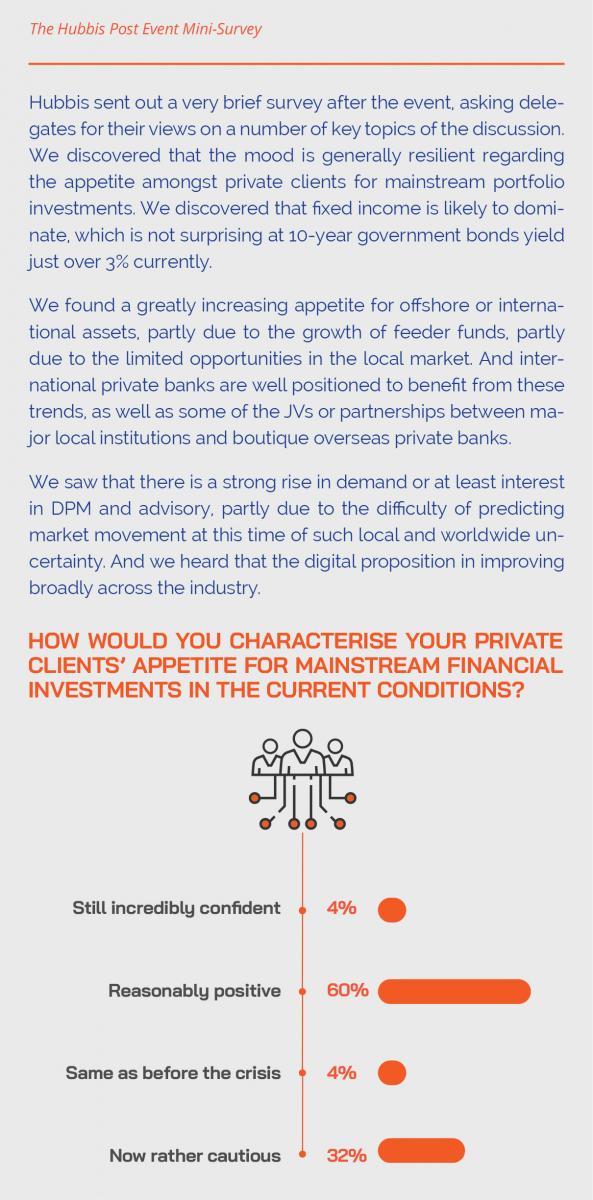

The Hubbis Post-Event Survey

Hubbis sent out a very brief survey after the event, asking delegates for their views on a number of key topics of the discussion. We discovered that the mood is generally resilient regarding the appetite amongst private clients for mainstream portfolio investments. We discovered that fixed income is likely to dominate, which is not surprising at 10-year government bonds yield just over 3% currently.

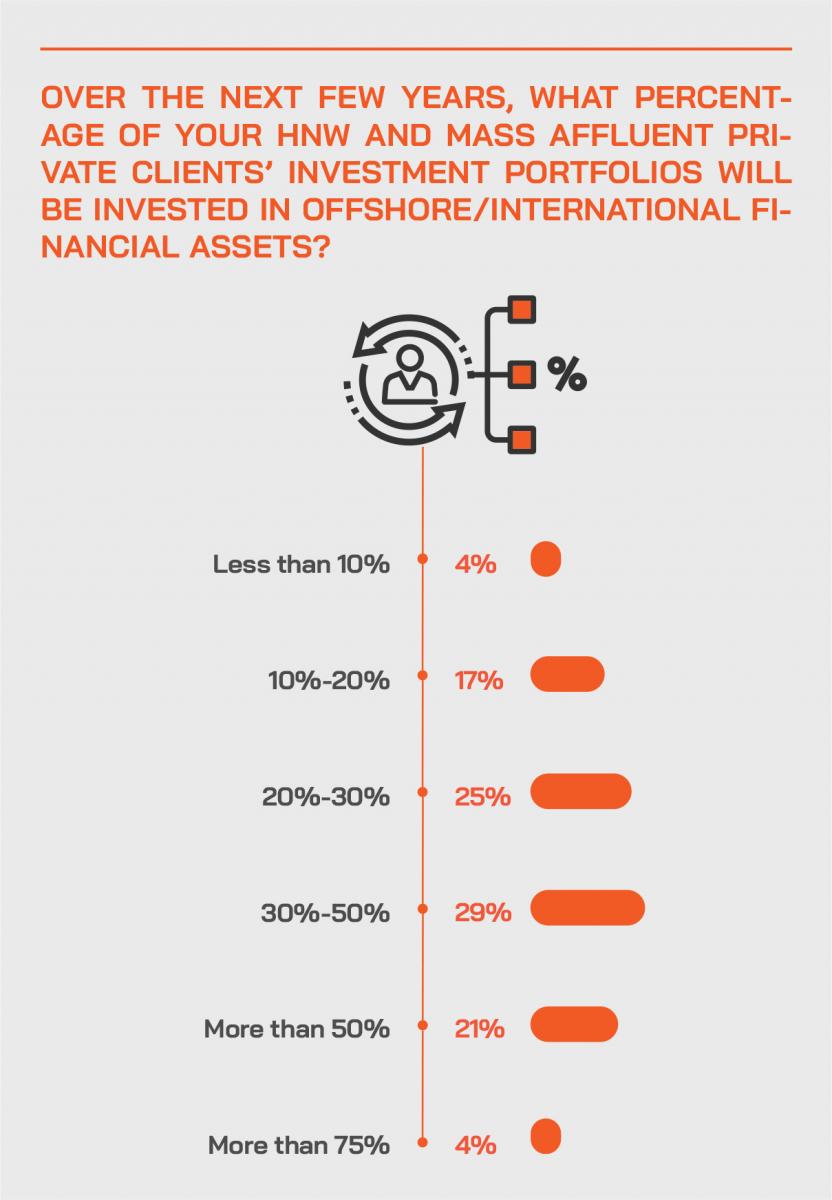

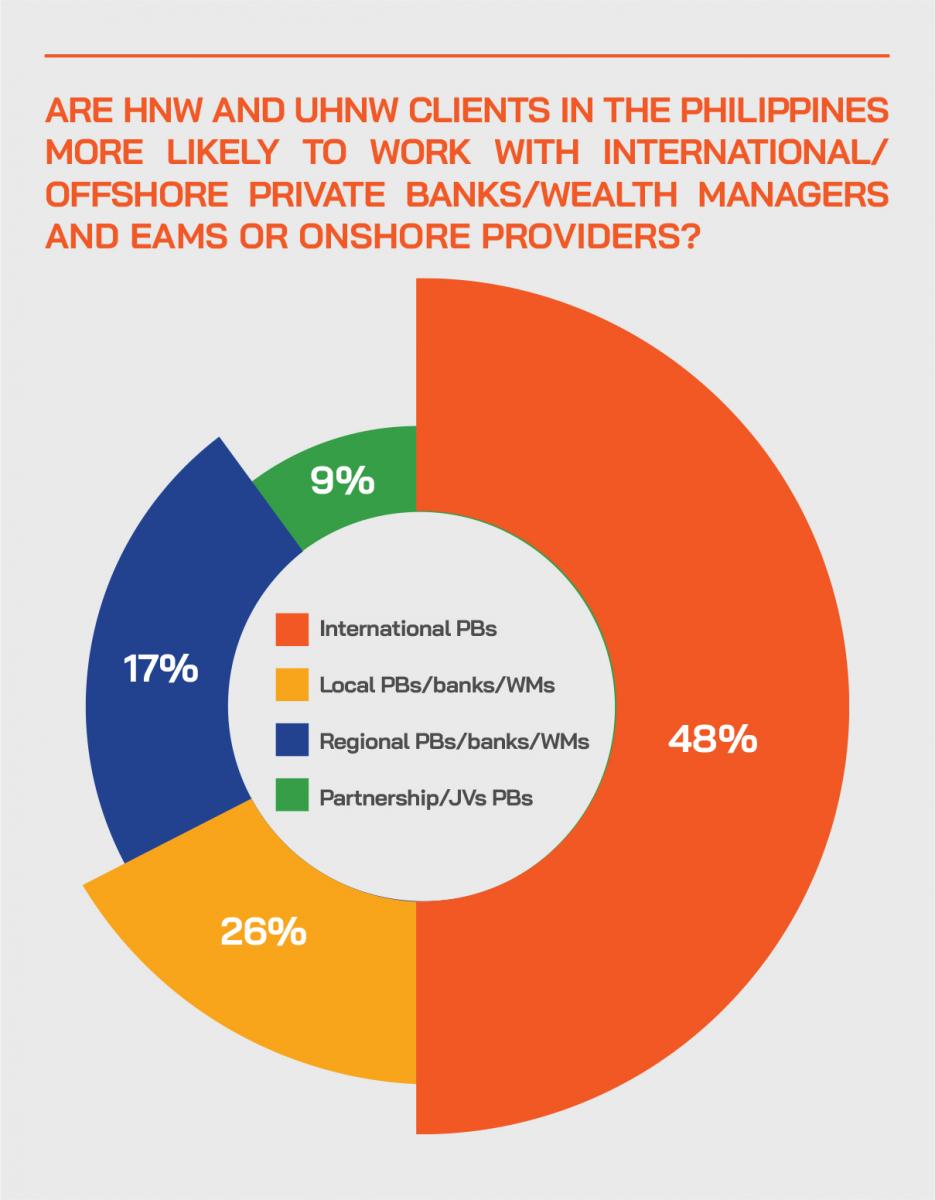

We found a greatly increasing appetite for offshore or international assets, partly due to the growth of feeder funds, partly due to the limited opportunities in the local market. And international private banks are well positioned to benefit from these trends, as well as some of the JVs or partnerships between major local institutions and boutique overseas private banks.

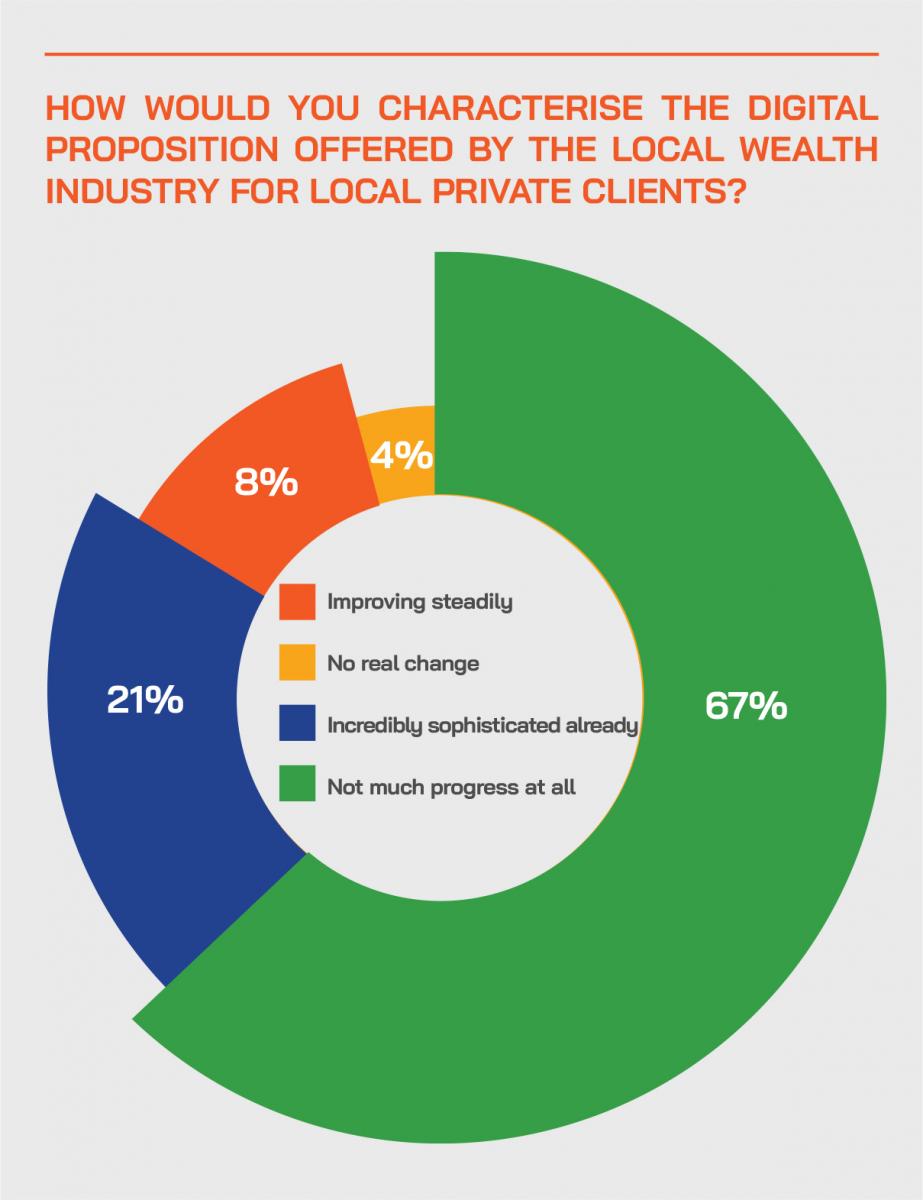

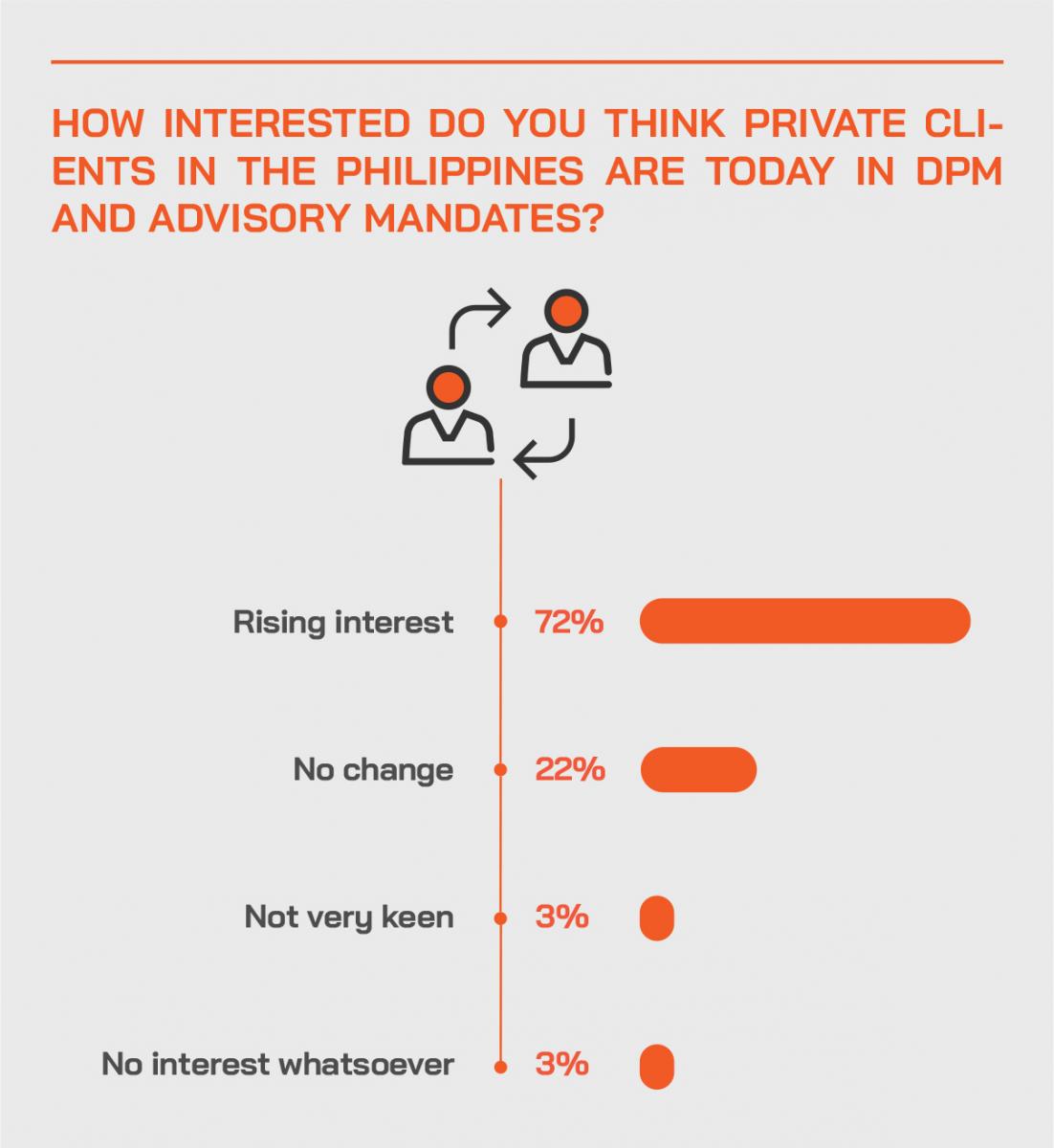

We saw that there is a strong rise in demand or at least interest in DPM and advisory, partly due to the difficulty of predicting market movement at this time of such local and worldwide uncertainty. And we heard that the digital proposition in improving broadly across the industry.

Improving digital connectivity

A guest picked up on an earlier point regarding infrastructure, commenting that the pandemic has forced the industry into far more rapid digitalisation. “The old model,” he said, “would mean that to invest, a client would go to the bank or the branch but we, for example, are now able to have investors buy the UITFs [Unit Investment Trust Funds] remotely from enrolment to redemption. We are starting to develop apps that would allow clients to do the same thing via their mobiles. The next step would be to facilitate similar access for investment management accounts; currently you need to sign a long set of forms that will allow clients to buy and sell various government securities, various equities, but today many of us are looking at how to do this digitally.”

Expert Opinion - Kevin Hardy, General Manager Asia Pacific, additiv: “Omni-channel is becoming the norm. Whether a firm is upending their legacy systems or building on top of a proposition, speed is key. Wealth managers should not accept rigid multi-year roadmaps when agile, cloud- based, API-driven SaaS solutions can get you there much faster; often in less than three months.”

He added that one positive from the misery of the pandemic is that it had forced on the industry a far more digital mindset. “We must also remember that many of our wealthier clients are older, so we must try to ensure that they are safe, so we need to more easily bring access to our products and services to them.”

Tracking global trends

Another expert commented that the industry is shifting towards the norms seen in the global markets, in other words digital onboarding, then digitised lifecycle management of an account, and also to what he called contextualised advisory, which is essentially understanding what actions clients take and why, and tailoring relevant advice to those clients. He added that contextualised advisory is digitally enhanced or enabled advice. Whereas today the RM is rather guessing what the client is doing and why and then guessing what they might be interested in, with far greater use of data, the clients can be engaged on a more relevant level.”

Expert Opinion - Kevin Hardy, General Manager Asia Pacific, additiv: “The Philippines is an attractive market for new global players, these new competitors will be API first/cloud native players. They will source their ideas from a global, not local marketplace; lowering ‘unit cost’ economics and leading capabilities on a platform specifically designed for speed, agility and greater efficiencies at scale.”

Scalable platforms required

A technology expert took that as a lead to offer his insights. He explained that it is remarkably valuable to have the right platform to enable many of these challenges to be overcome. He explained that it is very important to have a technology platform that is on a scalable basis through the cloud, and also connected via APIs, as clients these days want to be properly omni-channel in terms of their end-client servicing.

“It is all about addressing our clients’ target operating models,” he explained, “because that is often constraining how they work and how they grow their businesses going forward. We like to free our clients to explore various possibilities, so when they work with us, they will get the infrastructure to be truly omni-channel, they can utilise the cloud for scale, and they can create their own customised and bespoke experiences for their own private clients.”

Automation and efficiency

He observed that, globally, there had been some headwinds for wealth management, well before the pandemic. “Heavy regulatory requirements show no signs of diminishing,” he said, “and more likely it will get even tougher. Those must be automated where possible. Competition is significant and rising, and this country, for example, is exciting as you have a young, digitally savvy, mobile and growing affluent population. The Philippines population of about 110 million is growing really fast. The country has some 60% smartphone usage, and growing to as much as 80% in the coming years. People over 65 are just 6% of the nation, whereas in Singapore it is already 18% and rising fast. According to a Knight Frank report, the affluent, UHNW and billionaire market here grew something like 60%, 40% and 57%, respectively, in the past five years.” And all of this, he concluded, means the country is ripe for a widespread digital evolution.

Accelerating engagement

Another guest pointed to the ongoing need in this day and age of mobile connectivity, and the particular need during the pandemic to accelerate such engagement. “How can you provide your clients, especially your HNW clients who are used to that personal care and attention from their relationship manager the same type of connectivity and care through a digital medium, and then how do you do it in a way that's safe and compliant?” he pondered. “That is where we focus, the digital layer.”

He explained that the firm is work with bank clients to overcome key challenges right from onboarding of a client to maintaining that relationship, including protection of client information and working to build client loyalty with the brand to avoid the dangers of RMs leaving and trying to take clients with them. “These are some of the challenges that we're trying to address,” he said, “and we see the Philippines as a fascinating market for this, in some ways similar to India, with many similar challenges, providing a good platform for us.”

Upping the RM efficiency

He pointed to the work his firm is doing with a major global banking brand in India, which has adopted its product. “RMs could do maybe one or two meetings a day in India due to logistical issues in the past, especially traffic,” he commented, “as well as how widely dispersed clients are there, as in the Philippines. But introducing easy connectivity through apps that are secure and compliant can dramatically increase productivity, and suddenly RMs are able to do four or five meetings with customers. And that is the same here in the Philippines, and that is why this is an extremely interesting market for us.”

Keeping it ‘human’

A banker agreed with these thoughts, commenting that wealth management and private banking is still a human driven business, and that machines cannot replace people. “Investment is not a science, it is an art, and driven also by emotion, especially fear and greed, so although the bank can digitise a lot of this clients’ information and their preferences and so forth, at the end of the day, advisory on investment is still going to be an art, and you need the RMs. After all, a machine won’t offer clients empathy is they have just lost 10%!”

The conclusion seemed to be that tools and solutions for boosting RM connectivity to their clients are therefore of immense value, not as replacements, but as enhancers. “Data,” this expert said, “can provide you the listening tools, the predictive analysis, but in terms of relationship building, knowing the personality, RMs are there to stay, advisors are there to stay.”

Analytics require good data

Another guest agreed with the view that the RM’s role is fairly safe, but said the key is to ensure that the banks assemble accurate data and properly understand how to safeguard it and use it to boost loyalty amongst clients. “How do you keep a hold of those clients?” he asked. “Well, data can help you provide them a unique journey, or let's call it an ability to orchestrate a journey. You then need to have informed and smart RMs who are using that data either centrally or independently to make those very pointed decisions around, so that they target their energies and ideas efficiently.”

A guest said that banks will likely hire more data scientists to work in the investment groups to supplement investment knowledge and expertise the banks have with clearer guidance on the clients themselves. “You need to see how different groups of clients react and understand their behaviour,” he said, “so this will all affect how we should hire people and how we should train our people.”

A panel member commented how his firm’s five-year plan for going fully digital is now compartmentalised into a five-month period. “Many challenges have been front and centre during this lockdown,” he said. “We have worked with the regulators to come as a first to market with our e-KYC, this is a platform whereby a lot of our clients can now go to the online platforms that we have, whether it would be direct to consumer, direct to marketing and having clients enrol themselves in our e-KYC. We came up with what we call client discovery tools whereby they get to know about their life journeys in terms of pursuing financial independence, building up inheritance, preserving wealth, these are laddering questions that we equip our clients and have some sort of guidance into knowing who they are, and what the right products are for them. We launched this way back last year, it was intended for retail clients, but then the pandemic hit and it became more relevant for other categories.”

Cutting costs

He explained that what is really nice about all these digital upgrades is that they are helping to lower costs. “For example, instead of hiring ballrooms for events, we can now have an overseas fund manager talk about the global markets, pitching our feeder funds or fund of funds product offering,” he said. “And digital is really an enabler in terms of knowing who our clients are, in terms of onboarding them, for peer-to-peer conversations with RMs, with our advisors, all very important, as this is how conversions happen. We are really quite lucky that we were able to have a first-to-market advantage in terms of offering these things on our online platform.”

Expert Opinion - Kevin Hardy, General Manager Asia Pacific, additiv: “In 2021, wealth managers must work more efficiently remotely, however, more progressive players will take advantage of the ‘flux’ by differentiating client experiences. This doesn’t mean just digitising inefficient processes and delivering customers an ‘app’, it could be launching D2C channels leveraging 3rd party wealth platforms or robo technologies; lowering costs and capitalising brand strengths.”

Plenty of positive intent

A panellist commented that the digital transformation journey should already be well underway. “We are talking to everyone,” he said. “A lot of this work is about evangelising, getting the word out and having the conversations because only then do clients get an understanding. There is a deluge of information flying at customers, and it is tough for them to work out what they really want or need or what works. From our perspective as a WealthTech, we only talk about live products for clients. What we definitely see in the Philippines is the intent, but also that some of the decision making is muddled because of the way that firms are thinking with respect to the target operating model. I'll stress this point, because if you think about how you do things today, and all you do is try and digitise it, you'll just end up with a digitised, inefficient platform, which is wrong.”

Buy or build?

The other difficult question organisations are struggling with, he explained, is to buy or do I build. “I get super-frustrated when I hear that because it's a bit like the active-passive conversation, it's not one or the other, it's both,” he commented. “You should be going down both routes. When you have both, you can have better outcomes when you both build and when you buy. You don't have to go for Big Bang. We did some work with a behavioural scientist and it was a case of test and learn, then iterate. You can do that in small steps through a lot of the SaaS based technologies such as ours, that you can put in place.”

Step by step

He added that there are really three steps to consider. “The first is you can identify quick wins, you can find quick tech-based remedies that get you further ahead, these are not revolutionary changes, they are the quick steps that help build confidence. The second step is aligning data, which is useless on its own, with the right analytic tools to allow better targeted client engagements, and actionable with the RMs for example for targeted campaigns with individuals. This is not replacing the RMs, it is making them bionic.”

And the third step, once these series of these gradual shifts have been achieved, is reinvesting all that knowledge so that the clients repeat, test, learn and iterate. “It is vital to take all that knowledge and continue on your journey, because then you can then compete more effectively in a very competitive landscape. We and others here today are working with some of the largest organisations in the world, and the technologies that we can provide smaller and mid-sized players is likely to be the same, allowing smaller firms to compete on a level footing with the bigger guys at a similar cost. And because of the SaaS based pricing models, they do not need to part with millions and millions of dollars, they can do it at a lower cost.”

Where to invest and how?

The moderator then diverted the dialogue back to the world of investments. A senior banker responded by observing that the best first step is again to understand the clients, to help define their goals, and understand risk appetites and timelines. “That,” he said, “is the first piece of advice.”

He explained that his second piece of advice is to find the right products to suit these clients, and to ensure they are properly diversified across markets, products, regions, and types of assets, to suits needs and risk profiles. “And the third piece of advice,” he reported, “is keep monitoring, keep looking at your portfolio, know that this time, it's not set and forget, it is about re-balancing.”

Risk can be carefully applied

Another guest quoted “the willingness to take risk is not the same as ability to take risk”. “These are two different things,” he said. He then commented that investors across ASEAN have similar needs, and recommended looking further at technology, at China, and at ESG, where he said there is a lot more pressure by the regulators and the stakeholders and shareholders to drive ESG compliance. He also recommended looking at digital assets including cryptocurrencies, and finally private market assets, largely because public markets are so volatile and often over-valued.

Nextgens coming through

Other key themes, he said, included the transition of wealth and economic momentum to the next generations. And finally, he observed, there is the trend to professionalise investments, with family offices, and other developments.

The final word went to another expert who recommended a balanced portfolio and with plenty of offshore assets, as there is literally so much choice worldwide for funds and markets. “Of course, you should also look at the local markets because apart from yield, there are plenty of discounted prices.”