How are Private Banks fulfilling a key AML/KYC requirement during the pandemic? The challenges in obtaining source of wealth information were already high, are now more complex with in-person meetings difficult to schedule and obtaining client documentation, particularly certified copies, extremely challenging.

In association with our exclusive partner for the project, UK-global risk and compliancebased consulting firm Protiviti, Hubbis has conducted a mini-survey of the wealth management market in Asia to:

- Gauge the temperature and identify the types of concerns the incumbents have over these issues;

- Understand better how they are tackling these problems, and;

- Where better internal practices, management cultures, enhanced communication, and better technology and digital solutions can all ride to their help.

Key Pointers to a Better Way Forward

Greater consolidation, coordination and clarity are likely to produce better outcomes

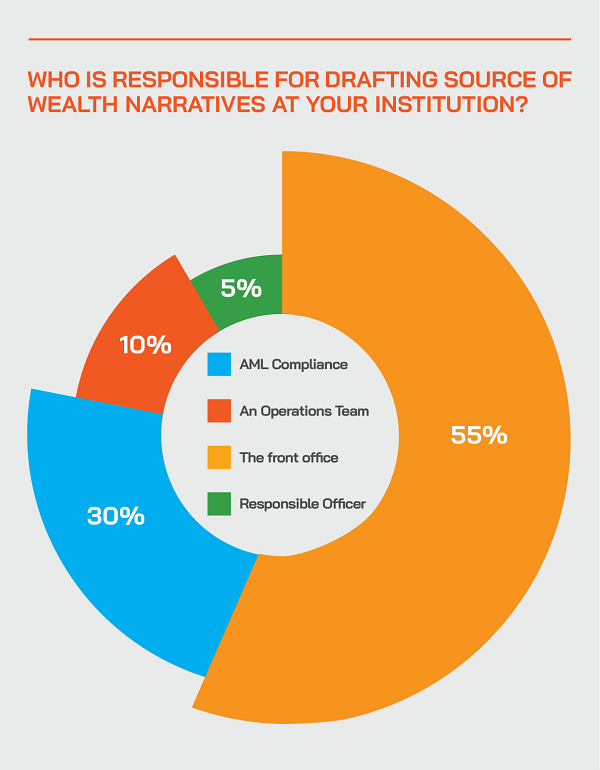

The responsibility for drafting Source of Wealth narratives at wealth management institutions appears to be spread out too broadly and inconsistently amongst different teams, with 55% of respondents pointing to the front office, 30% to the compliance/AML function, and 15% to operations and/or a dedicated officer.

There are many issues to address, and the obligations are constant

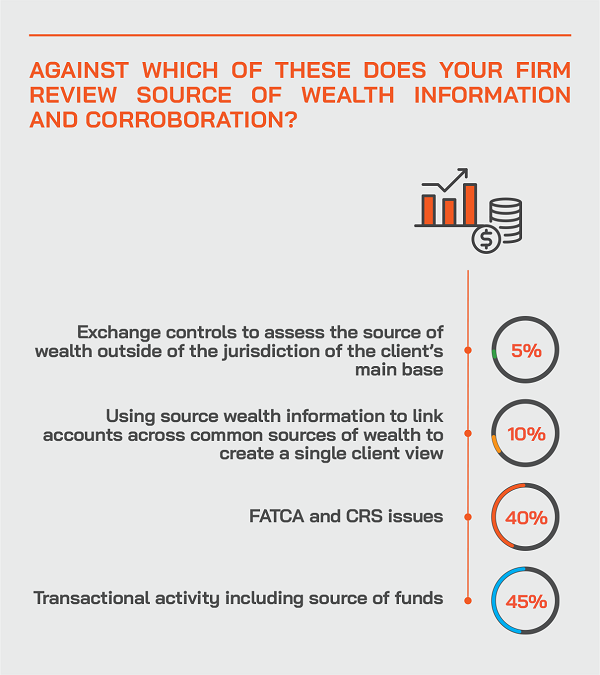

There are many boxes to tick, there are many targets to hit, and the obligations are constant, as Source of Wealth is not just a mission at the client onboarding stage. Source of Wealth information and corroboration is immensely complex – 40% of respondents pointed to the need to comply with global FATCA and CRS issues, 45% pointed to the need to verify the source of funds and ongoing transactional activity. Only 10% of replies pointed to using Source of Wealth information to link accounts across common sources of wealth to create a single client view, even though the single client view is so valuable from both a compliance and also ongoing client satisfaction perspective.

Internal communication is challenging, it is tough constantly chasing clients, and regulation evolves non-stop

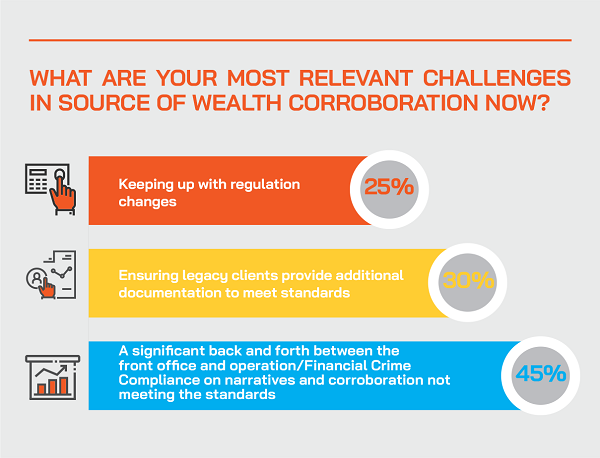

The demands on the wealth management players are onerous and costly to fulfil, communication and collaboration internally are often problematic, and of course, regulations are constantly evolving. Some 45% of replies indicated that a key challenge in Source of Wealth corroboration involves the constant need for communication between the front office and compliance/operations. 30% of respondents highlighted the ongoing obligations and how tough it is to ensure existing clients continue to provide the additional documentation to meet regulatory standards. And of course, 25% pointed to the difficulty of even keeping track of the constantly tightening demands of the regulators.

The absence of single standards makes life for wealth management institutions even tougher

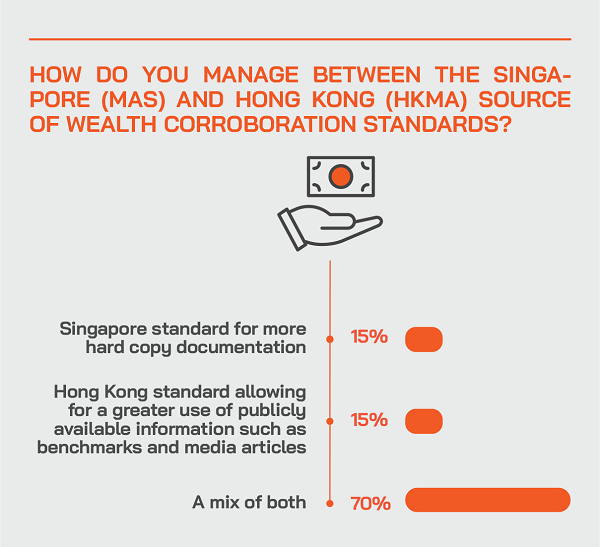

There is no single standard for Source of Wealth corroboration, not even between the two leading offshore financial centres in Asia. Accordingly, some 70% of replies stated that the wealth industry must adopt the standards demanded by the regulators in both Hong Kong and Singapore in order to tick all the boxes and be comprehensive in their approach, as each jurisdiction has a somewhat different approach.

The pandemic has brought even more challenges; there is no end in sight, and action is needed

Respondents pointed out how challenging the arrival of the pandemic had been because of the lack of face-to-face meetings that are often so essential in building mutual trust, the difficulty in verifying documents, and the often lengthy delays in obtaining certified copies, although some experts reported that video calls are quite effective with clients and that as the pandemic had reduced the industry’s ability to seek out and win new clients, that had helped mitigate some of the stresses. All seemed to agree that these problems will persist for the foreseeable future and that consistent and emphatic action is needed to get on top of these matters.

Using technology solutions should improve Source of Wealth practices and outcomes and help in fulfilling the wider onboarding and KYC/AML demands.

All our replies indicated that technology could or should help in checking and corroborating Source of Wealth information from public sources. However, while some are using such tools, some are analysing their efficacy, and many noted that information of more than 10 to 15 years old is very tough to confirm. Some respondents commented that it takes time for the banks to trust and adopt the technology and time for the clients to trust the institutions sufficiently to deliver the information in the first place. But our respondents appeared to almost entirely support the view that digital solutions will enhance and improve the entire onboarding, SOW, KYC and AML processes and obligations. As the demands are also ongoing throughout a client’s lifecycle, the costs of these technology investments should be considered over many years, not simply as a one-off upfront cost.

The Report

Why should wealth management institutions collect and attempt to verify Source of Wealth (SOW) information? It is part of a range of Know Your Client (KYC) measures that seek to address the Anti-Money Laundering (AML) risks that constantly arise in, or rather that are endemic to the wealth management industry. The objectives of good KYC, AML and SOW practices should be based on fact, as this information drives risk management for the institution and, if managed properly, can help to drive better client relationships, as there is a significant degree of trust to be achieved on both sides.

Mining down into the SOW detail

SOW refers to the origin of the entire body of wealth, from wherever that might be derived, whether from regular salary plus bonuses, from inheritance, from equity or other investments, from company sales, or the sale of stakes in companies, from property investments and disposals, life insurance policies, so on and so forth. This information will usually give an indication as to the volume of wealth the customer would be expected to have and a picture of how the customer acquired such wealth.

The regulatory are circling the wagons…

There is more and more evidence that private banks and other wealth management firms in Asia urgently need to overhaul their AML processes in the face of heightened regulatory expectations. We know from many Hubbis interviews, events, thought leadership discussions and partner insights reports that many banks and FIs have been predominantly reactive in their approach to tackling cases of money laundering, tending to have understaffed and under-skilled teams and are often weak or lagging behind when dealing with red-flag cases.

There is, therefore, no doubt that there is ever greater pressure from the regulators across the globe to drive enhanced and more proactive onboarding, KYC and AML protocols and improved outcomes. The institutions require a more robust internal compliance culture, and there needs to be a collective awareness of risks, with individuals accountable or answerable at each bank and institution. And they must have robust, well-devised and effective policies and processes in place that will serve as a sturdy barrier to help prevent fines or even worse outcomes.

Addressing internal inefficiencies and poor practices

And the regulators appear to be right. There are many internal weaknesses in risk management and systemic inefficiencies leading to fraud, and this means the banks and FIs are often struggling to meet heightened regulatory expectations on AML. And it is no longer simply a case of the regulators checking processes and ticking boxes – today, they want to see actions and outcomes. AML programmes must therefore become far more proactive rather than incident-driven, which is no longer adequate today. The older reactive approach is simply not good enough nowadays.

The wealth management industry in Asia has come a long way in raising KYC and AML standards and awareness, but the targets are constantly shifting, and the wealth industry must remain agile and able to constantly learn, adapt and improve in order to raise standards further.

Driving change, delivering improvements

The regulators of the major offshore financial centres in Asia – the Monetary Authority of Singapore (MAS) and the Hong Kong Monetary Authority (HKMA) - are certainly at the cutting edge of driving the banks and other FIs to create and maintain robust compliance regimes in place that can quickly adapt to the rapidly evolving and immensely complex modes of AML attack and the broader risks associated with financial disinformation and potentially crimes.

Education, in-house and external training, and a clear focus on raising capabilities are all essential elements. Indeed, today compliance, in general, has shifted significantly from being a back-office function to a vital component of any successful wealth management competitor.

The carrot and the stick

There are financial dangers in the form of fines, and there is the longer-term reputational damage that can occur, even to the major global banking brands, if they are involved in contentious or very public compliance crises. And this is precisely why the concept and practice of collective responsibility must be deeply embedded within each organisation.

Naturally, technology and the right tools can potentially significantly boost the ability of the client-facing bankers and advisors to obtain the right information and right from the very start of the onboarding process. But such technology must be well-chosen, proven and user friendly for those key individuals in each bank or firm. Soft communication skills are also vital in order that these in-house advisors and experts can indeed mine the right information out of their actual and potential clients.

Relieving the pain points

It is widely and fairly acknowledged that the KYC processes remain fairly manual and often archaic in approach and that they can be improved significantly. A pain point, albeit a necessary hurdle already, the wrong processes and a laboured approach by the banks can make it even more off-putting for clients.

Banks and other providers need to look for the smartest and least ‘painful’ means to access identity information and other easily accessible documents. Moreover, as the client continues their wealth management journey, this information can be combined and analysed to help significantly improve the client experience, resulting in greater loyalty and the potential for a larger share of their investment wallet.

Changing attitudes and practices

There are of course plenty of impediments to the achievement of these goals, such as the unwieldy legacy bank systems and the lack of internal coordination and the ‘silo’ type culture at many of the larger FIs.

The compliance teams often fail to communicate regularly with the client-facing bankers and advisors, the marketing teams do not leverage the data and resources that might be at their fingertips, the back-office transaction processing team are not discussing enough with the compliance and marketing teams, so on and for forth. And all of these shortcomings weaken the ultimate client experience and proposition, as well as wave a major red flag to regulators who need to see a more coordinated effort to drive data and reporting for KYC, AML, CRS, FATCA and AEOI, as well as for other important compliance purposes.

The right culture and the right tools

Nowadays, every wealth management firm has some degree of KYC and AML tools. If they are the right ones and if they use the latest technology, they can greatly complement the rules-based approaches and manual labour approaches that have dominated in the past.

There is a huge amount of data required for KYC/AML, including of course SOW information. And there is a lot of data analytics needed, with digital tools available to map out all the data, pull it all together, sort it, analyse it and hopefully uncover the key interactions and links between the client and their past and recent actions and different parties are.

Part of this is, of course, spotting changes in behaviour and identifying patterns, and weeding out anomalies that raise flags, helping the experts at the banks and other firms to then mine down into whether or not such flags can be dismissed or elevated to truly deep red status. The reality is that without this type of approach, the relationship between providers and clients will always be built on shaky ground.

Hubbis: What are your main challenges gathering Source of Wealth information today?

We have summarised some of the replies as follows:

- Client reluctance to provide Source of Wealth documentation.

- Respecting client privacy and not wanting to offend the client by probing too much.

- Tracing back to the actual sources of funds from different layers.

- Time and money

- Regular impression of information being concealed.

- Clients' refusal/resistance to provide information/documentation as they do not understand the need for such information to be provided as part of our mandatory KYC obligations.

- Incomplete information provided.

- Immediate certification/authentication of documentation is difficult to obtain.

- None. Our digital transformation is very advanced. Most clients are digitally savvy and communicate with ease via digital channels.

- Geographic uncertainty regarding assets and information in different countries.

- Inability to meet face-to-face for missing elements in the information gathering prohibit a smooth process.

- When requesting for information past statute of limitation periods and going as far back as 10 to 15 years makes it especially difficult as much of such information is not yet digitised.

- This is not specific to Covid, but institutions presume everything is available online. Many older clients have no online or historic records of their source of wealth required by institutions applying today’s standards of record keeping.

- The lack of direct meeting with clients and overseas peers and other service providers.

- Client delays, the poor formatting of documents, the certification of statements.

- It is often more efficient as well as more effective to gather source of wealth data in face-to-face meetings, but in times of Covid-19, clients/prospects may not be willing to meet. With video calls, some but not all of the inconvenience can be minimised.

- Lack of open sources and references to verify the declared sources of wealth.

- Obtaining corroboration of the source of wealth from clients, especially revenue/tax documents.

- Regulatory expectations of historical information to be gathered as part of source of wealth analysis are too onerous. In particular, this is difficult for second generations of wealthy families, where the wealth was generated by previous generations.

- Maintaining privacy for clients is extremely difficult.

- Authentication of documents and finding the right talent/staff to conduct this properly is far from easy.

KYC is not static, it is continuous

Moreover, this is an ongoing mission, as it is vital to continue to look carefully into how the clients interact during their whole wealth management client life cycle. What are the transactions? Are there regular changes of note? Changes of phone numbers, email addresses, addresses, even countries/jurisdictions? For all such information, technology solutions can and will help greatly in identifying anomalies and irregularities, but of course the processes, team formation and a generally positive and committed compliance culture are also essentials.

But let’s face it, the onboarding of clients is the main bottleneck today, especially in the remote working and travel-impaired world that we continue to live in today. Once clients are onboard properly, it is far easier to update client data, as well as easier to check for anomalies and to then monitor transactions and activity. And at the onboarding stage the key issues centre around verification of SOW and making sure as best as possible that the information supplied by the clients matches with public or other records that the banks or wealth management firms can obtain.

Boosting the single client view

The single client view is a key building block as it brings together all available data from a range of KYC information, transactional records, behaviour/activity, as well as disparate marketing and customer service channels, thereby offering an accessible, aggregated view of all of the data a wealth management company has on a customer. This is also highly appreciated by the regulators, as it offers a one-stop, holistic view of the customer, historically as well as currently, and combined with SOW data and ongoing transaction monitoring can provide a truly bird’s eye perspective for the banks and FIs, as well as for the auditors and regulators.

Turning negatives to positives

The reality is that these many onerous requirements can if properly managed, be turned to as much of a positive as possible to boost the client experience. And this is why it is so obviously in the best interests of the banks and other providers to coordinate more effectively and with better collaboration internally.

If the right data can be shared with the different teams and is in a manageable, accessible format, that will surely enhance both the outlook for the providers and for the clients through their wealth management journey. The banks and other firms learn more about their clients; the clients receive a more tailored, personalised, proactive and relevant set of products and ideas. This type of win-win situation can emerge from smart KYC and ongoing information gathering and analysis.

There is also the potential for the banks and others to form alliances with partners, for example luxury goods makers, airlines, travel companies, or high-end distributors that can then align their offerings more closely to these clients, of course, without obtaining any confidential information or breaching data privacy protocols. AI and machine learning technologies can help mine and analyse all this data and make sense of often disparate information coming in from a wide variety of sources.

Sowing the right seeds for the future

SOW protocols are understandably central and extremely important to the early stages of the onboarding, and this flows through to the future client relationship. Conducting source of wealth reviews is as much an art as a science, designed of course to encompass all sources of wealth – from inheritance to company creation and later sales, successful property investing, high-flight salaries plus annual bonuses and stock options, so on and so forth. And at the same time, the process, if conducted efficiently and cleverly, should help to reduce the burden on the providers and the clients as much as possible.

Seeing the connectivity also to the ongoing transaction monitoring and activity is also an essential element, with technology available to leverage the processes and the outcomes, producing better information, more verifiable information and reducing the number of false positives. Ultimately, if the right approach to SOW and, more broadly KYC and AML can be achieved, then the banks and FIs can turn a regulatory burden that is spread across every single player into a differentiating factor that can help elevate the bank or firm above its peers.

Again, if the right approaches, processes, internal coordination and technology are employed, the single client view is elevated, not only boosting both the relevance of the advice and ideas and therefore the potential revenues to be derived from the clients, but also helping win plaudits, or at least approval, from the ever watchful and increasingly proactive, even invasive, regulators.

From holistic to relevance and loyalty

The single client view that offers a genuinely holistic view of the client’s accounts, historical SOW, current activities and transactions, will really help the providers build these relationships by demonstrating to them that their needs and expectations are well understood and that the different internal elements of the banks and firms are attuned to these and delivering at all the various touchpoints.

And of course, in the global world of HNW and UHNW clientele, the ability to do this across borders and across different jurisdictions is increasingly important. Very wealthy families will very often have family members, homes, businesses, investments and lifestyles spread across several countries.

Hubbis: Has the COVID-19 crisis already had a substantial impact on your ability to gather Source of Wealth information from new or existing clients? What do you expect to happen in this area in the next 6 to 12 months?

We have summarised some of the replies as follows:

- Yes. SOW information will remain hard to obtain

- Yes and no, it depends on the countries, their situations and the governments.

- It could be worse over the next 6 to 12 months.

- Not really.

- Yes, we anticipate longer delays in obtaining information and/or documents from clients.

- Partially impacted

- Virtual meetings help, and we expect this situation to continue well into 2022.

- We are not suffering any significant impact currently.

- A challenge particular to Covid-19 has been obtaining certified copies of documents and records; sometimes, this is simply not possible, given the travel and WFH requirements.

- Certainly, but we expect that situation to improve in the 6 to 12 months.

- Not substantial, but significant...I believe this will improve.

- Not so impactful because of the difficulty in finding new clients during the pandemic. For existing accounts, many clients have more time on hand and hence will call quite often to chat and eventually share more information on their personal circumstances.

- Video calls continue to be an important tool in client engagement.

- Yes, for both new and existing clients as we are unable to meet clients physically. Some UHNW individuals do not trust virtual meetings. These problems will persist in the next 6-12 months.

- Yes, cases where source of wealth is hard to verify have increased since Covid. We think this problem will continue for some time ahead.

- Without the face-to-face contact, there is not the level of trust required to confidently build the information for both parties.

- As intermediaries not able to have face to face meetings with customers, there is no doubt that some new technology and/or AI solutions are needed to solve some of these issues.

Remember – don’t waste the opportunity

The downsides of not getting onboarding right are many. During the onboarding process, this is a period of lost opportunity, as there is no revenue for that period. Even worse, the entire onboarding process, if conducted badly, might drive clients away. If wealth managers make the mistake of turning the onboarding process entirely over to administrative staff, perhaps supported by a somewhat archaic legacy platform, the clients can be immersed in a slow, cumbersome, complex, confusing, often repetitive and frustrating machinery that can be very impersonal and off-putting.

Under these types of circumstances, wealth managers risk losing the client before he or she is fully onboarded. And remember, this is a delicate and annoying period for these would-be clients, so they are prone to being fickle potentially at this stage.

Asia and ‘new’ wealth

Remember also that in Asia, many emerging market clients are from new money, and often unfamiliar wealth management, and the wide array of investment options. And even sophisticated clients will need extra help. Yet, it is often hard for wealth managers to know if a client needs help if they pass the whole process and responsibility over to administrative teams who are not personally invested in the future revenue streams from those clients, and if the banks or firms they work for are more of the silo mentality.

To make matters worse, younger generation clients have lived all or most of their lives in a digital economy that often provides near instantaneous customer service. Therefore, an onboarding process that takes several weeks or months, which is awkward and repetitive, will definitely frustrate that client. Using the latest communication tools is also important and useful. Take for example, the highly digitised new Chinese client wanting to onboard with a private bank in Hong Kong or Singapore – they will be extremely used to the chat apps and to offer secure communication through their preferred apps and media can be a real plus-point.

The generation game

The importance of wealth and estate transmission from older to younger generations should also not be underestimated. Inter-generational wealth transfer is moving ‘older’ money to ‘newer’ money, for example, parents to children or parents to grandchildren and so forth, and the process that is taking place in Asia is worth literally trillions in the coming decade. There is much evidence that a considerable percentage of holders of ‘new’ or inherited money will change wealth managers when they inherit their wealth.

This is an opportunity for the wealth industry, but also a threat to many as the younger generations seek out different banks and firms from their parents or grandparents. But if they experience rotten onboarding at their chosen new provider, they might well quickly return to the original fold. As many of these people inheriting such wealth have grown up in a digital economy, they are most likely to be driven away by an outdated and irksome onboarding process.

Hubbis: Have you looked into using technology solutions to aid sourcing corroborating information, particularly from public sources within the Source of Wealth space?

Comment: All replies indicated that technology could or should help in checking and corroborating information from public sources. However, while some are using such tools, some are analysing their efficacy, and many noted that information of more than 10 to 15 years old is very tough to confirm. Some respondents commented that it takes time for the banks to trust and adopt the technology and time for the clients to trust the institutions sufficiently to deliver the information in the first place.

Maintaining privacy and security

Another vital area is security and privacy. Nothing will be more destructive to a potential wealth management relationship than data leaks and poor cyber-security practices. Accordingly, the culture of privacy and good data security must be embedded deeply within the banks and firms at all levels and in all the different teams. This involves not only the right technologies and software but the right internal approach to service quality and good practices. Data security and privacy will remain as top concerns and are absolutely crucial for all stakeholders in wealth management.

KYC and cyber-security

Today’s finance organisations need to understand and be heavily involved in an enterprise’s overall security measures and data protection strategies while monitoring data security, privacy and governance related to all finance and accounting data and activities. As part of this, they should consider mechanisms for monitoring and responding to changing internal customer expectations and demand regarding the financial analyses and insights the finance organisation produces to help their business partners and clients make better and more forward-looking decisions.

Capitalising on the Cloud can help, and the notion that organisations with on-premises hardware and data storage are more secure than those adopting the cloud is an incorrect assumption, as evidenced by numerous security and data breaches that have occurred the past several years. But the relationship and organisation of the Cloud-based data management must be extremely well handled, with clearly defined roles and responsibilities with regard to access, provider controls, key controls and more.

The final word

Source of Wealth improvements must be seen within the wider context of enhancing KYC and making the ongoing compliance commitments of each wealth management institution smarter and more efficient. Achieving a faster and smoother onboarding and periodic review experience, which offers a high level of automation coupled with 'straight through processing' (STP), ultimately reducing many of the friction points associated with traditional KYC and AML processes are all vital elements that must be deeply embedded in the cultures and practices of those providing wealth management services.

The more efficient the automation that can be achieved, the better the outcome, as there is no doubt that demands have increased dramatically and KYC costs have risen significantly over the last decade.

Technology is a key building block in moving the industry towards more rapid and efficient onboarding, but also ongoing or perpetual KYC, which the regulators are essentially demanding these days, even if they do not quite state that outright. But so too another key is the right internal practices and culture and management commitment – without the right levels of communication and cooperation internally, many key elements, including of course SOW protocols as part of KYC and AML can go horribly wrong.

Faster, cheaper, more effective solutions clearly require upfront and ongoing investment, but they should be seen as a longer-term gain for reputation, quality, integrity and client satisfaction and loyalty. And with social distancing likely to remain in place in the post-pandemic world, firms depending on paper-based ID checks will need to switch to remote, digital, e-verification processes in a bid to keep their businesses running efficiently. In short, the more seamless and efficient the onboarding and ‘perpetual’ KYC, the better it is for all parties.