Publications & Thought Leadership

How Will the Incumbents and the Challengers React to the New Digital World Ahead?

Jun 5, 2020

As we all emerge extremely tentatively from lockdown, it is becoming clearer that in practical terms, doing business will likely not be the same in the future as it was pre-2020 for financial institutions, as a considerable number of the rules and restrictions will likely stay in place, creating a new normal. The virtual panel of technology experts Hubbis assembled for its May 28 Digital Dialogue event explored the post-pandemic environment, gauging the digital health of the incumbent banks and other financial institutions to determine their ability to survive and thrive in wealth management in the years ahead. Will they be challenged by the neo-banks? Will those challengers, when they are fully operational, have an inherent advantage in this scenario? Have the Hong Kong and Singapore regulators got it right in terms of the neo-bank licenses? Will the use of digital identity applications ease and speed the remote KYC/onboarding process, and at the same time, meet practical cyber-security and privacy challenges, as well as compliance requirements? Will the digital banking arms of the bigger banking groups be able to exploit their brand-name and reputational advantages to fight off both the neo-banks and other challengers, for example, the ranks of FinTechs or the might of Big Tech? Can digital enhancements enable wealth management institutions to truly deliver products, solutions and advice remotely? And what needs to be done amidst the ongoing social distancing demands to adapt platforms to the potential landscape of the post-pandemic world? These and many other matters were discussed in the engaging and insightful 1-hour discussion, which was split into three presentations, a panel discussion and a Q&A with the virtual audience.

Moderator

Andrew Chow

Regulatory Compliance, Legal, FinTech & Digital Banking Practitioner

Speakers

David Roi Hardoon, PhD

Senior Advisor for Data and Artificial Intelligence

UnionBank of the Philippines

Pranav Seth

Head, Digital & Innovation

FRANK by OCBC

Wong Nai Seng

Regulatory Risk Leader, SEA Risk Advisory

Deloitte

First Presentation: Setting the Scene of the New Normal

David Roi Hardoon, PhD, Senior Advisor for Data and Artificial Intelligence, Union Bank of the Philippines

“My talk is about banks innovating for the digital era,” Hardoon began, “and as we know, there are many dimensions which an organisation, a bank, or a financial institution will need to consider as part of its transformation to digitalisation. For this presentation, I will focus on the three dimensions I consider to be absolutely crucial.”

First, however, he set the context, explaining that the current immersion in remote working, virtual events in the form of webinars, and socially distant connections to colleagues and clients are an expedited version of a trend to a new norm that had pre-existed this virus, as financial institutions adapted to deliver financial services to as broad a demographic as possible, and as seamlessly as they can, focusing both on internal efficiencies and the end-user experience.

“To give you the context for example in the Philippines,” he explained, “we are a country of over 109 million Filipinos, in which around 65% are unbanked or underbanked, where 93% have got no credit card, and in which 80% of the bank loans are to corporations. So, as you can imagine, there has long been a near-desperate necessity to make sure that the services and provisions are actually provided to these people. This crisis has, in fact, simply accelerated this very pressing and pre-existing necessity.”

Three pillars

And with that comment, he expanded on the three underlying key pillars that he considers crucial in this new norm and crucial as part of the digitalisation agenda.

The first pillar, he explained, is about driving the mobility to consumers, whether those are consumers from a retail perspective, through a customer app, or through providing a similar type of service, a similar type of experience to SMEs and larger corporations.

“We have seen a 2700% increase at the bank this year in online onboarding, and we now want to continue that drive, to bridge the gap and achieve greater practicality,” he reported. “Mobile banking is all about extending services to people; to help that, we are seeing also some changes to the regulatory landscape in how to facilitate those.”

He then talked briefly about the technology of blockchain, which if applied properly he said will significantly boost the trust element for customers. With that, he showed a slide highlighting how blockchain-enabled settlements and payments were put in place to connect the numerous rural banks in the Philippines for transactions and payments via a pilot scheme using Stablecoin, essentially a digital substitute for the Philippine Peso.

“Stablecoin, which is a pilot scheme not yet proof of concept, is supported by blockchain and will facilitate payments across the network,” he explained. “Thus far, almost one-third of the rural banks, 141 of them, have signed up, and 57 are already transacting amongst each other and soon to be actually incorporating it with mobile ATMs.”

He added that there are other solutions providing similar digital transactional capabilities, all based on the same underlying blockchain technology and generating trust across logistics, interactions, supply chain, and digital identity. “And of course, for compliance too,” he reported, “because the other element in instilling this trust all the financial institutions and customers need is not just providing those underlying services but at the same time having that vital transparency for compliance and audit purposes.”

The third pillar, he then explained, moves beyond open banking into this new quarantined world, allowing the financial institutions the flexibility and predictability they need to operate in an ecosystem and thereby providing the ability to interact and to have full inter-operability. “There are numerous potential possibilities in how effectively a bank can transform and become a tech company,” he observed, “or perhaps more of a tech company that does banking in the future, rather than simply being a bank that does technology.”

Accelerating the digital journey

Hardoon summarised his views by commenting that what the pandemic has done is, therefore, to bring a new normal nearer by accelerating what has already been ongoing from the transformational and technological perspective. “But it is not just about adopting technology,” he commented, “it is also about the cultures and mindsets of institutions. We must all make sure that we understand what we are doing and that we are able to fully operate in the forthcoming environment, by constantly digitalising for the future.”

He drew his brief talk to a close by remarking that such a transformation doesn’t happen overnight. “The reality of the matter is that one often needs to create API layers on top of legacy systems, in order to make it possible to get the required data and information moving in a transient and efficient manner from one point to the other. And as I said a vital key is culture, so suddenly leaders have been more clearly seeing the challenges in full focus for themselves, and more clearly realising the true value to be attained at the end of this process, even if painful to reach that point.”

He explained that in the case of UnionBank, the group has been on its digital journey since 2016, building the means to operate nationwide in a very agile manner. “Now it is also all about how we capitalise on this virus-enforced necessity today to make sure that once we go into the new normal in the post-pandemic environment, we do not go back to the old normal, and we make sure that we continue to build this infrastructure, we keep building up these services even more effectively,” he concluded.

Views from the Post-Event Survey

Hubbis: What do you think the new normal in banking will look like?

The Audience’s Replies:

“After Covid-19, banking will be much different than it was pre-pandemic. The change in the way people bank, the future of work, the use of modern technology and the value of brands will all depend greatly on the time it takes to settle on a 'new normal'. A look into the future provides a good foundation for what needs to be done today.”

“The traditional method of banking is extremely inefficient and needs to step aside for the new age. It is extremely time-consuming to personally go to banks, whether it may be using the machines or the teller/RM services. The much more convenient option is to have everything conducted on the smartphone. Wiring money is far better than writing cheques, but it seems that not all banks are on the same page with that idea. Not to mention a lot of government agencies, regulatory agencies, and/or other companies do not have the proper infrastructure to support such a major transition in society. I understand that some banks still have a hard time accepting virtual cheque depositing, which seems like an interesting first step into this major transition. At the end of the day, there should be a decline in brick-and-mortar banking and branches, for certain.”

“Being in client-facing roles while managing the operations, Covid-19 has forced a new perspective to how things can be done. Gone, perhaps are the times when competition drives you to make physical trips to meet clients, use technology for communication instead. Many clients, at least from our end, have seen the advantages, for example, as we are able to showcase a lot more data and information including Bloomberg screens to illustrate situations and ideas to them. This may change a lot of trends.”

“We will see more working from home, smaller offices, more hotdesks, continued compression of fees, faster digital evolution, and a rise of e-solutions for clients. More virtual meetings and presentations.”

“I would like to think and hope with lessons and new things learnt that are workable digitally during this period, and management would be able to streamline processes and procedures more efficiently and digitally.”

“For a functioning global economy, a functioning banking and payment system is vital. The financial services industry is facing another shock after the financial crisis 2008/2009 with shrinking revenues due to lower consumer and business spend, lower interest rates, increasing credit risk and volatile capital markets. The New Normal will see banks prioritising and driving digital banking and payments to meet the increasing demand for remote/online and mobile solutions, opening up new digital onboarding capabilities for any type of banking service and investing in open banking capabilities to collaborate with FinTechs, and speeding up the implementation of their digital banking agendas.”

Hubbis: What are some key challenges that you face during this circuit breaker period?

Distilled Audience Comments:

- Low team morale

- Lack of personal client meetings

- Poorer IT equipment and internet outside the office

- Weaker generation and maintenance of corporate culture

- Lack of direct interaction in the normal working environment.

- The difficulty of client generation/acquisition

- The difficulty of obtaining personal insights to clients

- Hurdles in handling legal documents

Hubbis: Can split operations really work on a permanent basis?

The Audience Replies:

“Hardcopy documents still have to be reviewed and processed by operations which can be of the cause of delays. I would believe if there are good processes within the bank, split operations could actually work.”

“The challenges are mostly minor and revolve around technical or operational issues that can be resolved with a few phone calls. I believe split operations can work on a permanent basis. No doubt it would be good to be able to see colleagues once in a while.”

“Yes, split operations can really work; however, the desire to interact face to face with another human will not 'go away' overnight, as personal meetings offer the ability to read body language, which is not really possible via video. Similarly, there is a need for human validation on important issues.”

“Yes, split operations can work on a permanent basis, provided there is a nucleus team that is based at HQ, to act as the hub to the spokes. Outsourcing at the banks has been in place for years. However, for this to successfully take place, top management must commit capital to bring about automation that is suitable for the 21st century that is client-centric and addresses changing lifestyle trends that include on-the-go mobility, that offices and work take place virtually everywhere and 24/7.”

“There is still too much paper, and documentations need personal sighting for verification. The solution is for compliance to start thinking out of the box so that they can assist the business to simplify processes which will still uphold compliance.”

Second Presentation: Digital Acceleration to thrive in the New Normal

Pranav Seth, Head, Digital & Innovation, FRANK by OCBC

Seth began his talk by noting that OCBC is today far and away beyond what it was years ago, namely a brick-and-mortar bank. “While we are certainly an incumbent bank, 95% of our transactions are today drawn digitally,” he reported, “and as the former speaker indicated, these transformations do not take place overnight. Specifically, and of course, you must have the infrastructure required to support a digital transformation of the scale that we are talking about, but you also need a vision in place, which we have been embracing for some years already on this journey.”

He explained that he himself has been ‘preaching’ to more and more digital converts within OCBC and outside for more than ten years. “What we are seeing in this lockdown, of course, is a dramatic acceleration due to the pressures of social distancing, being unable to conduct business in the traditional forms, but I believe in any case there has long been a huge need to accelerate the transformation.”

A long and difficult journey

“Those banks and organisations,” he continued, “that have been systematically upgrading their infrastructure, their API layers, their database systems, creating microservices that can be reused much more effectively, no matter what the form factor, whether it is on the phone, whether it is on a smart-watch or whatever might the form factor might be, it is those organisations that have been consistently investing in the modernisation of the technology stack which definitely has a greater ability to accelerate their digital transformation than any organisations starting late, or worse still, starting right now.”

In short, he observed that technology architecture is a long-term build. “For anyone that is well behind the curve,” he cautioned, “this has been a real wake-up call. For any of the incumbent banks who are behind the curve, they must be ready for the new age; the battle is essentially theirs to lose.”

Digital transformation in action

And with that, he offered delegates a series of slides which highlighted OCBC Bank’s true digital transformation, as well as showing how dramatically digital connectivity, advisory and transactions had increased this year across the board for the numerous retail, SME and corporate customers of OCBC.

He closed this section of the talk by offering the virtual audience a comment ascribed to a certain Clarence Darrow, a US lawyer famous in the 1930s, who was on record as stating: “It is not the strongest of the species that survives, nor the most intelligent, but rather the one most adaptable to change.

Digital Identity

Seth then focused the audience’s minds on the role of digital identity and non-face-to-face technologies in helping achieve digital acceleration.

“The most basic reason why people used to come to the bank branches was to open accounts,” he noted. “But with digital identity solutions, we can now do remote onboarding without the need for people to walk into a branch. For Singapore, pre-COVID, we were already doing 30% of all account opening online, and that number has now shot through the roof given that the branches are closed. We have SingPass and CorpPass, which I see as the gold standards in the region, if not the world; they are the keys to unlocking the flow of data in an economy, in a digital economy.”

He added that the major goal in digital identity today is to create standards around all disparate government systems in the region to work towards an inter-operable system. “From our point of view,” he reported, “I think this is best done by government systems; as an organisation, our position is definitely to go with the government-backed digital identities. This is vitally important in being able to provide solutions, loans, other products at speed, digitally. Whether these are in relation to accounts, auto finance, credit cards, personal loans, with digital end-to-end delivery, to your accounts or in your mobile wallet. The question therefore is how fast can incumbents continue to digitise all their products using a digital ID.”

Seth also highlighted the growing need for remote advisory and sales. “For OCBC,” for example, “for a lot of our offshore business we need to onboard customers digitally, not face-to-face, but of course there are problems inherent. We have therefore enabled our premier customers to do secure video chats, voice chats, and so forth, to make sure that the sales process can continue to operate, and as we go along, we are adding more segments and more products to it.”

Of course, he explained, this has huge implications on the validity of signatures, where the signature is needed, where is the signature not needed, and this depends partly on the type of product, for example, whether simple products where a verbal acceptance that is recorded is good enough, or perhaps life insurance products where the terms and conditions and the features of the products are complex and where some of the authorities and agencies still insist for signatures. “This,” he advised, “means that the financial institutions must, therefore, adjust to this new reality, with very rigorous rules around digital signatures.”

He added that there is a need for the industry to also engage new customers who are not so digitally savvy, to ensure they are not left out in this digital world, whether perhaps poorer or less educated, or older and more distrusting of technology. “Moreover,” he commented, “the providers must work hard to ensure they understand and react to lifestyle and behaviour patterns of their customers, and provide ideas and solutions linked to those data-driven assessments.

And he also highlighted how digital transformation could help improve areas of activity such as climate change resilience, food security, sustainability, and the future of the workforce.

“We need to see the banks take an elevated outlook, helping all types of customer navigate this crisis and their futures,” he commented. “We know that unemployment rates globally are soaring; we expect to see more of people’s inability to take care of their basic needs. Loans could come under pressure, and banks will need to react with loan moratoriums, additional loan lines, and other approaches, and all must be done digitally. Credit management post-pandemic will also be crucial given the fragility of the economic environment, so that is a key challenge for the incumbents and for the neo banks alike.”

His final word was on security and privacy. Security is also a key consideration. “Everyone working from home creates new challenges, creates new threat vectors, creates new abilities for fraud, unfortunately,” an expert explained. “We have to have the digital means to detect patterns and anomalies; we are in the business of managing other people’s money, so this is a critical area.”

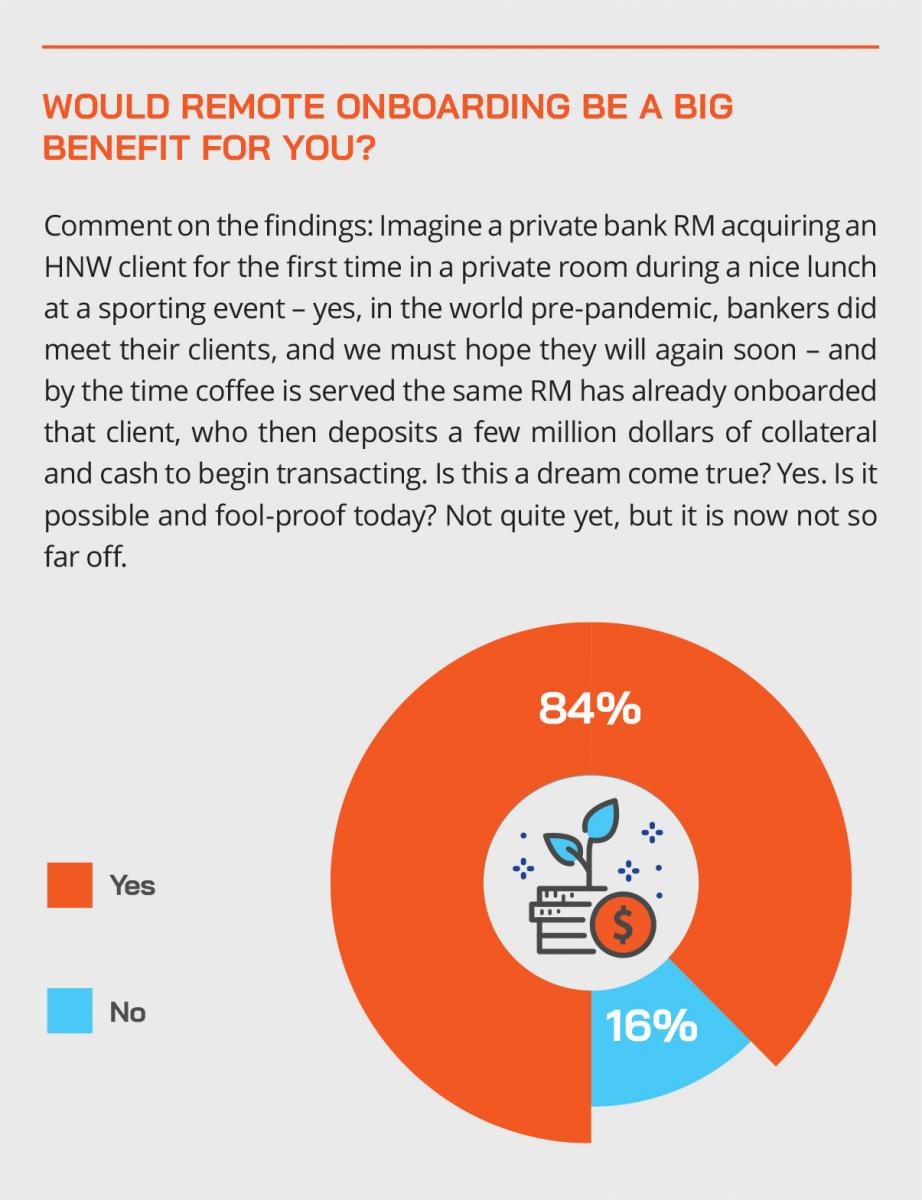

Imagine a private bank RM acquiring an HNW client for the first time in a private room during a nice lunch at a sporting event – yes, in the world pre-pandemic, bankers did meet their clients, and we must hope they will again soon – and by the time coffee is served the same RM has already onboarded that client, who then deposits a few million dollars of collateral and cash to begin transacting. Is this a dream come true? Yes. Is it possible and fool-proof today? Not quite yet, but it is now not so far off.

Third Presentation: The State of Play for the New Digital Banks in Singapore and Hong Kong

Wong Nai Seng, Regulatory Risk Leader, SEA Risk Advisory, Deloitte

Nai Seng first ran through the current state of play for Asia Pacific regulators that have been introducing digital banking frameworks in their respective jurisdictions.

Hong Kong and Singapore have attracted significant interest. The Hong Kong Monetary Authority (HKMA) published the Guidelines on Authorisation of Virtual Banks on 30 May, 2018, and to date, HKMA has issued 8 digital banking licenses. The Monetary Authority of Singapore (MAS) announced its proposal to issue digital bank licenses on 28 June, 2019. There are 21 applicants for up to 5 licenses. Successful applicants will be announced in 2H 2020.

Elsewhere in the region, South Korea’s Financial Services Committee (FSC) has issued three digital banking licenses and has announced plans to issue more. Taiwan’s Financial Supervisory Committee (FSC) introduced virtual banking license requirements in 2018 and later issued three digital banking licenses. In Australia, the Australian Prudential Regulatory Authority (APRA) introduced the new “restricted” authorisation for new retail banks in May 2018 and later granted its first restricted license to Volt Bank Ltd.

Bank Negara Malaysia (BNM) issued the Digital Banking License Framework Exposure Draft on 27 December, 2019, with the feedback period extending to 30 June this year. To date, the Indonesian Financial Services Authority (OJK) has issued guidelines to manage the provision of digital banking services by commercial banks (Regulation POJK 12/2018, effective 8 August, 2018).

Objectives, controls and strategies

He then highlighted the differences between the digital banking regimes in Hong Kong and Singapore. “In Singapore, there will be 2 types of licenses, with up to only 2 digital full bank licenses and up to 3 digital wholesale bank licenses.”

Policy objectives, he reported, include financing growth enterprises and SMEs, reducing costs and improving convenience for consumers, helping people to plan early and achieve financial security in their retirement, creating jobs, and financing the growth of infrastructure and climate-resilient, low-carbon investments.

Over in Hong Kong, where there is only one type of digital banking licence, eight have been granted, with no specified limit on the total. Policy objectives include the promotion of fintech and innovation, offering new customer experiences, and to promote financial inclusion, covering the retail and SME segments.

Stepping back to survey the current and anticipated landscape, he commented that a core consideration for many regulators around the region for introducing digital banking framework is to encourage financial inclusion. This needs to be balanced against the current market structure. “In Singapore, we can surmise that MAS considers the market is generally well banked and does not want to create too much fragmentation, hence the limit to five licenses,” he explained.

He then ran the audience through the assessment and selection criteria in both jurisdictions, highlighting common elements across both Singapore and Hong Kong such as financial inclusion, the value proposition, technological innovation, having a viable business plan, adequate compliance and risk management, as well as other hygiene factors that need to be met by successful applicants. He added that Singapore also has a strong emphasis on creating jobs and developing the workforce.

Wong highlighted some differences in the regulatory approach, noting that Hong Kong has a uniform regulatory framework that applies equally to the digital banks business and the incumbent banks. In Singapore, there is a slight tweak, providing some latitude for the Digital Full Banks in terms of paid-up capital during the initial years of operation. Another difference is in terms of the ownership structure, with the MAS requiring Digital Full Banks to be controlled by Singaporeans, with no such restriction in Hong Kong.

He highlighted that several successful digital bank applicants in Hong Kong have a strong presence of incumbent banks as shareholders, probably due to the adoption of a defensive strategy by those banks.

“There is no similar trend in Singapore,” he explained, “because there is a separate framework for banks that want to setup digital banking subsidiaries; the MAS has made it very clear; if you are a bank and you want to set up a digital bank subsidiary, you can do so by the different framework, and you won’t be encroaching on the quota of five licenses that are made available under the new digital banking framework.”

He also noted that there are some other commonalities between the two jurisdictions, observing that the consortia formed or being formed are generally bringing together different partners with diverse capabilities, financial resources, technology, and different ecosystems of customers.

“We see combinations of financial institutions, technology companies, telecoms, platform operators, e-commerce firms, B2B platforms, real estate players and wealth management institutions,” he reported, “and of course we also see major tech firms going it alone as a diversification into new banking for the new world ahead.”

He added a word of caution for the challenger banks. “Covid-19 has delayed the license application process in some cases,” he noted. “Moreover, when they do launch, the post-pandemic economic environment could remain difficult, and perhaps their projections for building up their business and loan books might be challenged, therefore bringing to question whether they will grow quickly enough to attain sustainability.”

Incumbents – rising to the challenges

He then explained that the global pandemic has certainly introduced some new considerations in the digital banking discussion. “We have seen how some of the incumbent banks had to scale down their physical locations during lockdowns, and how consumers are now more familiar with digital channels and have developed greater trust and confidence in using these channels.”

Nai Seng also offered a comment to concur with an earlier perspective from a fellow speaker. “Apart from having the architecture, the technology, and the support as we heard before, the culture of the incumbent banks and institutions is also very important as they rise to the challenges of the new entrants,” he explained. “Some banks have been doing it for a number of years already, they have built up their muscle memory, and are therefore able to adopt a nimble approach across the transformation journey. Those starting later, or even now, will find the challenge that much greater.”

Fighting tough

“The incumbents will not be sitting still,” he continued. “They are certainly very much up for the challenge, with most making substantial investments in technology, to make themselves more nimble and better able to take advantage of the unique advantages that they have as incumbents. They have large franchises, strong brands, and a huge amount of trust with their customers already, so it is then a question of how effective they are at leveraging these advantages.”

He added that the first round of banking de-regulation in the late 1990s and early 2000s saw more foreign banks come in, but 20 years later the local banks continued to hold more than 50% of domestic deposits; in fact, during the global financial crisis they increased share as customers preferred their stability and that they are Singapore-owned and headquartered. A similar path is being tracked again in this pandemic.

It is therefore entirely up to the incumbents to be competitive, to stay ahead of the chasing pack. “There are existing and future competitors coming in, so it is essential to be relevant, competitive and to constantly identify the opportunities and capitalise on them,” he concluded.

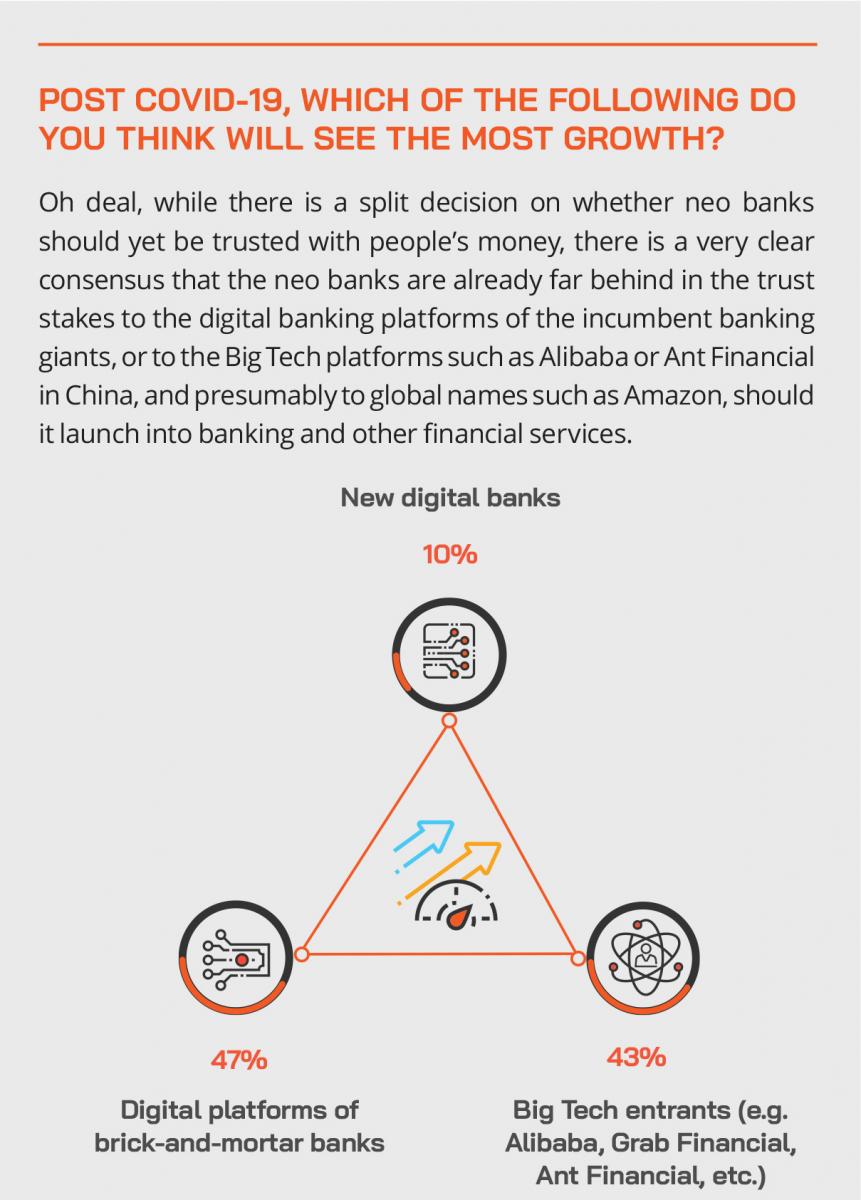

Oh deal, while there is a split decision on whether neo banks should yet be trusted with people’s money, there is a very clear consensus that the neo banks are already far behind in the trust stakes to the digital banking platforms of the incumbent banking giants, or to the Big Tech platforms such as Alibaba or Ant Financial in China, and presumably to global names such as Amazon, should it launch into banking and other financial services.

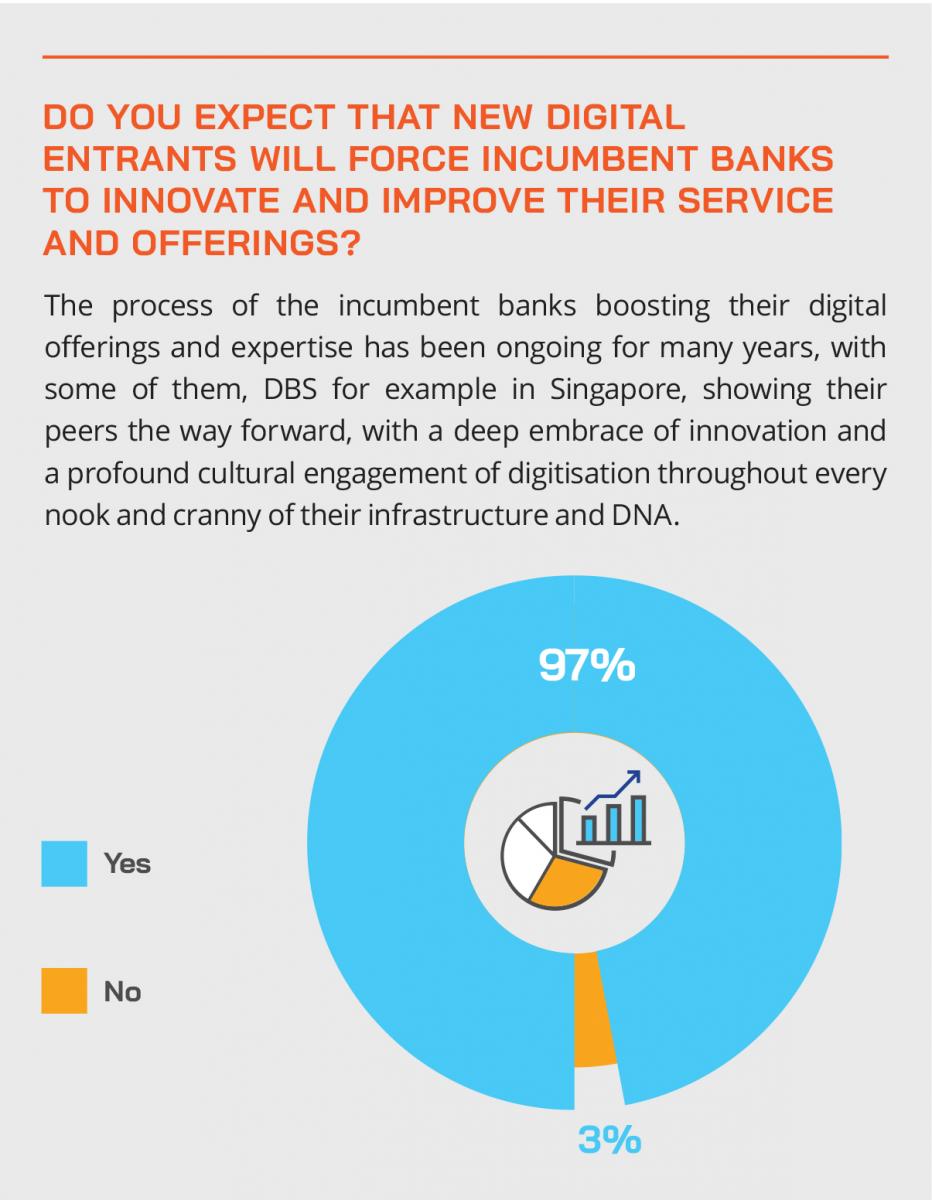

The process of the incumbent banks boosting their digital offerings and expertise has been ongoing for many years, with some of them, DBS for example in Singapore, showing their peers the way forward, with a deep embrace of innovation and a profound cultural engagement of digitisation throughout every nook and cranny of their infrastructure and DNA.

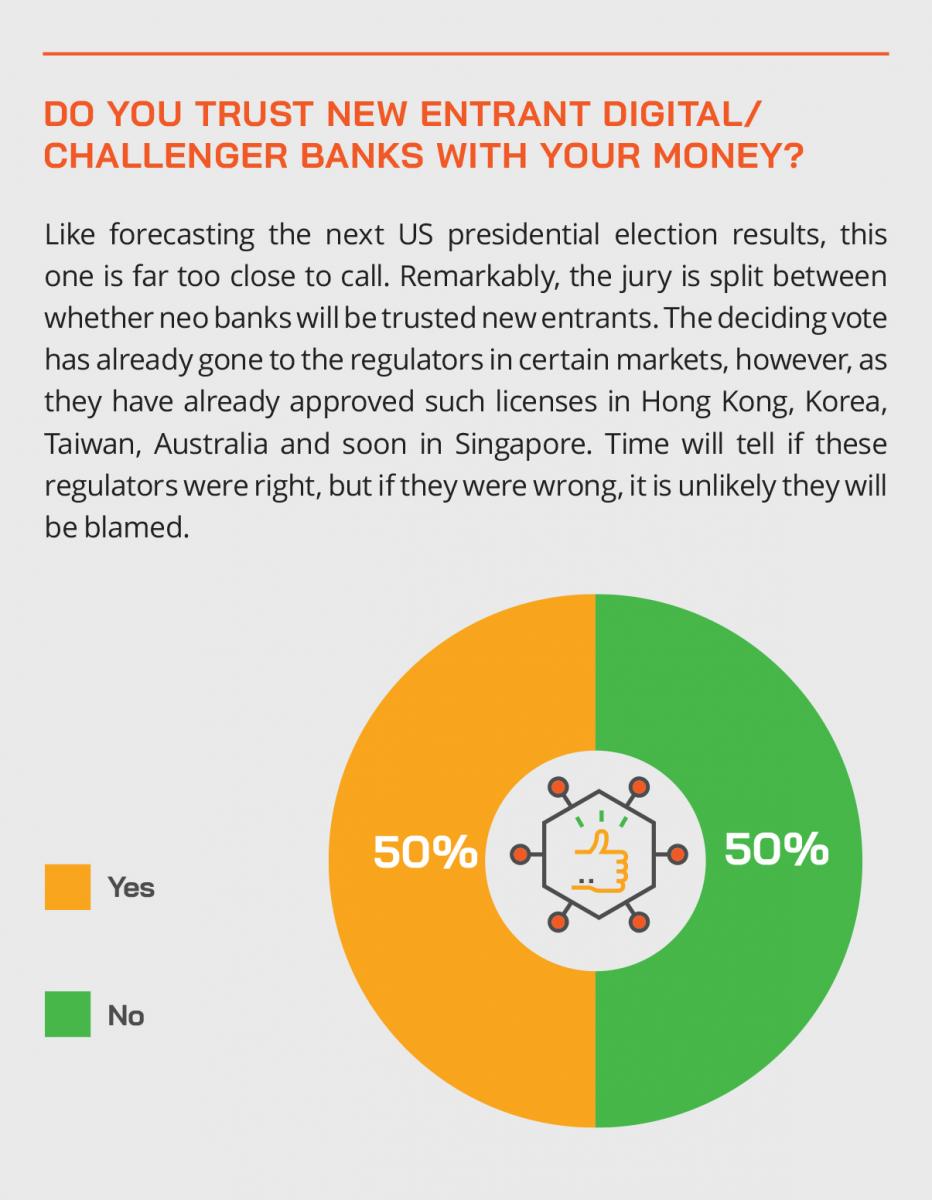

Like forecasting the next US presidential election results, this one is far too close to call. Remarkably, the jury is split between whether neo banks will be trusted new entrants. The deciding vote has already gone to the regulators in certain markets, however, as they have already approved such licenses in Hong Kong, Korea, Taiwan, Australia and soon in Singapore. Time will tell if these regulators were right, but if they were wrong, it is unlikely they will be blamed.

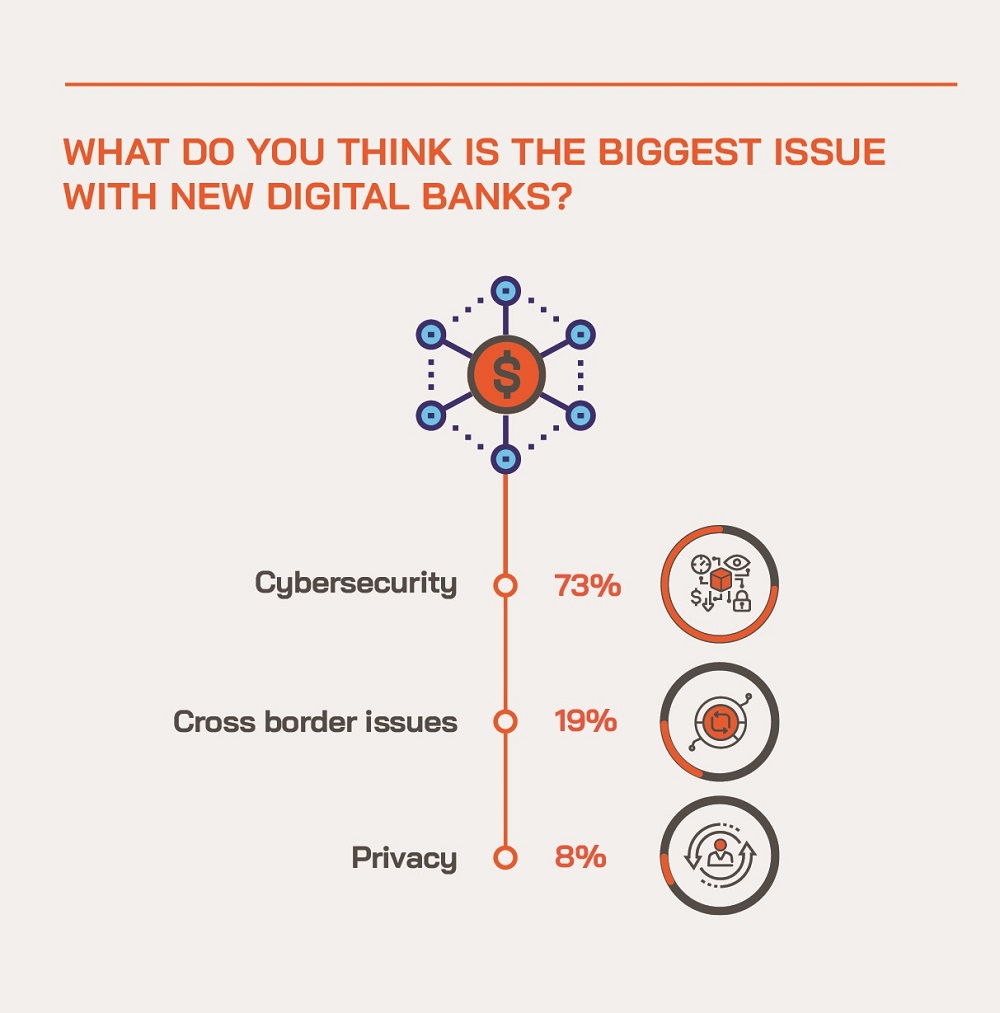

The Panel’s Further Insights on Digital Identity, Privacy and Cyber-security

There were then some questions form the audience mining down into more insights on Digital Identity, Privacy and Cyber-security.

A question came about the effectiveness from a compliance perspective of ensuring regulators approve of digital identity protocols. “It is quite funny really,” came one expert’s reply. “My four-year-old daughter can forge my signature, so why are we still having a conversation around physical signatures? This is something that regulators need to wake up and realise it's irrelevant. What is the next thing, they should be focusing on, rather than constantly retrofitting to something that we all know doesn't work?”

He also added that, of course, we should all work within the lines of government-confirmed digital IDs, because after all, he pointed out, we all work with those anyway, whether it is a birth certificate, driving licence, passport, marriage certificate or whatever else. “It is only the means of collection and authentication which differs as this can now be digital,” he commented. “Similarly, think about all of the challenges from a cybersecurity perspective, but don’t over-theorise, as there are plenty of shortcomings to the physical verifications we have long adopted.”

He concluded that what we all need to do is to disrupt ourselves, meaning that we disrupt ourselves to do things better, rather than accepting a process or whatever it was because that is the traditional norm, but perhaps not the best way. “There is no such thing as a fool proof solution in existence,” he said, “so we can react to this externally-imposed situation of the pandemic and fundamentally rethink.”

Views from the Post-Event Survey

Hubbis: Would you have any reservations with opening an account with a new entrant digital-only bank? If so, what are the reservations that you have?

Audience Replies:

“No, I have completed account opening with digital banks in the past. However, I usually won't put substantial funds with a digital-only bank as compared to traditional banks.”

“I am terrified of FinTechs start-ups cutting corners that should not be 'cut' and for them to

skip critical steps because they are not fully versed in the business.”

“I might not want to open an account immediately as I would like to observe how they pan out in a year or two.”

“I would not trust a new entrant versus an incumbent, although incumbents are going to need to get their act together to be more agile and nimbler, less bureaucratic and more relevant.”

“The provider must be reputable, controlled by owners I trust and licensed by the regulator.”

“Online security must be assured.”

“The neo bank must assure customers by demonstrating how they will be different in terms of products and services from what the traditional banks offer with their digital/online offerings; secondly, they must emphasise security, transparency and safeguarding privacy of data, and they need to demonstrate a ‘fallback’ process in the off chance that online access is not available.”

“Data confidentiality, privacy and internet security must be assured at the highest level, and as long as there is proper regulatory oversight, I would have very little reservations and would be more than willing to fully embrace digital banking and the opening of an account with a new entrant.”

Another expert took up any audience question about the particular challenges of digital data collection and privacy. “This actually cuts both ways,” he opined. “We should focus on the basics of hygiene factors that an institution needs to have in place to ensure that the data that they collect is properly safeguarded, properly used and that then is essential for building the trust with the customers, so they see that value in releasing the data and sees that the institution is trustworthy in its handling of the information. Then you move into the landscape of being able to collect more information, provide better insights to the customers and better and deeper relationships ensue.”

On this same point, another panel member said that given all the class action lawsuits in the past couple of years in the US surrounding data and privacy, institutions or anyone handling data must properly communicate the value exchange they extract in sharing that data. “That equation needs to be really clear to the customers,” he stated.

Views from the Post-Event Survey

Hubbis: Do you think that verification via digital identity platforms compromises your right to privacy? If so, why?

Audience Replies:

“Identity solutions are an integral part of the digital experience, and consumers want nothing to do with them. By authenticating users, these platforms keep fraud at bay, boosting trust, clicks, and sales. But they often require consumers to jump through hoops such as creating unwieldy passwords, for example, or entering verification codes from a second device. The seamless convenience consumers expect online is now like a trip to the dentist. As a result, many digital identity solutions aren’t as efficient, effective, or commercially successful as they could be. Consumers often decline to use more secure, but more onerous features like multi-factor authentication. Meanwhile, a number of large businesses - including some of the household names of the digital era - have opted to go their own way, creating proprietary identity platforms.”

“No, privacy is not compromised in my view. In fact, it seems like a logical next step that all companies are striving to move towards. It seems that during this indeterminate period of transition, government and regulatory agencies are uncertain as to which platforms they can officially accept as a legal form of verification. It seems that getting everybody on the same page has proven to be difficult as there are always double standards in the industry.”

“This is will increase the identity exposure risk even though the cyber-security technology has reached a new advanced level.”

“Information is already out there. When one signs up for membership to various services, for example, car rentals, food delivery, ride-sharing, one’s personal information is given and required. One needs to be wary of how each platform stores and utilises the information.”

“Actually, infringement is already quite pervasive currently. I don’t trust banks to keep my data private, so I practise a need-to-share approach in filling in forms, and question bank staff on illogical information requests. This is not going to change just because it is a digital identity platform. If it does not meet my comfort level, I simply don’t open an account or make transactions.”

And another expert pointed out that the danger very often comes from the weakest point in the chain, the Achilles heel of the organisation. “For example,” he said, “this might be a data or call centre in a low-cost outsourcing country that might be hacked or otherwise compromised. “And then we might see a domino effect throughout the organisation. But we are in the business of managing risk, so for us to not understand where the risk is emerging from is foolhardy. We need to ensure and keep proving that digital identity verification and validation is conducted in a fool-proof manner. We need to be transparent and offer traceability. To my mind, the government-driven digital identity approach will win over any private initiatives.”

A fellow panellist, however, pointed out that privacy can be a more complex issue, as people fear government interference in their private lives. “Now,” he commented, “there is a lot more focus both in terms as a player to understand how do I provide inter-operability, how can handle data with privacy, security, hygiene and so forth to allow for inter-operability, especially when talking about cross-border, and often across very different regimes, whether Singapore, China, Europe, America or wherever. These are some of the really difficult and absolutely critical questions.”

“Yes,” said another expert, “this requires an alignment of standards, although we are only at a very, very early stage in that endeavour, globally, and then we are talking about immense complexity, national pride, and so forth, so while it might happen and I think we wish for it, we are still far away from a solution, so in the meantime, I think we will just have to live with it.”

Conclusion

What had proved to be a remarkably detailed and thought-provoking discussion drew to a close with the virtual panel agreeing that the speed of digital transformation in the financial sector will now likely accelerate considerably in the months and years ahead. Any institutions that felt they could drag their feet and watch how digital transformation played out have had a startling wake-up call. Change is upon the financial and especially wealth management industry. Embrace change or risk being drowned by it.