Publications & Thought Leadership

How the Incumbents are Rising to the Challenge of the New Ranks of Neo Banks in Asia

Jun 2, 2021

There are more and more new ‘virtual banking’ entrants across the main economies of Asia, and other new licenses are either being issued or in the pipeline. There are some daunting estimates by some leading consultancies, Gartner, for example, that many banks across the world will be driven out of business by the rise of the Neo banks; hence the traditional and legacy banks and the incumbent wealth management providers ignore these developments at their peril. The ability of these Neo banks in the future to compete across a wide variety of products and solutions should not be underestimated, as they leverage AI, machine learning, data mining and analytics, as well as other technologies and processes to fight for market share in transfers, FX, credit, risk management, investments/trading, portfolio management, robo-advisory and personalised advisory, and in other key areas. Hubbis assembled a panel of experts offering immense expertise to provide delegates at the Digital Dialogue of May 27 with invaluable insights on positioning themselves for what is the seemingly inevitable rise of the ‘Neo’ or ‘challenger’ banks.

The Panel

- Karsten Kemna, Managing Director, Asia Pacific, CREALOGIX

- Kimberley Ho, Senior Vice President, Digital Wealth Lead, Consumer Banking Group, DBS Bank

- Adam Reynolds, CEO, APAC, Saxo Markets

- Damian Hitchen, Chief Executive Officer, Singapore, Swissquote

By 2025 some 65% plus of banking customers in Asia-Pacific are likely to use some digital banking services offered by Neo banks and Challenger banks, according to one expert on the panel. Accordingly, he said incumbents will need to adjust their models, perhaps by investing in some of these new entrants themselves, or by creating their own fully digital banks, or by significantly boosting their digital banking offerings. This means adopting a challenger-like strategy to compete across the board, to be rapid and nimble in approach and activity, and to be continuously innovative. Lethargy and inaction are extremely dangerous.

Another panel member noted that progress on the new licenses and operations had been delayed in Singapore due to the pandemic, Singapore having started the process later there. In Hong Kong, he noted, of the eight licenses granted, there had been more progress, but some were performing far better than others, with two of the Neo banks in operation by the end of 2020 accounting for a reported roughly 70% of the business generated to that date in Hong Kong. “That in itself suggests there are plenty of challenges with achieving the credibility you need as a digital bank to be able to bring in many clients,” he observed. But at least there is activity and progress.

Client acquisition – a major challenge

He added that client acquisition costs are perhaps the biggest hurdle to overcome, and to rapidly spread the message, it is tougher when there are seven other new arrivals all competing at the same time for similar types of customers. “I actually don’t see many successes around the region,” he reported.

Competition is constant, another guest observed, reporting that their approach is that the best way to fight disruption is to pre-empt it and to disrupt themselves. “We have been on the journey towards digital transformation since 2011,” they explained, “transforming from back to front, working out how we optimise our internal processes so that we can offer clients an almost real-time straight-through-processing experience wherever possible.” They added that the bank today has transformed so dramatically that there are today twice as many engineers as bankers, a true testimony to the dramatic shifts taken in recent years.

Expert Opinion - Damian Hitchen, Chief Executive Officer, Singapore, Swissquote: “A key point for the new Challenger and Neo banks, in addition to the common goal of client acquisition, is to be precise and focused on revenue generation and monetisation of the services they bring to market. Thus far, the new players have been positive in areas such as client UX and innovative services, but even with large war chests of capital behind them, they need a clear roadmap to monetise and drive revenues as the runway will not last forever. Hence a clear focus to prioritise which services, to which client segments in respect of monetisation should be built into the business development roadmap from an early stage.”

Digital-first to gain and retain an advantage

In some markets around the region, and partly in anticipation of the arrival or growth of the challenger banks, the strategy has been to go digital-first, leveraging the best of what the bank has to give clients the best access digitally, as well as offline. They explained that this very conscious decision to go digital-first was the fastest and best way to achieve scale in populous countries such as India or Indonesia, where the populations and the growth had been so rapid that the people there had literally skipped the PC/desktop generation and gone fully digital and mobile-first. They reported this had been a successful strategy thus far, and they continue to build out the digital products and the proposition in both India and Indonesia, including, for example, now providing unsecured lending in these markets, adding new investments online, and all done in a manner that is easily accessible to all.

As to the business model, they explained that it is essential to get it right in terms of costs of client acquisition and to then drive that necessary continuous engagement with clients, and bearing in mind that competing on charges and fees is not scalable and therefore not a realistic approach in the future.

Time required, but returns must follow

“As my fellow panellists have mentioned, it does take time, so we need to give the challenger banks that time to build their strategy, build their infrastructure, and deliver to market,” another expert commented. “But they also need to become revenue-generating and profit-generating before too long. They are pumping a lot of money into client acquisition, and then first provide services such as transfers, or payments that have very thin margins, actually which are probably loss leading at this point, in order to help create a large client base.”

The question he pondered is at what point do the Neo banks then actually try to monetise the new clients because, at some time, they must do that. “I would not consider them successful if they can move from the start-up and setup phase into the monetisation and profit-making phases,” he stated. “To do so, they need to be highly strategic and laser-focused in terms of which products that they're going to try and accelerate. For fee income, this could be brokerage from global markets, brokerage from cryptos, meanwhile lending is fundamentally a better long-term revenue stream to have, but lending, particularly in new markets, and particularly with capital requirements, is quite difficult, not that easy for a new player.”

Expert Opinion - Karsten Kemna, Managing Director, Asia Pacific, CREALOGIX: “About two-thirds of banking customers in Asia-Pacific are likely to use digital banking services offered by Neo banks and Challenger banks by 2025. Incumbents who have successfully adopted a challenger-like strategy will need to compete with the new challengers by increasing the rate and quality of innovation. Being a fast follower is not enough to make you a digital leader.”

Customer experience and client servicing

Another expert said that much of the future success comes down to the customer experience, at the end of the day, and high-quality client servicing. “We must consider how we continue to maintain those high level of service standards to give clients a hyper-personalised experience; that is a core issue,” they explained. “Secondly, we want to really reap the benefits of the full suite of offerings through the breadth and the depth of our bank’s proposition, and that is certainly something that challenger banks won't really be able to achieve overnight. Then we work on tying all this seamlessly together to really give clients that great feeling that we have exactly what they are looking for. Then, thirdly, it is about great accessibility through omnichannel.”

Proving their staying power

To achieve their goals, another guest said the challenger banks need to prove their longevity and really build trust and confidence. “For those with a serious bank or major corporation branding behind them, this will be easier,” he said. “Secondly, it is all about the customer experience and how you make sure that you are unique, that you provide the seamless experience.”

Expert Opinion - Karsten Kemna, Managing Director, Asia Pacific, CREALOGIX: “The competitive threat is not just about how to add new features, and how good they are for customers. It is about speed. If banks are in denial, it will be too late to wake up and compete at the stage when challengers are at parity.”

Future focus – a shift to wealth management?

“From my perspective, the key question for everybody in Asia who has been and is currently opening their digital bank or their Neo bank is how to really make money,” came another view. “I guess it is only a matter of time until the more transactional retail banking experience needs to lead into a wealth management experience also for these challenger banks. It has not happened yet out here, but I would assume for the new players, for example in Singapore and Hong Kong, or Malaysia coming up, this has to be fairly soon in the future landscape.”

“If the challenger banks move more into wealth from a more transactional retail banking experience, I think they really need to be fast,” an expert commented. “And for the incumbents that also means they need to be fast. I don't think there's much room for failure. I don't think you can hesitate in terms of is this not the right decision or not? But I think you need to be very quick in decision-making, and having the right digital strategy would certainly help with that. And that will also allow you to be perceived as innovative, and that will allow you to have a good market reception.

But how do challenger banks really get their lion's share of AUM of customers willing to go in this direction? “I feel at the moment,” he observed, “it's really more like a trial and error kind of thing, but in the longer term, I'm sure this would be a major problem if the challenger banks are established, that the outflow of AUM from the traditional banks will really also cause them some issues on the balance sheets. So, I think the incumbents really have to find the right strategies there to avoid that or counteract that already early to be able to grow with the flow instead of to suffer from it in the long run.”

Another expert reported that to fend off competition from the challenger banks and robo-advisories, and to pre-empt the Neo banks challenging the robo-advisories, they had developed their own hybrid approach to digital delivery of advice and portfolio creation, in partnership with a leading robo-advisor FinTech, creating managed services digitally, delivering an automated process for portfolio rebalancing, and for execution. The investment team still guides the portfolio allocation of the baskets of investments created and offered, but delivery and ongoing activity is mostly digitised. The human and the digital therefore combine to create a hybrid offering that elevates the proposition beyond the purely robo approach.

They also explained that the bank approaches digital as a channel for self-directed execution to monitor market movements and activity, but that from a wealth management perspective, advice is unique in that it is tailored and must be of the highest quality.

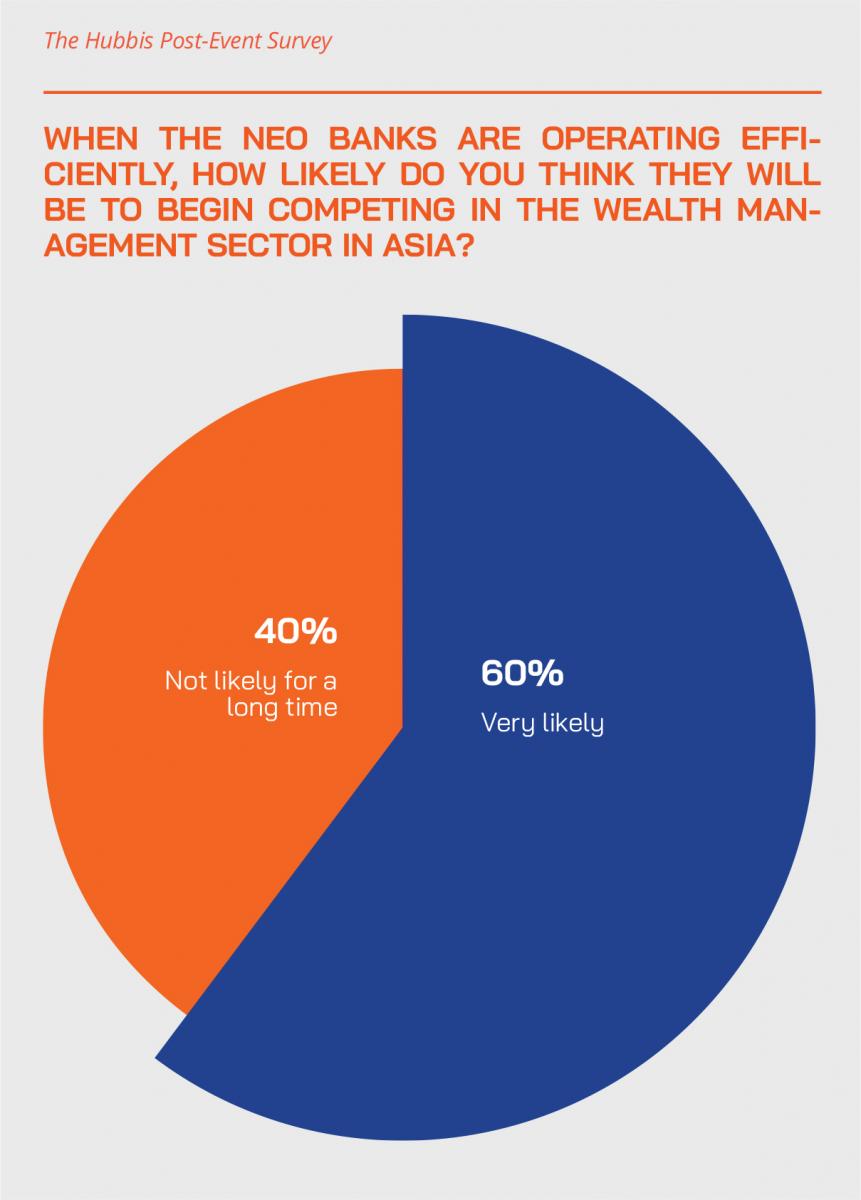

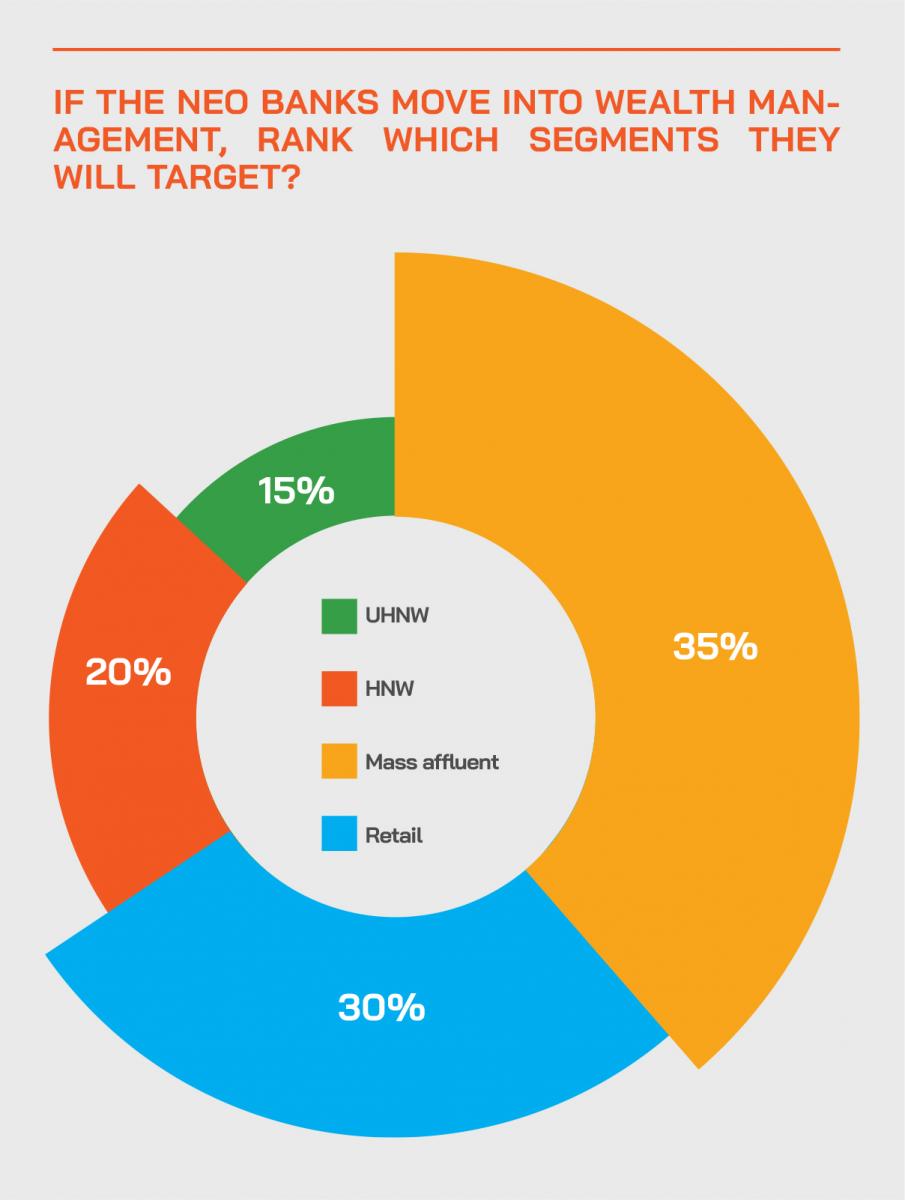

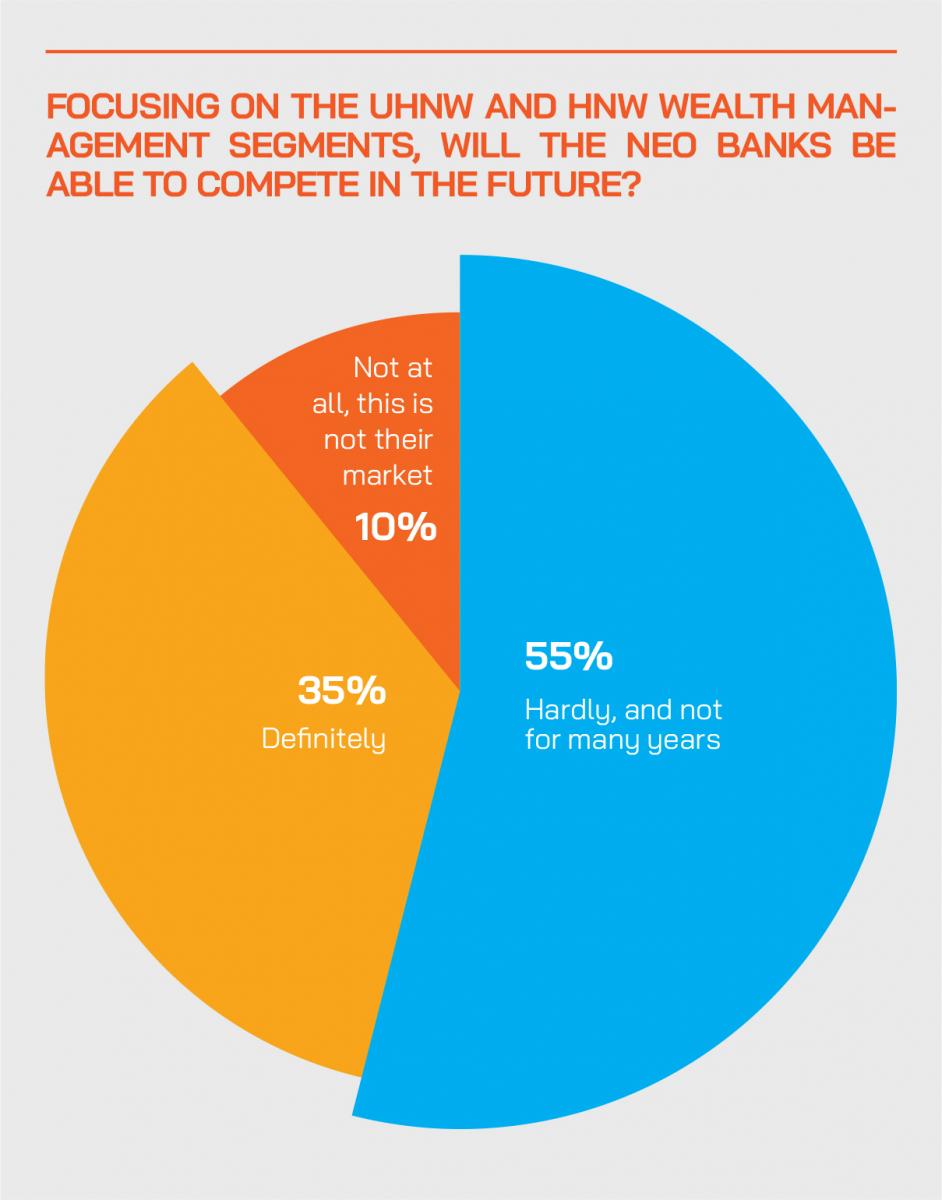

The Hubbis Post-Event Survey

Hubbis: Do you think the rise of the Neo banks in Asia will, later on, mean direct new challenges for the region’s existing wealth management industry? Very briefly, why or why not?

- Yes, the availability of the latest technology from the digital platform.

- Yes, for those services they are able to provide, and their cost base will be much lower than that of traditional FIs.

- No, I believe that eventually Neo bank [wealth] services in Asia will be developed by existing wealth management institutions, and it will be more like additional services within their broad spectrum of services.

- Neo banks in Asia will potentially post new challenges for the region's existing wealth management industry but the impact will be lower in the UHNW and HNW space as these people still prefer the personal touch and customer services and personal advisory. That [UHNW and HNW] space comprises of people who are still not tech-savvy, and they are happy to pay the fee for the services and the personal advisory where they believe these professionals are in a better position to provide quality advise through intensive research and market experience.

- Yes, somewhat. The younger generations will try out new services.

- They may find a more receptive view amongst the younger generation but not the old-school clients.

- No. Each has its own market segment.

- Yes, Neo banks have the ability to leverage a single network with the complete financial portfolio; this is more comfortable for the customers, as just one click then can open the door to what they need at just one stop, and at one time.

- Yes, but much depends on regulatory requirements.

- The rise of Neo banks will definitely help further mature WM industry, plug the loopholes and bring about more transparent and faster execution of trades.

- No, because [in the upper wealth segments particularly], the person to person relationship management process will still be key.

- Neo banks will certainly challenge the existing wealth management industry as clients are more tech savvy than before. This is the trend.

- Yes, definitely, especially for younger generations who are more accepting of new ways of investing.

- Yes. Asia is expected to see aggressive growth from neo banks over the coming years. Banking competition is predicted to intensify as regulators in the region accept applications for digital bank frameworks.

Hubbis: In which segments of the Asian wealth market might the new ranks of neo banks be most competitive, and very briefly why?

- The retail segment.

- DPM, funds, equity, bond and FX advisory, standard services where you can pool interests.

- Retail where they do not get or expect personalised service from the banks, as well as mass-affluent clients as these are younger generations who are tech savvy and prefer to deal online than the traditional ways.

- Equity trading for execution only, which requires limited attention from asset managers.

- Access to lower cost investment products.

- Affluent and HNW will shift towards these offerings.

- Only in the lower wealth segments where clients are seeking simple transaction processing for smaller transactions.

- For clients with AUM under USD 5million, because those clients are mostly self-directed and tech-savvy. Most incumbent wealth managers are paying less attention to these group of clients.

- The HNW segment and the younger generations, due to lower costs, more convenience, and the rise of mobile banking.

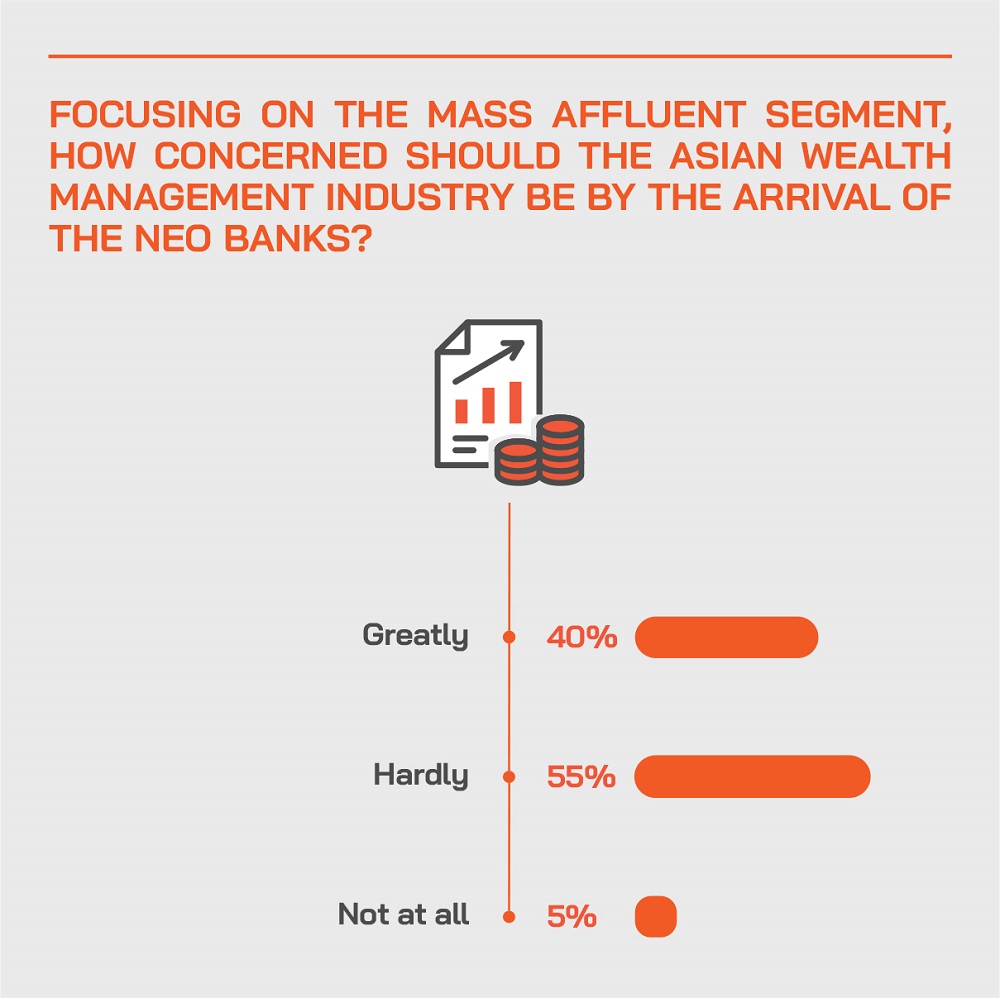

- The mass affluent segment, in order to achieve scale.

- UHNW clients are more dependent on and trust the RMs; they prefer to hear from RMs personally for their advice. They will not give up the convenience of getting RMs to help them with investments with just a phone call.

- There is a fundamental shift in the way retirement funds are managed as the investment opportunities in funds and other vehicles are more limited, so this is a means of achieving both security and investment at the same time.

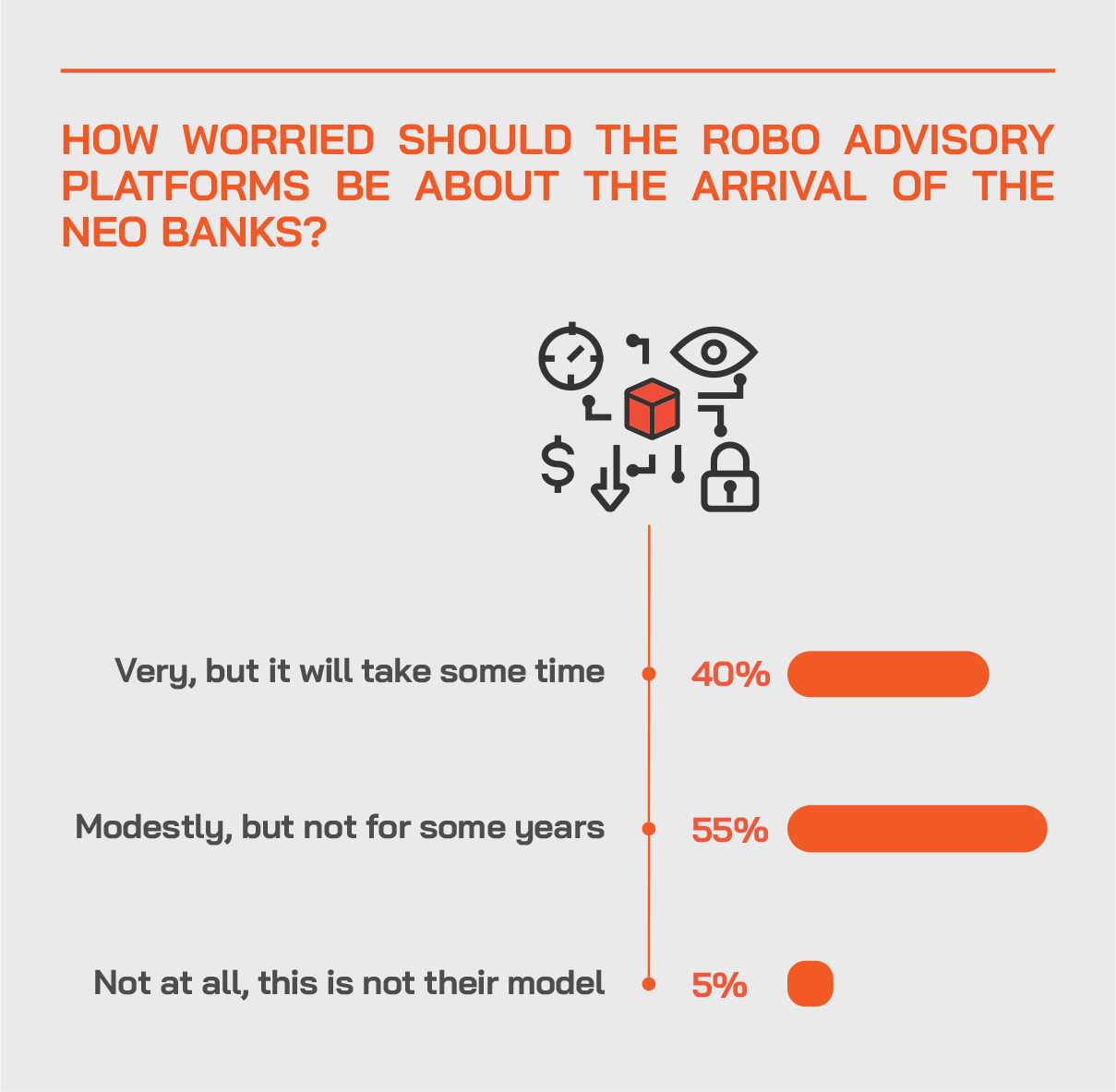

Hubbis: Do you think the Neo banks will soon/later aim to compete head-to-head with the new array of robo-advisory start-ups beginning to build AUM across Asia and for which market segments?

- Retail only.

- If they are able to incorporate algorithms and processes similar to those of the robo-advisors, then probably yes.

- Yes, differentiation, customer experience and marketing will be keys, I believe, for the mass market.

- Neo banks are gaining traction with their low-cost bases to penetrate and build market share. Most likely to succeed with the mass affluent and retail sectors and with the second and third generation of HNW where they are more tech-savvy and prefer to deal electronically than through the traditional banking avenues and processes.

- It will be very much later. HNW clients still prefer to speak to a person.

- Yes, as the Neo banks expand their service proposition to clients, including investment and portfolio creation and management advisory services.

- Yes, but it takes time to educate all the customers to use digital banking.

Hubbis: How effectively can the incumbent banks in Asia fight back with their own digital banking offerings?

- I think they can compete very effectively by developing or integrating their own digital offerings as they likely have the resources to do so or are on track to doing so. It is also a question of data gathering that they can use to enhance productivity and efficiency.

- Banks are building up their fightback against these digital in their own way via enhanced customer experience and investing heavily in this area. Transparent, non-intrusive fraud monitoring and detection can actually enhance the service and allow banks to do more for their customers, provide more options for money transfers, provide higher security to combat any online fraud and differentiate itself from the online platform.

- They will develop their digital bank services/offerings.

- They cannot really fight, they just have to adjust and adapt.

- They will collaborate increasingly with Neo banks to keep their market positions.

- Very effectively.

- More innovation.

- Through business partnerships with FinTech organisations which offer white label services.

- It really depends on the visions of the leaders; I think most of them nowadays are very short-sighted.

- Enhance product offerings, improve cost-efficiencies to offer competitive pricing to clients.

- It really depends on how much they are prepared to invest to maintain their current leadership.

Why bother with a Neo bank?

“As I see it,” said one expert, “a mass market digital bank is not something that I personally would want to put my money into. I think giving better, more interesting, more dynamic, more diverse portfolios for clients is something where I personally would be interested.”

He added that his platform had developed a managed account portfolio solution in partnership with a Singaporean firm, allowing clients to invest in quality funds and portfolios, with the managed account created in their own name with legal title to those assets, and with the portfolio performance assessed.

“This is effectively a sub-account under their own personal account; it's not a separate account,” he explained, “and accordingly it becomes an omnichannel experience for them. This is an area we will continue to develop. We will offer more options there ahead, including more dynamic portfolios, perhaps with more regular rebalancing, and more interesting assets; for instance, we have a huge interest in cryptocurrencies from our client base, while many of the banks remain reticent to offer those to their retail clients, whereas we think it's a part of the portfolio of the future, and it's a technology of the future, and well worth developing an understanding of the market and the technologies.”

Advice – the assembly and delivery

Turning back to the issue of the generation and delivery of relevant and high-quality advice, a guest observed that as clients have different risk and expectation profiles, it is not that hard to create different personas, different risk profiles, and address the different needs for those clients, thereby to categorise them into different groups and then to tailor the investment profile around those different groups. “As each client is unique, they must be handled in a unique way,” he observed, “but the danger is that the banks or other firms give too much power to financial advisors who do not have the skill set to make those kinds of decisions.”

As to the necessity of an RM, an expert said this was really down to the qualities of the individuals available. “I agree that the higher you go in the AUM chain, and the more it gets towards the UHNW segment, the more probably you need a more personal relationship also. Whereas at the mass affluent or affluent level of environment, what can a relationship manager provide them in terms of real value that they cannot do themselves?” he pondered. “Or is it actually that you are wasting time by talking to the person because you anyway know already, more or less exactly what you want to do, and you just need to execute it or transact it.”

Are the RM’s days therefore numbered?

A panellist reported that from his viewpoint, there remains a large subset of clients where the RM is still valid and still necessary. “There are clients who do not have the confidence to necessarily make a choice themselves,” he observed, “and there are clients who don't have the time to make these choices themselves, to conduct the necessary research, so there are many reasons why someone may want to have an RM or financial advisor to help them along the way. However, as time moves on, the younger generations feel more confident about their views on financial markets, which is why there is more of a move towards direct trading and self-directed investment, and we have seen a huge pickup in that in the first quarter of this year.”

On balance, he concluded that the number of clients who want to have a human advisor is shifting in the direction of digital, but there is far to go. “The older and wealthier people in general still like to have a personal advisor,” he said.

Digital wealth managers

“I think that there have been some more successful independent digital wealth managers so far as we see it, and some failures so far,” he reported. “We have seen massive growth in the AUM that they are acquiring in 2020, which has continued into 2021, so we see this as a challenge for the digital banks who are coming in when there are some strong and established players already in that space.”

“I think even in the independent financial advisor space, a lot of the guidelines come from the CIO office team,” he said. “They do have the skillset, but not the numbers to cover all the different clients.” Accordingly, he said that the banks need some sort of policy approach where they decide what sort of portfolios are going to fit different sorts of clients, different risk profiles, different time horizons.

And as to robo-advisors, he said that most of them do have individuals who are defining how the portfolio is constructed, and the robotic part of it is really about whereabouts on the risk spectrum within that portfolio each client may sit.

B2C? B2B? B2B2C?

A digital investments platform head explained that their business in Singapore had been focusing on B2C, which had already become a very substantial part of the operation. “We've made a large investment in marketing in Singapore really since 2018 when we launched our B2C investor platform,” he reported. “And the new managed account portfolios we now offer are very much targeted B2C, so that has been a huge growth area for us in the Singapore market and in other markets over the last few years. We see it as being a strong growth area for us as well going forward, as we move more from self-directed traders into a broader universe of digital advice, and digital wealth clients as well.”

Another platform head explained they had taken a conscious decision to cater for execution-only or self-directed customers, which could be B2C or B2B such as institutional client partners. “But we've also both invested an awful lot of time and money into our B2B2C proposition,” he reported. “What we have done over the past decade or so and continue to do is we then look at our client segments, be that B2C, B2B or B2B2C, and we roll them out on different platforms. And each of those platforms has different functionalities for those different client segments.”

He elaborated on this, reporting that this means a platform for professionals, for institutional clients to do API trading, group orders, asset management, to run their own model portfolios, and so forth. And there is also the standard e-trading platform for B2C clients, including a new application in Switzerland and Europe specifically for millennials and also entry-level investors, and limited to a universe of some 150 investment products.

“In this way, we have a very wide architectural investment universe, and then we're effectively distributing those to the different client segments via different platforms and different applications,” he commented. And extrapolating to the challenger banks, he observed that their model might also be gradually building their technology stack and infrastructure and moving forward step by step.

He also explained that in Asia, the platform had not moved to B2C yet. “We decided when we came to Singapore to be B2B2C, so as to effectively provide our platforms and our tools to our institutional partners, and then they provide the advice and money to their end clients, investments and portfolios,” he reported. “In Singapore, there are a number of very good players for B2C in this marketplace and a number of banks and other who have strong brands and a lot of customer loyalty. Accordingly, to actually build a large B2C portfolio from scratch when you're not necessarily known in the region is going to cost an awful lot of money from a marketing perspective and client acquisition perspective. Accordingly, at least initially in terms of our journey in Asia, we knew we had already oven-ready partners who wanted to use our platforms in the institutional space and the B2B2C space. We might branch out in the future to B2C, but not yet.”

Tools for the independents

For the moment, the model is, therefore as a digital investment platform to provide the tools for IFAs and IAMs/EAMs/MFOs to service their clients, providing an end-to-end service of execution, custody and account structure around all that. The digital tools for this segment are continually being developed, for example, to give the advisors tools to gain digital consent from their client where consent is required, providing better apps for portfolio views for the clients, tools to help them trade part of their portfolio themselves. “All these developments that are commonplace increasingly in the US and European markets are becoming more commonplace over here in Asia,” an expert reported.

Driving insights

Another guest returned to the subject of advice, explaining that this is what clients of all types come to their institution for. “That real quality of relevant advice needs to be complementary to digital,” they reported. “So, for us, the question is to how to provide this type of tailored advice at scale to the clients, either direct digitally or through our relationship managers. In wealth management, for clients to simply look at a list of funds, it is tough to make the right choices.”

Accordingly, they explained, the bank had started to look into giving clients more insights. “There are two parts to that, firstly what is our CIO saying, what ideas do we have, and also how we can then distribute some of these ideas to the clients in a digital manner that is highly accessible and easy for them to discover. Secondly, and this is from a discovery perspective, we are looking at how we start curating some of these products in a manner that can help those customers make a decision. Honestly, at the bank, I don't think we've nailed that yet, but it is an area that we are continuously fine-tuning.”

Pushing the boundaries

They added that for the moment, for their upper private wealth clients, the bank has introduced such insights, and it had started to curate funds for clients, coming up with thematic ideas and products. “All of these are aiming to really help someone shortlist what they should look at, based on preference and objectives,” they added, “and we are working further on this, really looking at pushing the boundaries to truly make investing into a theme.”

The same expert also reported that continuous innovation is essential and that they were now driving energetically towards delivering cognitive banking. “This is really leveraging the data that we have, the data insights that we have, to more actively and accurately nudge customers. We have begun this last year, driving this intelligent banking initiative. It is about leveraging data insights, the customer behaviour that we know of, and then gently nudging, keeping them informed, aware, giving them alerts, and thereby make their banking and investing easier. This is a core mission on which we are doubling up right now.”

Driving the customer experience

Another core mission comes back to the customer experience, really looking at the end-to-end portfolio management down to investments. “I can’t share more detail on this effort, but we are putting a lot of emphasis on customer feedback, working out where we get the five-star ratings, and what we need to do to improve the customer experience because I fundamentally believe that is really the essential element for a digital platform to be successful. It actually doesn't matter how many products you have online, how many different types of investments you have online. At the end of the day, it all boils down to the experience.”

Trust and innovation aligned

The final word went to a guest who said that for a major incumbent bank to compete in the future, it is essential to align both trust and innovation. It is not only about being ‘cool’, they concluded; it is also to reinforce the message that working through a major institution, the clients are totally safe and that the institution is totally trustworthy. In this way, the bank continually reinforces its core values and offers customers that degree of solidity they know is vital for any important financial services institution.