Publications & Thought Leadership

The Drive to Enhanced Client Engagement in Tomorrow’s World of Digitised Wealth Management

Apr 27, 2021

(The Soft Stuff is the Hard Stuff)

In late March, Hubbis in partnership with InvestSuite, a European B2B WealthTech company providing a suite of digital solutions to help drive client engagement in the wealth management space, hosted an exclusive Webinar to highlight the vital importance of evolving the private client experience, focusing on how the digital technologies of today and tomorrow can assist wealth managers to enhance and also retain the engagement with their private clients.

The discussion built further on a significant body of thought leadership events and reports that Hubbis has organised in recent years on the immensely important topic of digital transformation, in this case with InvestSuite’s experts zooming in on the whole concept of digital solutions to enhance client engagement and to improve the curation then delivery of relevant, and potentially tailored advice.

Wealth management has always been a story of personal relationships, trust, knowledge and skill. However, in the broader financial industry’s ongoing digitisation, the main focus seems to be on transactions and making interactions as fast, functional and frictionless as possible. But is this the way forward for the wealth industry? Is it not ‘the human element’ that will distinguish the genuinely superior client experience from the merely good experience? And if so, what could digital investment services look like when we shift the focus from product to client-centric design?

The premise for the Webinar was that as the universe of digital solutions being promoted and rolled out across the region’s offshore and onshore wealth management markets expands apace, any wealth management institution wanting to compete in the future will need to be at the cutting edge of client engagement, promoting an optimal client experience, especially in the age of Covid-19 where remote dominates the landscape, by necessity but also increasingly by inclination.

To achieve these goals, the wealth management incumbents must leverage data, analytics, AI, machine learning, and a host of client-friendly digital media that are all vital to top-flight advice, client engagement and loyalty. The experience begins right at the outset of the relationship and digital tools aligned with the right processes can boost trust, engagement and confidence throughout, from the vital step of onboarding all the way through transactions, portfolio creation, performance monitoring and more user-friendly reporting.

The Webinar was also an opportunity for InvestSuite to highlight its name, its short history, its solutions and its core missions and to explain how the firm is now engaging with clients across Asia Pacific. InvestSuite is now in the process of significantly expanding its market reach and products in this region, growing the team and bringing what they believe are unparalleled innovations to customers around the globe, as it accelerates AI-based digital investment solutions for financial institutions to expedite their digital wealth transformation.

Founded only in 2019 in Europe, the firm has assembled what the enterprise’s leaders consider a world-class team of more than 50 professionals spanning across wealth management, behavioural science, digital design, AI and computer science, and is present in Europe, Latin America, and the Middle East, while at the same time now attentively and strategically building its presence in Asia Pacific.

The Agenda

The Webinar presented three key InvestSuite leaders as well as an eminent ADR, cognitive science and psychology academic, Professor Klaus Harnack. Together they provided their perspectives on the following areas:

- Creating Client-Centric products and advice founded on Client Insights

- The Evolution of Digital Solutions aligned to perception and decision-making processes

- How can Digital Solutions Align with Behavioural Economics

- Digitised Education of the rapidly expanding mass affluent client base

- The Evolution of Digitised Reporting to Clients in a Digital World

- Why InvestSuite is Bringing its Global Solutions to the APAC Wealth Market

The Speakers

Keynote Speaker - Professor Klaus Harnack

Dr. Klaus Harnack studies and teaches ADR, cognitive science, and psychology. Over the last ten years, he worked as an academic, behavioural consultant and trainer on the topics of perception and decision-making processes in industrial, economic and financial settings. His main objective is to bridge the gap between behavioural research and applied economic settings as an advisor, author and columnist.

InvestSuite Speakers:

Sven Moons

For the previous 15 years Sven was senior strategist at Kunstmaan/Accenture Interactive where he created the branding and customer experience for companies in a variety of industries: from insurance, payments, brokerage services, HealthTech. He is now with InvestSuite, where he is in charge of customer insights, doing research (often together with universities) to inform the company’s client-centric product development.

Brendan Meehan

Brendan is Senior Product Manager and Oxford MBA with experience in building businesses and FinTech products. Brendan has a passion for understanding humans through the lens of behavioural economics and creating digital products that change behaviour for the better. Brendan is a Certified Financial Planner.

Tim Smith, Managing Director of APAC

Managing Director of InvestSuite for Asia Pacific, Tim has over 25 years of experience in banking and wealth management in Asia Pacific, and most recently led Westpac’s Private Bank in Sydney for 10 years. Tim’s insights into the Australia wealth management landscape and solutions, his knowledge of the Asian wealth market, and of the InvestSuite bank of digital solutions are already helping Tim gain significant traction building relationships in the region’s wealth industry for clients to engage with InvestSuite’s range of solutions.

The Event

Driving Client-Centric products and advice founded on Client Insights

Sven Moons opened this portion of the proceedings, offering his insights into the world of personalised client engagement. Aside from skills and knowledge, wealth management, he reported, has always been about the development of personal long-term relationships, supported on the foundations of trust and discretion, and also good communication skills.

A case in point…

“I recently read a book about the story of a Dutch private bank, based in Amsterdam,” he told delegates. “They are more than 200 years old, and one of their RMs today is over 70 years old and manages just one specific client, a family for whom his own father used to be the private banker at the same bank. His role there and his longevity at the bank prove that the core competencies of financial advisory and wealth management are manifested in the long-term relationship, founded on trustworthiness, discretion, and skilful communication.”

Trust, Discretion & Communication = Long Relationships

He then observed that this long-term relationship, this trustworthiness, discretion and honest communication are core to wealth management as a whole for several reasons. They are competencies that other players (and not in the least the ‘Big Tech’ players) will find very difficult to imitate. They can be applied to all kinds of services and activities, right from the onboarding of new clients to portfolio composition, reporting, and so forth. And they bring a kind of value that clients are actually prepared to pay for, as clients are buying not just knowledge or access to markets, but also the trustworthiness, the dedication to long-term objectives, the discretion and high-quality communication.

The Digital Transformation of the UX/CX

He then extrapolated that, despite these observations, the big changes and ‘disruptions’ in the financial industry of the past 20 years or so, have not been inspired by these core competencies. In fact, he said these major changes are essentially just about digitising transactions.

“We first saw this in the early 2000s in some of the more ‘easy-to-digitise’ domains like insurance or payments,” he reported, “and as those activities are inherently ‘transactional’, they were rather quickly digitised. And we saw the same when Elon Musk’s Paypal fired-up ecommerce in 2000, and today for most young people today, a ‘wallet’ is now app on a smartphone.”

Elevating the experience

He explained that these ‘transactional innovations’ inspired new distribution models. “Usually, involving lots of disintermediation, they inspired new business models, and usually involved words like ‘free’ or ‘freemium’ or variations on that theme,” he explained. “And they inspired a lot of super-streamlined services that are now no longer just called ‘services’, they are called ‘experiences’ nowadays.”

He joked that there is perhaps no financial institution in the world that hasn’t had a business consultant come to them and say they should become the Uber of banking-experiences. “It seems like those consultants wanted to warn us all that, if banks didn’t create an “Uber-like experience’ they would become obsolete, remember the story of the dinosaurs.”

Wealth management must evolve, and rapidly

Joking apart, he stated that there is no way that the world of investments and wealth management will remain immune to these changing expectations and the new cultural norms of the online world, and the drivers are not simply the youngest of the online generations, because the Millennials soon at the receiving end of the biggest inter-generational wealth transfer in history are now turning 40 this year.

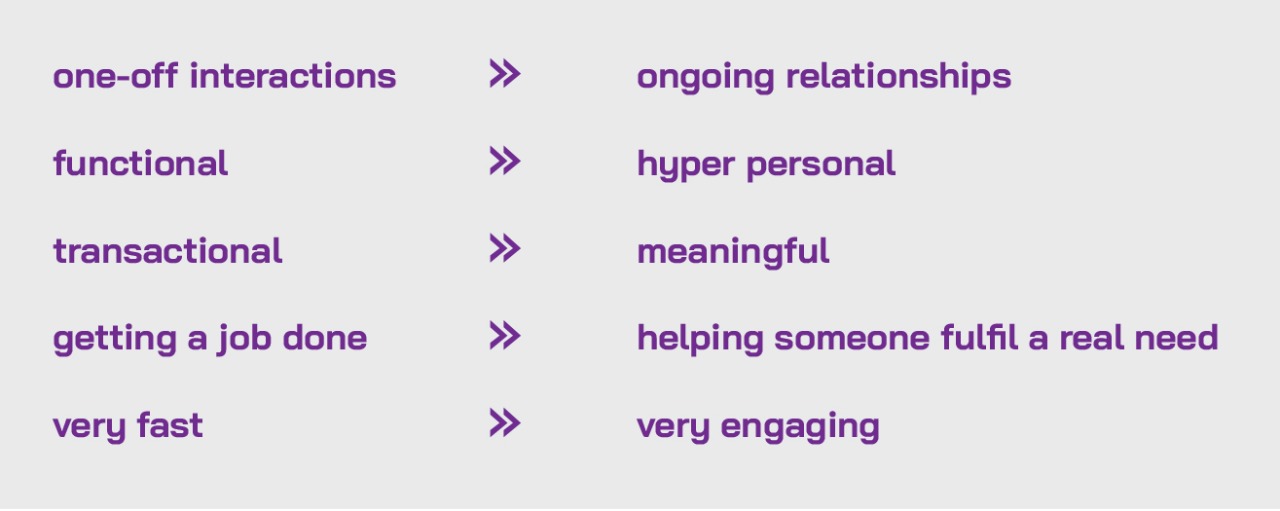

“Actually, when we look at design innovations in wealth management in recent times, we actually see the exact same focus on transactional optimisation we saw 20 years ago,” he observed. “We see, for example, that onboarding and risk profiling often just look like an online version of the old ‘pen & paper’ questionnaires. Reporting on portfolio performance has moved from the usual face-to-face meetings to Zoom, but it’s still supported by the same slides, the same tables, pie-charts and graphs as before. And we see that the UX design of all the really ‘hot’ investment platforms is around transactions that are extremely fast, functional and frictionless.”

Adapting to the emerging client base

He said that all these views lead him to pose the question as to how the wealth management industry can continue to thrive and engage a new generation of clients in this changed environment and culture.

“The answer, we believe, lies in creatively applying our core competencies in the digital environment and ensuring that the ‘human element’ is not a blocking or negative factor, but actually is empowered to distinguish the genuinely great from the merely good client experience,” he reported.

Relationships must transform from transactional to human-centric

And he explained that if this is to be achieved, a major shift must occur. The relationship must change from:

“To wrap up this presentation, I can say that the single most important concept is for private banks and wealth management firms to thrive in the future, we must shift from a functional to a human-centric design philosophy and extend the experience that our clients have always sought and had of a trusted, long-term, personal relationship into the digital world.”

The Evolution of Digital Solutions aligned to perception and decision-making processes

Klaus Harnack took the virtual stage to observe that onboarding at the outset of a relationship is largely about establishing a trusting relationship.

To be trusted, you must care

He explained that the concept of trust from a scientific point of view boils down to the client’s perception of whether the other person they meet in any type of relationship is well-intentioned and caring, and whether in a business and advisory context they are also competent, and therefore capable of acting professionally for the client based on good intentions.

He therefore essentially defined trust as a psychological state comprising the intention to accept vulnerability based upon positive expectations of the intentions or behaviour of another.

Shifting the emphasis from competence to benevolence

He explained that too often people aim to demonstrate their competence, but not their benevolence, not that they truly want to take care of the customers with compassion and goodwill. “So,” he stated, “this is the starting point. In order to establish the trust, we really have to rearrange how we present ourselves away from competence, a shift from competence to benevolence.”

Deep and continuous assessment of client needs

The second key element of this equation, he reported, is the assessment of the client needs. He observed that, usually, the attempt to understand the client takes place early in the relationship, what he termed a single-shot measurement, and approached more as a ‘burden’ or duty, rather than a genuine opportunity to be embraced to far more deeply understand those clients and their needs.

Focus on client goals and deliver with good intent

In order to offer suitable financial solutions and tools, the provider needs to focus on the personalities, motivations and goals, and that process then opens the door for the delivery of the firm’s or the banker’s good intentions and deliver those with competence.

How Digital Solutions can Align with Behavioural Economics

Brendan Meehan then spoke, first explaining that his background is in financial advice and that at InvestSuite he is the product manager for the robo-advisor. “And that leads me neatly into what I want to focus on today, which is how we can apply human thinking, human-centred design in digital technology products,” he explained.

Robo advisors can build genuine trust

He reported that from the outset, the robo advisor can build trust and ‘benevolence’ through an extensive risk profiling process, including, for example, asking clients about their views on ESG, climate change, shifts in technology, whether they might require Shariah-compliant products, and so forth. He explained that the mission is to demonstrate that the offering is really interested in them as individuals as well as users, thereby developing a trusting relationship with the robo advisory.

Monitoring behaviour, adapting solutions

He added that whereas so often the risk profiling takes place only at onboarding and then remains static, perhaps for some years, the robo advisor approach is to maintain this on an ongoing basis, digitally. He reported that in doing so, the InvestSuite robo advisor solution can monitor the behaviour of the client, open engagement with the clients based on their activity, open narratives that are relevant, thereby adding a more human element, building trust.

Redefining risk profiles

Additionally, the risk profiling can be updated every several months, by presenting a few additional questions to the users, thereby helping to refine the risk profile. And in doing so, the mission is to build the relationship for the longer-term, not see it simply as a transactional tool.

Digitised Education of the rapidly expanding mass affluent client base

Education is vital for any endeavour and in the complex world of finance and investments, bringing the expanding investor base up to speed is vital and must be an ongoing commitment. Doing so digitally is incredibly valuable in helping customers whose wealth and investment activity is on the rise better understand investment products, markets, financial planning and investment strategies.

How cognition translates to action

Klaus Harnack addressed this topic, explaining that there has been a paradigm shift in how to view learning processes and cognition. “Before,” he reported, “the idea was that cognition is something similar to a computer, so you have an input, something is computed, and you have an output again. But nowadays, we see that cognition is for action, and therefore skills, learning, perception and memory must be understood in terms of their contribution to situation-appropriate behaviour. Learning means what can the person do is such a certain situation.

Caring is directly relevant to the investment world

“This is what good caring means, it means giving the people the chance to discover the opportunities, and then really help them to enact them by supporting them with good tools,” he explained. And he added that this is directly and entirely relevant to the investment world.

In-app learning (leveraging digitised education)

Sven Moons also tackled this subject of client education. He explained that some financial institutions provide no education on investing, some might have a digital learning platform, some an academy or dedicated links on the website, or in the app, some even offer more formal training webinars such as these, and some in normalised times even classroom education.

“But what we are doing,” he reported, “is building an embedded learning feature into our self-investment app to achieve in-app learning. We aim to ensure that the learning moment is really relevant and timely, the app guiding users through their actions.”

With in-app learning, he concluded, the learning moment must be really relevant and timely. “You learn something when you need it, so there’s no crash course before you can actually start,” he explained. “Instead, the app just guides you through your actions.”

The role of ‘micro-learning’

He explained that the firm had leveraged some language app approaches towards what is known as ‘micro-learning’, which can take only perhaps 60 or 90 seconds each time, and then the user tries it out for themselves. He said that in the InvestSuite robo-advisor context, this is organised in a ‘safe’ way that does not actually expose the user financially until they are ready to take certain steps."

Enhancing the feel-good factor

The second element, he reported, is to ensure that the learning must be progressive. “The app helps users learn incrementally, in a manner of drip-feeding and then with the clients engaging through their actual usage,” he explained, “and basically we keep holding their hand throughout. The process is, therefore, to nudge you gently to these mini-learning opportunities, and then allow you to try out what you’ve learned, then you obtain a kind of ‘self-confirming-feedback’, leaving a feel-good impression at the end.”

He added that the firm is working on a research project together with the University of Leuven’s Social Sciences Department with the aim of obtaining scientific proof that micro-learning in this financial and investment context will be much more effective than the formal learning methods used widely thus far.

The Evolution of Relevant Reporting to Clients in a Digital World

Klaus Harnack addressed the topic of reporting to clients in a digital world, explaining that there must be a genuine connectivity between information about performance and an understanding of what the client needs. He said that based on understanding the personalities, their needs and expectations, also their goals and motivations, and then the right feedback can be delivered in the right way to the right people.

Linking reporting to idea and advice generation

With all of these elements in play, the wealth management provider can then assess the right ideas to offer them for new products, and at the right time, or perhaps even advise them not to take products but to save cash and act later.

Moving from standardised to contextualised reporting

“There is no magic to it, you simply have to assess the motivational stances, the risk attitudes, but this needs to be coupled with the environment, with the context of the time we are in at that moment,” he concluded, noting that much of this can simply be missed with a standardised feedback and reporting protocol. Clients, he said, need a report that really support them in their financial world; that should be the main aim of the reporting protocol.

InvestSuite’s Storyteller solution

Tim Smith offered his views on reporting as well. He explained that the norm has been for the customers to receive the Excel spreadsheets and smart PDFs filing out of financial institutions full of loads of data and acronyms, but with few if any insights into their portfolios.

“But I know from first-hand experience how engaging it is when an advisor can have the tools such as a new reporting style,” he commented. “And this is where InvestSuite’s Storyteller solution brings customer centricity driven by the latest technologies in AI and machine learning. It comes back to the ability to personalise your investment performance in a new way to engage clients.”

Personalised and hyper-personalised

He explained that the new world InvestSuite sees ahead is the video delivery of statements personalised to the individual client. “That will be the new world ahead,” he stated. “Personalised and hyper-personalised to your portfolio. Someone reads that to you like it's a television programme, and it's your portfolio. That technology is here today. We built it, and that is part of the new world of client engagement.”

Leveraging reporting for client engagement

He said that the relationship manager is the one who would send the video report to the client and then arrange a follow-up discussion to run through the thematics and information in that particular report. “We see it as engagement, as complimentary, as educational,” he concluded. “We are already in discussions with private banks in Europe at the moment about exactly this product.”

Tailored to different wealth segments

And this solution can be adapted, he explained, for the HNW market as well as targeting the mass affluent clients. “In Asia, there are not usually RMs in the emerging affluent, so they need education, simplicity, support, privacy and security. But these reports can also be tailored to the HNW market and above, using different language and different tone but all based on a similar type of analysis.”

Digitised to fit

That opened the door for Brendan Meehan to add some perspectives on hyper-personalisation. “This is exceptionally important, as everything is tailored towards the user, even the language of the risk profiling, for example,” he explained. “The portfolios that we create are personalised based on the parameters that our clients set, so what you are invested in is tailored towards your beliefs, your risk profile, and so forth. This is the hyper-personalisation of wealth management, and that is what we are achieving digitally.”

The obvious mistakes that clients make when investing

Klaus Harnack explained that based on behavioural finance, there is a long list of cognitive biases that people frequently adopt, and that research shows that people are more or less incapable of learning to deal with these biases, in other words, we make the same mistakes over and over. Accordingly, the apps and offerings should offer both client control but also guidance.

“This guidance can be done via artificial intelligence to consolidate data and to then make decisions easier based on a holistic understanding, then offering us simpler choices,” he explained. “That is one important way out of the classical traps we see in the financial world.”

Why InvestSuite is Bringing its Global Solutions to the APAC Wealth Market

Tim Smith closed the event by offering some more insights into the world of InvestSuite and its solutions. “We are only three years young,” he explained, “and I think you will now appreciate that the core DNA of InvestSuite is to provide customer centricity. Armed also with behavioural scientists as part of the team, we have a different philosophy of looking at technology to enable the relationships that are core to generating revenue from maintaining, obtaining and retaining clients and building your own businesses,” he explained. It's this technology that we are bringing to the region that we are confident clients out here will embrace.”

B2B at the core

He explained that the design aspect of technology is really evolving and that although the focus of InvestSuite is entirely on the end private client, the business is entirely B2B. “By focusing on their clients, we are helping the incumbent global wealth managers, as well as aspiring wealth managers, in short those that are looking to get ahead of their competitors by leveraging and implementing these new technologies.

Well-designed to fit

Design, he also reiterated, is the key, so that the solutions fit the business model of the private bank or wealth management. “Having run Westpac’s private banking division here in Sydney for a decade, I saw first-hand how the use of technology is shaping major transformational changes.”

Building the brand in APAC

“Our mission in this region today,” he added to close the discussion, “is making sure that the wealth management community knows that we are here providing these solutions and also understands more about how these technologies can enable your business, your relationship managers, your advisors, your asset management firm to interact with clients in a different and elevated way. If I had had these tools at my disposal 10 or 15 years ago, it would have made my job immeasurably easier. And with that, I would like to thank all the wealth management attendees today, my fellow speakers and of course, Hubbis. I think I speak for all when I say look forward to meeting you face-to-face before too long.”

InvestSuite: Its Digital Solutions and its Relevance to the APAC Wealth Management Community

InvestSuite is a European B2B WealthTech company providing a differentiated suite of digital solutions to help wealth managers address their rapidly evolving digital needs. Hubbis asked Bart Vanhaeren, CEO and co-founder of InvestSuite, for his insights into the firm and its solution. He explained that the firm is now significantly expanding its market reach and products, growing the team and bringing unparalleled innovations to customers around the globe, as it accelerates AI-based digital investment solutions for financial institutions to expedite their digital wealth transformation. He explained that less than three years on from his co-founding of the business alongside an experienced team of bankers, computer scientists and product designers, the company has grown to over 45 employees across Europe with a sales presence in Europe, Latin America, and the Middle East, and is now intent on building its presence in Asia. We also soke with Tim Smith, the Sydney-based Managing Director of APAC, who before joining InvestSuite had enjoyed a successful career in private wealth management and institutional banking. Tim is already building relationships and pitching InvestSuite’s solutions across the region. Tim explained that digitalisation is already a big step up, but it is not enough, as wealth managers need to deliver the ‘best’ digital experience, from onboarding all the way through performance and reporting.

The global wealth management evolution

The global wealth management industry is going through massive disruption and transformation at present. There is pressure on fees, increased regulation, a far greater focus on returns and a completely new generation of investors are demanding a greater customer experience in their wealth interactions.

Established wealth managers in the Middle East and Asia Pacific are not immune from the global changes. InvestSuite is driving its solutions and name recognition in both regions now.

Bart explains that the firm sees four extremely important steps in gaining and keeping clients. These are:

- Onboarding will be digital: make sure it is an inspiring and engaging experience

- Experience is everything, hence the importance of human-centric design

- In the end, it’s about the return, so iVaR is based on how people really experience risk and the engine of our portfolio construction framework.

- Next to onboarding is portfolio reporting, which is one of the most important moments in a client lifecycle, and using AI can really make this a moment that counts, meaning a hyper-personalised and truly insightful client experience.

iVaR – a propriety approach

“Investing is all about harmonising the challenges of seeking return and mitigating risk,” Bart elucidates. “Our approach to AI and robo-advisory is truly different. We have a truly differentiating algorithm; we do not use Markowitz and volatility as risk parameters, we have gone well beyond risk definitions such as VAR, and we have developed a fourth-generation proprietary risk approach which we call iVaR. This is our proprietary solution for minimising risks while seeking returns. Nothing is guaranteed in the world of investments, but we aim for the smoothest journey to creating, then re-balancing investment portfolios for our bank and wealth management clients, and of course, for their end-clients.”

The Four InvestSuite Products

In all, InvestSuite has four core products.

Robo Advisor

InvestSuite’s Robo Advisor was designed as a customisable and low-cost digital wealth management service for retail clients. It provides Mifid-compliant onboarding and risk profiling, along with portfolio reporting and re-balancing. It is fully customisable at the front end and can be used with your own or third-party funds. It even provides options for fully personalised portfolio construction.

Self-Investor

Self-Investor is a next-generation, intuitive and user-friendly online trading platform that helps wealth managers and private banks stay ahead of the competition. It enables clients to manage a part of their portfolio in a self-execution setup. It allows them to research and trade investments themselves for that part of their portfolio, while the private banker/relationship manager gets automatically informed, providing touchpoint opportunities.

StoryTeller

StoryTeller helps wealth managers calculate and report investment performance to end investors in a fully personalised way, using relatable, understandable language. It analyses the drivers of investment performance thanks to state-of-the-art performance attribution and news aggregation algorithms and outputs the results in an intuitive, fully personalised and automatically generated report. “In short,” Bart reports, “it is a completely new way of relaying performance of a portfolio in plain language.”

Optimizer

And Optimizer is the firm’s next-generation quantitative portfolio construction solution. It offers a portfolio loss protection methodology that can be overlaid on any investment strategy. “But using Optimizer, this is exactly where the firm’s state-of-the-art iVaR portfolio construction methodology aligns with traditional portfolio insurance algorithms,” he adds, noting that it works ideally with either a defined investment universe or model portfolios.

A B2B FinTech with the end client at heart

Bart also notes that InvestSuite is essentially a pure B2B WealthTech company, with a team of seasoned experts who operate across AI/machine learning, design, human insights and wealth management. “Our shared goal is to create user experiences that open up new markets and drive commercial success for our clients,” he states. “In the wealth space, InvestSuite helps banks, brokers, wealth managers and other financial institutions serve their clients better with its suite of modern digital investment solutions.”

Adding value to the wealth management industry

“We are therefore instrumental in helping the private banks and wealth managers develop digital solutions to retain these clients while avoiding excessive investment in proprietary systems and keeping up that crucial element of personal service,” he reports. “Our suite of digital tools has been designed to help private banks and wealth firms to build on existing expertise and processes, and deliver the next-generation services that will help set them apart, but crucially without burdening them with huge, and potentially often failed, digital transformations expenses.”

Helping Asia catch up

When it comes to wealth management and investments, the incumbent players, perhaps especially in Asia, are generally still actually lagging behind, he observes. “We therefore see this huge need out there, driven by the end-customers, for banks, financial managers, private banks, pension funds even, to offer clients their services in investments and wealth management in a fully digital way. But it is not easy. Working with us, they are able to efficiently launch a robo-advisor, and use our investor platform. Our work is therefore from the front-end, the digital part, up to the middleware or the core banking. That is the landscape we operate in.”

Sights set on Asia

Elaborating on expansion across the world from its core strengths in Europe, Tim Smith reports that in APAC, Australia, Singapore, Indonesia and Malaysia are the first targets. “The opportunity in Asia is similar to the rest of the world, which is basically that whichever institutions one works through, one is investing either as self-directed, through advisory or via discretionary,” he reports. “And digital is the evolution required for all. However, for a bank to build a robo-advisor themselves, it will cost perhaps as much as EUR10 million and take three years or more. And it might not even be successful.”

Opening new doors in APAC

Tim explains that with the strength of this offering, the firm’s uniqueness and its four state-of-the-art products, the firm can open doors to major banking groups and names in fascinating markets such as Indonesia, for example.

Unique offerings

“It is incredible to see our solutions pitted against everyone else in the region, and we are starting to get shortlisted by household names across the world,” he explains. “And that tells us that we're on track to truly differentiate ourselves. We have one major universal bank in Asia telling us that we have a unique offering. So, when I look at the opportunities in Asia, and here I'm speaking of the Philippines, Hong Kong, Malaysia, Singapore, whenever I present to them across our broad stable of products, particularly with StoryTeller, or our optimised self-directed platform, the Optimizer product, which is more for family offices in Asia, feedback has been really positive.”

InvestSuite’s Key Priorities in Asia

“First,” says Tim, “we are setting about letting the whole of Asia know who we are, what we have, and what makes us special, different and better, especially with the Robo Advisor, which we believe is well ahead of the competition. Number two is to gain a foothold in the Asian market with the Portfolio Optimizer product, and later StoryTeller. And third, we are in advanced discussions with parties with regards to brand recognition and thought leadership.”

Bart adds: “This last point is a big area for us right now – we want to use thought leadership to convey how we are combining all aspects of the latest technology in the world, and bringing that to some of the more established players in the region to truly give them the ability to leapfrog the competition.”

The real competitive edge

Bart closes by reporting that InvestSuite is providing their clients with a real competitive edge. “These should not ultimately be cost-based decisions; they should be success-based,” he concludes. “These solutions, if constructed and delivered optimally, will make crucial, critical differences, while getting this wrong might have dire consequences.”

Managing Director, Asia Pacific at Investsuite

More from Tim Smith, Investsuite

Latest Articles