Publications & Thought Leadership

HNW Life Insurance – Riding a Wave of Demand with a Diversified Product Range

Jun 10, 2021

HNW Life Insurance Solutions have moved increasingly centre stage in Asia’s dynamic, expansive wealth market for many years and have made a significant contribution to the revenue for many private wealth managers across the region. But has the pandemic slowed the market due to the difficulty of remote paperwork, medical certificates and other impediments? Or has the industry risen to the digital and logistical challenges and met the additional demand for security and family protection with state-of-the-art solutions? In our Digital Dialogue discussion on Thursday, June 3, we explored the state of the life solutions industry today, reviewing the latest trends in products, identifying the optimal solutions for individual needs, and analysing where demand is on the rise from different segments of clients in the Asia region, and why. The industry is replete with a host of acronyms, from UL, to VUL, IUL, PPLI, and there is also Whole of Life, so in the current and interest rate environment, and given the outlook for financial markets and the economies, the panel of experts debated which are most suitable and offer the best balance of protection, investment returns and cost. They also looked at the major issue of funding policies and whether larger, more leveraged policies are advisable given the state of the financial markets and rates. They considered whether private banks and independent wealth management firms are doing the best they possibly can to help deliver insurance concepts and solutions in a compliant manner, working with the specialist agents and distributors in the market. And the experts discussed how life solutions are playing an increasingly central role in estate planning and facilitating the smooth transition of wealth from policyholders to their chosen beneficiaries, something that is especially important in a world of intense and proliferating regulation and compliance.

Panel Members

- Lee Woon Shiu, Managing Director & Regional Head of Wealth Planning Family Office & Insurance Solutions, DBS Private Banking

- Rohit Ganguli, Head of Wealth Planning Asia, EFG Bank

- Gaya Vythes, Chief Commercial Officer, IPG Howden

- Lee Sleight, Head of Business Development, Asia, Lombard International Assurance

- Mark Smallwood, CEO, Rapier Consulting

- David Varley, Chief High Net Worth Officer, Hong Kong, Sun Life Financial

The discussion opened with a guest citing a research report from EY that found that even before Covid-19 arrived, as many as 75% of APAC HNWIs were using or planning to use life insurance for succession and legacy planning. He said the pandemic had further accelerated this trend, especially as more people see more friends and acquaintances or family members hit by the virus. The result being that the bank had been closing more such life solutions deals and some of the megadeals.

Insurance solutions within wealth and estate planning

“Discussions around succession planning and estate planning strategies in general, and reviewing the existing structures, those had started maybe five to six years ago with the onset of CRS, consolidation of existing structures, awareness of tax issues, and the arrival of economic substance and other regulations,” added another expert. “Issues of mortality have further accelerated these discussions, so there are many more opportunities. However, there are challenges, as we know, especially travel and meetings. And when it comes to succession and other planning, issues such as those and governance, these are best handled in person, and there are limits to Zoom and other calls.”

Another expert agreed that there had been a big change in mindset in clients resulting from the pandemic, but also a big change in mindset of governments as well which have been funding massive deficits to help save businesses, jobs and economic momentum through the crisis.

“Insurance fits as a high death benefit risk mitigation tool for the family,” he commented. “Risks are higher today. And for RMs, this is really a vital topic to be discussing with clients. Insurance is also a tax mitigation tool in many countries, and clearly with the deficits that are being run as it is, there are many clients who now focus more on tax, and indeed the possible tax hikes ahead. For RMs, they should be discussing all these threats and how these solutions can address risk mitigation for life and also tax mitigation.”

A banker on the panel agreed, adding that the internal conversations are no longer just about simply protecting risk of livelihood or life, but more also about how to use structures, and insurance solutions to address risk and tax issues in a sophisticated way, for example, by using more complex solutions, like PPLI and VUL, and so forth. He said that in Singapore, with the growth of the family offices, there is a great opportunity for such discussions, and more lateral marketing across all stakeholders in the Singapore ecosystem, with momentum improving all the time.”

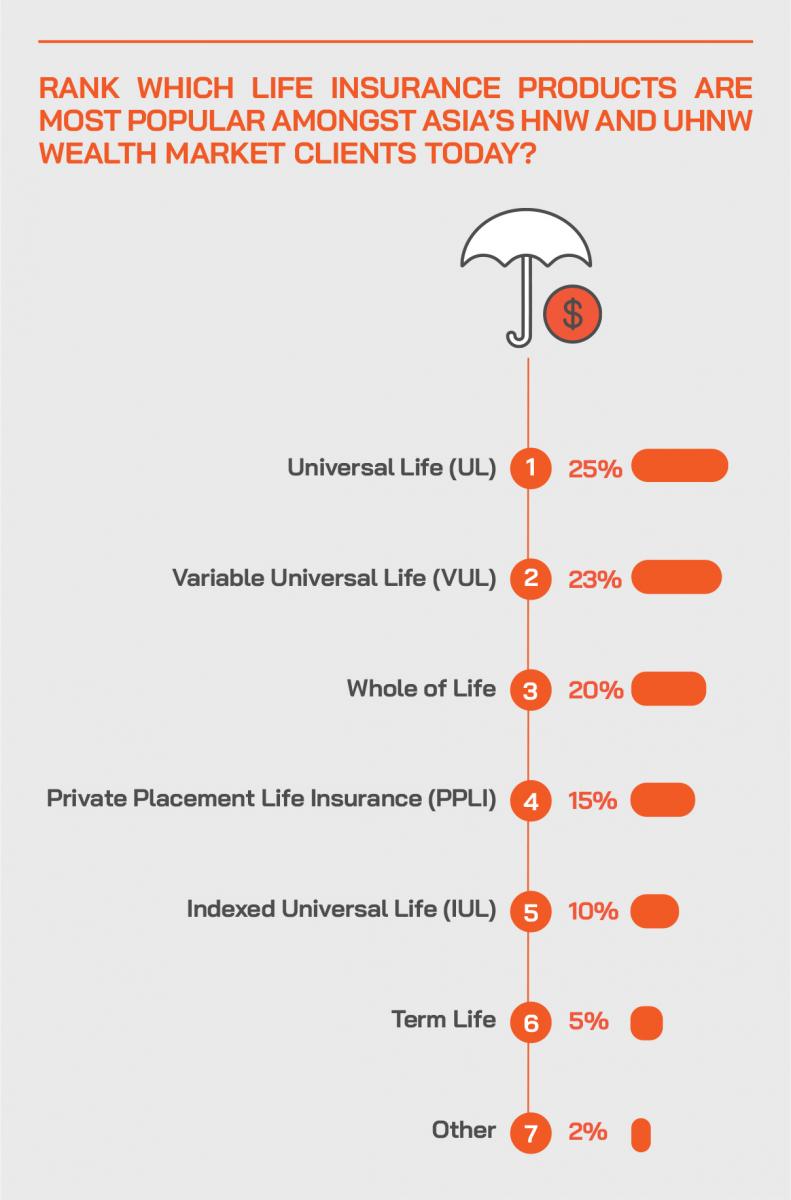

The evolution of the product suite

“From a broker’s point of view, we definitely have welcomed the product innovation,” an expert reported. “We saw UL dominate for a good 10-11 years, but clients are much savvier, so in Asia, there's definitely a bigger appetite for the guaranteed whole of life products. Leverage is definitely still key - rates are very low, there is great liquidity in the market and clients are looking for alternative asset classes, so that why we see the momentum in savings plans where clients as an alternative asset class, which can also be premium financed. We definitely welcome the opportunity to be able to advise the client based on their risk appetite, their objectives, whether this is through PPLI or VUL, or even a guaranteed whole of life.”

As to products and what solutions are in favour, a guest noted that five to six years ago, it was very much “There's more to this broadening market than universal life,” he commented. “UL was indeed such a big part of the HNW market. But in recent years in particular with crediting rates coming down, clients are concerned that perhaps a universal life policy is going to run out, so they have been swinging across to more guaranteed whole of life policies.

“They are paying their premiums, whether it's a single premium or a 5- or 10-year pay, and therefore the cover will last for life,” he reported. “And there is still a big premium finance market, especially in Asia, because interest rates are so low. We have also seen more savings plans with the private banks and the family offices, which can also be financed, and involved in wealth transfer and legacy planning. And PPLI and VUL are terrific structures, with certain brokers growing fast in those areas; VUL and PPLI remain a niche market, compared to jumbo Whole of life or the ULs or the savings plan but I do think in the coming years we will see more and more clients looking at PPLI and VUL as an opportunity for wealth planning and wealth structuring.”

Boutique and bespoke planning

Another guest highlighted the mobility of wealth these days and the complexity and global diversity of families and family members. “The need for boutique bespoke planning goes beyond the off the shelf, one size fits all, and what we're seeing is clients becoming more financially aware as they look to protect their wealth, pass it on to the next generations, so all this amounts to a big seismic shift. We see the need for more bespoke knowledge, not just from the client side, but also from the advisor’s side. We have certainly seen more PPLI and VUL, as people look to broaden their horizons and find the right solutions. The clients need bespoke solutions that specifically meet the needs of that client and the family.”

Another guest added a little more detail on the increasingly very popular savings plans, explaining these are insurance policies where a client puts either a lump sum or a regular pay with the insurance company and the insurance company commits to give back a certain amount, some guaranteed, some non-guaranteed.

“Some of these single pay policies have a guaranteed high day one cash value, and the clients can finance up to maybe 80% to 85% of that day one cash value, similar to a jumbo protection, UL or Whole of Life,” he reported. “When you are financing it, perhaps at 1.5% and the return is 4.5%, 5%, 6%, you're getting a very high IRR. Accordingly, savings plans have absolutely exploded in terms of being a key part of the high net worth journey in the past three to five years. Both regular savings and single pay savings plans are now a core part of the business for wealth transfer, for liquidity planning, and also for building up wealth and asset diversification in the HNW market.”

The Hubbis Post-Event Survey

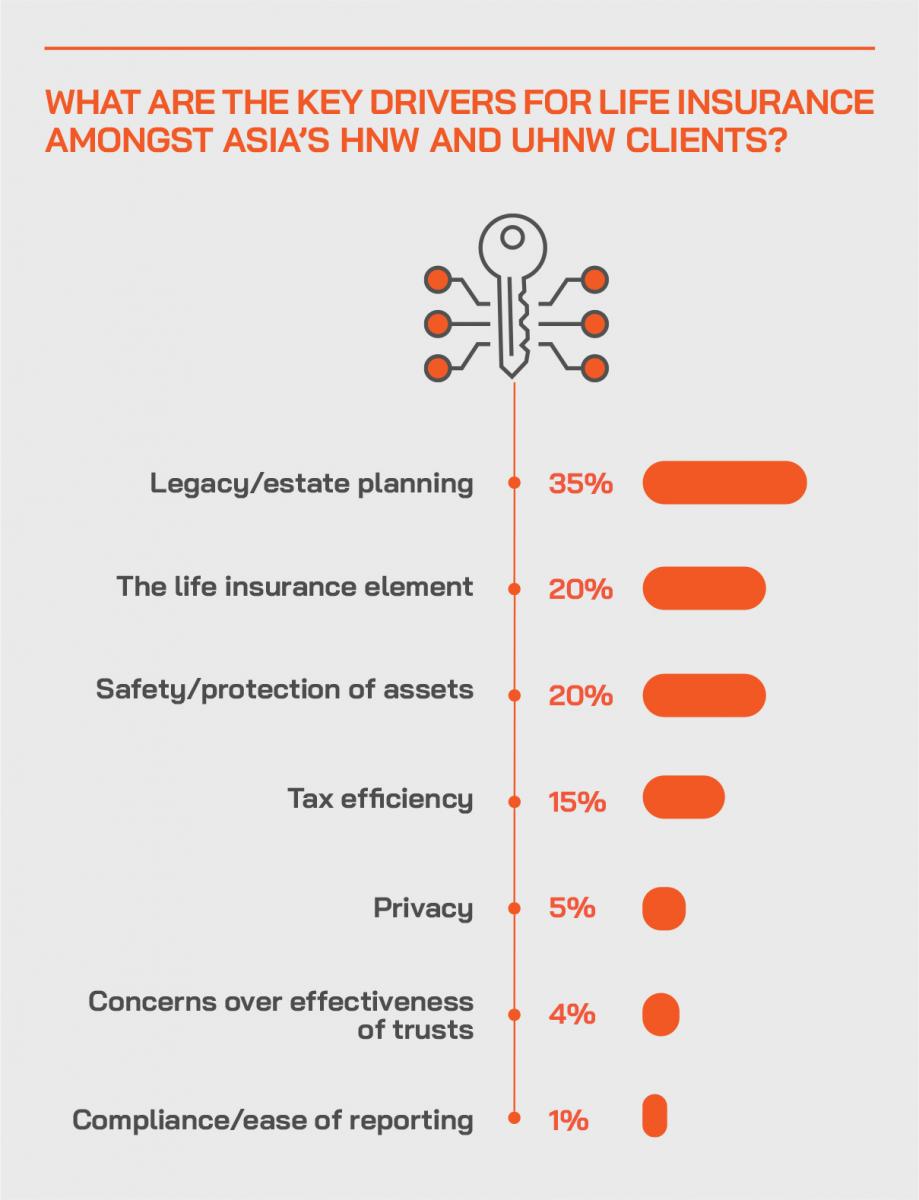

Hubbis: In your view, what are the main drivers for life insurance solutions for Asia’s HNW and UHNW clients?

- Wealth planning, estate planning and wealth succession. Using life insurance as collateral for investment purposes.

- Succession planning.

- Estate and succession planning.

- For death coverage benefits and deferment of taxes.

- Wealth planning and protection.

- HNW investors today are complex and have multiple assets in various global locations and accordingly it is imperative to protect them today and for future generations from tax, creditors or unfriendly governments. The pandemic has made clients more aware of their own mortality and the resulting volatility in the markets has resulted in clients needing more security when succession and legacy planning. Inevitable increases in taxes across the board compound their fears. The bespoke insurance products in my opinion, offer the flexibility now needed and are the ideal solution for these HNW clients.

- Nowadays, HNW and UHNW clients are looking for a tailor-made solution, plus the credibility of the insurance company. In respect of the geography and mobility of the people (including their family), optimal tax solution will be their key concern.

- Need to plan for future generations and wealth transfer.

- Charitable giving (particularly for the very wealthy).

- Inheritance tax and succession planning are the main reasons in my view. Also, there is instant liquidity for family members who may not want to sell real estate, shares or other less liquid or illiquid assets. However, for the Brokers/Private Bankers/IFAs, the commission is the driver.

- Valuable for segregating personal assets from business wealth.

- Pre-migration tax planning.

- In my view, the main drivers for life insurance solutions are predominately due to clients' intentions to protect their income, better taxation planning/mitigation and to better plan for their liquidity.

- Primarily, the Covid 19 pandemic scenario which leads to health concerns. Likewise, HNWs and UHNWs are scouting for alternate asset classes that deliver both protection and significant returns.

- There is increasing need for succession planning and rising awareness and sophistication amongst advisors and end-clients.

- Ensuring appropriate levels of protection remains a key driver, but there is increasing focus on insurance solutions as part of a holistic long term wealth planning solution – generation planning, portability and tax clarity and efficiency.

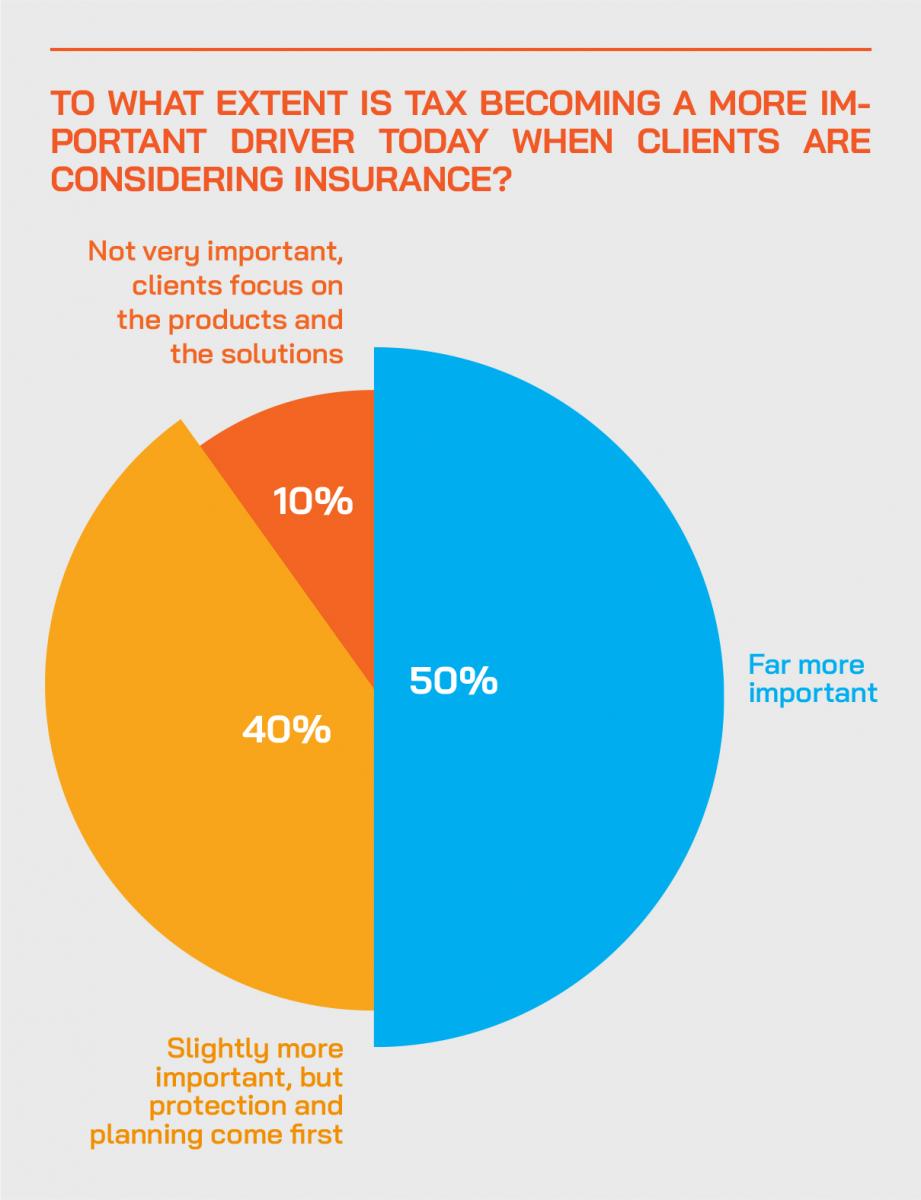

- Regarding tax considerations, the pandemic and regulations have further opened the door to a greater opportunity to reinforce the value of insurance solutions to these clients, and there is greater acceptance. For succession and trust planning, the awareness of life vulnerability post-pandemic drives HNW families to hedge these uncertainties via insurance solutions to protect their legacy from these external negative forces. Increasing awareness by HNW families on the benefits of liquidity and flexibility life insurance solutions offer in crisis. Regarding compliance and ease of reporting, life insurance can also provide dynamic solutions addressing liquidity needs for businesses, as well as key personnel protection for smooth succession planning.

Conceptual discussions and client engagement

Another banker observed that they drive many conceptual discussions around wealth and legacy planning and solutions, being careful to avoid direct tax or other specialist advice that regulations require them to steer clear of. “To have the conceptual discussion, and to have the awareness of the issues which should be considered by the client, and to increase your technical skills are all very important,” he reported, noting that the bank places great emphasis on training and skills to boost this type of dialogue, then referring clients to specialist brokers for insurance and to other experts as required.

A fellow guest agreed, noting that conversations with clients often take a number of ‘meetings’, as it is complex to mine down to the individual or the family needs and to fine turn ideas to particular people and situations and needs.

More carriers, more products

“The number of carriers as well as the number of product variations available on the market has definitely grown to a larger extent, which is why we have our own in-house marketing and products team who will do their own due diligence on the type of solutions available, we will then decide amongst the committee whether this is the solution that we want to have on the platform to then subsequently distribute,” he reported.

“Not every product does make it through our due diligence process,” he explained. “Typical things such as the S&P ratings of the insurance companies play a major role, so that limits the carriers to some extent. And our counterparts, being the banks that we work with, and they also conduct their own due diligence on the insurance companies. All this means there are certain levels of risk mitigation involved before the carriers are onboarded, and then subsequently showcased to the clients.”

Offering a snapshot of the solutions available, an expert said that the conversations should be advanced by RMs and advisors, or other people will step in to do so. The brokers and insurers have the specific expertise to conclude these deals, but the wealth industry should be nurturing more conceptual discussions, whether about guaranteed whole of life, or IUL, PPLI or plain vanilla UL.

A guest highlighted that insurance should not be viewed as standalone. “We can be looking at trusts and other existing structures that clients may have, and how to enhance the planning that clients have today,” he advised. “The combination of insurance plus an existing structure can make that more future proof. So, rather than coming out and having a fresh conversation, you can help to enhance structuring by combining those with insurance. And you need to be confident that this will be fit for purpose in 5, 10 years’, 15 years’ time, so we need to think of improved flexibility.”

Expert Opinion - Lee Sleight, Head of Business Development, Asia, Lombard International Assurance: “The current environment has further heightened the focus on sustainability and has truly encouraged HNW and UHNW families to re-examine their succession plans, to reconsider the ‘purpose’ of their wealth and align their assets with their non-financial goals and aspirations. It is becoming more than just simply passing on wealth to the next generation. Individuals are asking questions such as “what is my wealth about?”, “what are my objectives?”, the fundamental idea being how to use this wealth constructively to make a change.”

Expert Opinion- Lee Woon Shiu, Managing Director & Regional Head of Wealth Planning Family Office & Insurance Solutions, DBS Private Banking: “In the midst of the Covid pandemic, the ability to act proactively listen and react to the needs of clients and distributors and decisively pivot in terms of service offering and delivery will differentiate the winners from the laggards in the HNW life insurance space.”

The Hubbis Post-Event Survey

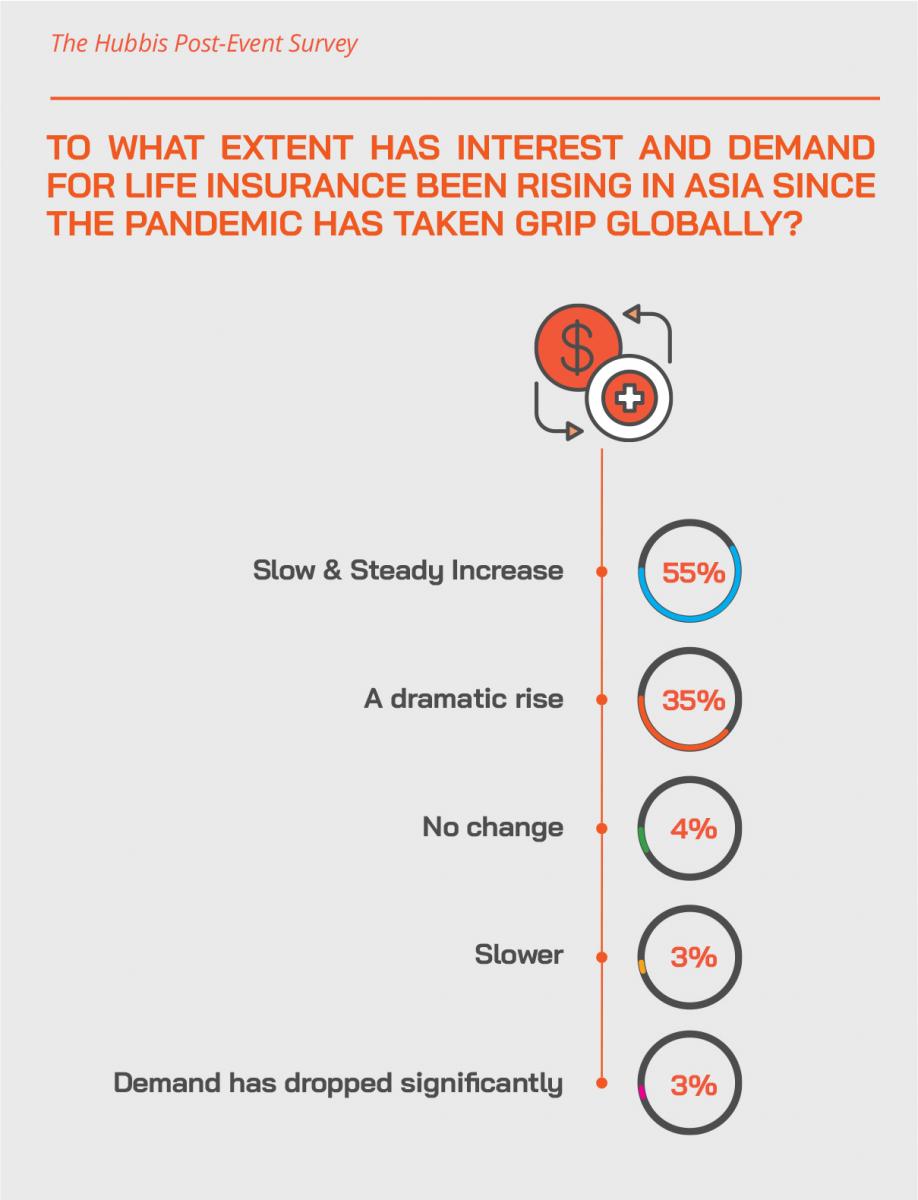

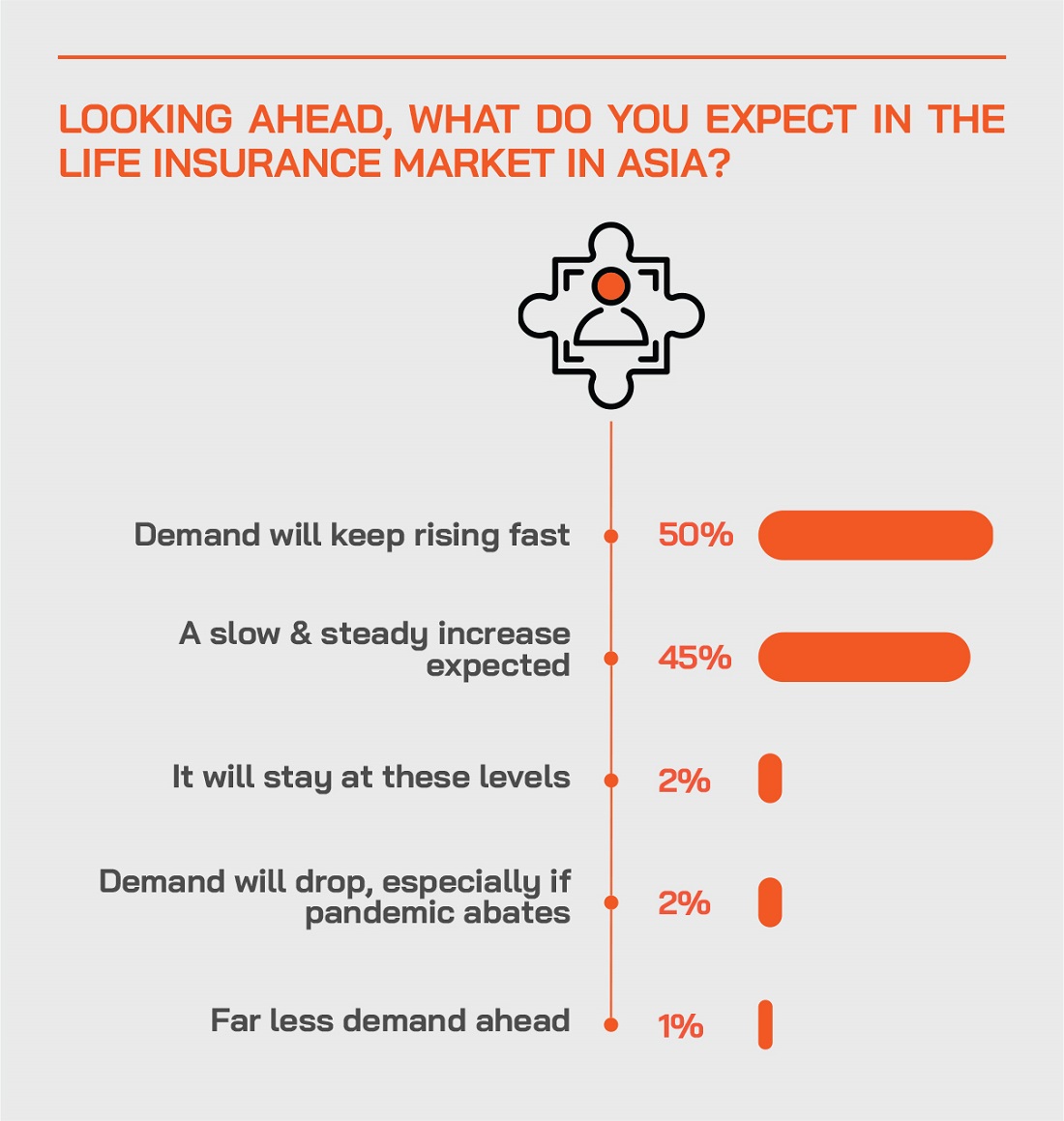

What impact has the pandemic had on demand for life insurance amongst your HNW and UHNW clients in Asia?

- It has highlighted and brought into sharper focus the importance of death coverage benefits for loved ones.

- It is not just people being more aware of their own mortality, but also the increase in market volatility and future increases in taxes that are driving clients towards a more secure investment and protection option.

- We had a record year last year and also so far this year.

- More clients are aware and interested, especially since the pandemic and the intimations of mortality, the knowledge that disaster might strike any time, from nowhere. Also, clients have a bit more time on their hands to consider these and other solutions.

- There is a greater inclination towards solutions as a pre-emptive step to preserve the wealth and to shelter the family from external and unforeseen changes.

- The pandemic has affected a small percentage of our clients. Demand is slow but definitely will increase sharply in the next couple of years, especially in countries badly affected by the pandemic.

- The pandemic has certainly led many clients Asia to realise the importance of succession planning and how to maintain the lifestyle of the subsequent generations in the event of the client's demise since so many HNW and UHNW clients in Asia are sole business owners.

- Increasing urgency resulting in rising demand.

- It has certainly narrowed the focus on what's important and what is less important and has made clients realise how quickly things can change and therefore the pressing need for proper insurance and proper legacy planning. It has been very much a call to action.

- The pandemic actually highlighted and accelerated the interest towards life insurance by clients pertaining to the overall protection of wealth. Current challenges we face are naturally the lack of face-to-face interactions and challenges on medical screening requirements.

- The pandemic has helped clients to realise the importance of organising their wealth and succession planning more efficiently, and it offers Private banks and Independent Asset Managers and RMs to address these subjects with UHNW and HNW individuals.

- There is increasing demand for protection life insurance solutions and higher urgency for UHNW and HNW individuals and families to look into insurance solutions to preserve the wealth and to protect the family from external threats. Research data shows more than 70% in agreement that insurance plays a significant role in creating and protecting wealth.

- As a Trustee we have found an increased demand for using our structures as policy owner in Hong Kong due to travel restrictions.

Thinking about jurisdictions

The issue of jurisdictions, whether Bermuda, Hong Kong or Singapore was addressed by an expert who said it is advantageous if you have HNW insurance companies that are based in all three jurisdictions to cover all the different client expectations. “Due to the capital and regulatory regime, different jurisdictions can do products differently better,” he elucidated. “Par Whole of Life, par savings, par jumbo savings attract clients from all over Asia and all over the world often come to Hong Kong. Bermuda was traditionally very strong for IUL or UL and now IUL is coming up in Singapore. PPLI and VUL are tough in Hong Kong now due to the regulatory issues, so you're seeing Singapore, Bermuda, Guernsey, Jersey, and Isle of Man doing more PPLI and VUL. And different markets also have different approaches to handling the pandemic restrictions.”

He added that the jurisdiction was also very important as well as the product, as some markets are better than others for specific solutions, and each has its own capital and regulatory requirements. “That's why you speak to insurance companies and brokers, in order to understand where the best solutions are from and what solution fits the client's needs the best.”

Expert Opinion- Lee Woon Shiu, Managing Director & Regional Head of Wealth Planning Family Office & Insurance Solutions, DBS Private Banking: “HNW Insurers who were willing to disrupt the status quo and move fast in leveraging technology to secure the first-mover advantage for the continuous protection of risks scored big in 2020, and will continue to win fans in 2021 among clients who value speed and certainty given the ongoing unpredictability.”

Expert Opinion - Lee Sleight, Head of Business Development, Asia, Lombard International Assurance: “On global connectivity, as wealthy individuals become more internationally mobile, global connectivity is key in our sector. They need relevant diversification and management of assets strategies that are fully compliant across multiple jurisdictions and benefit from security and accessibility. To navigate increasing complexities in an unpredictable global economy, HNW families need experienced technical specialists that understand local regulations and nuances of cultural references and priorities, in order to cater to their unique requirements.”

Insurance solutions and issues of residency and location

The issue of residency arose, with a guest pointing to tightening initiatives. For example, there are many, many wealthy Indians living in Dubai, claiming residency there, but with their businesses in India and spending most of their time in India. “The tax authorities can see this, and they're after these people, but there are solutions, as you say, with residency and citizenship planning. Non-resident Indians, or NRIs, are not allowed dual citizenship, so they would have to give up their citizenship and take up another, for example in places such as the Caribbean, or Malta, Cyprus, or other places with investment migration programme.”

He said that another example would be the many Asian clients exposed to the UK, and a lot of Asian clients who have a massive UK inheritance tax problem because they own real estate there, mostly in London. They can take a term insurance policy if their intention is to sell the property within a short period of time or take out a whole of life policy to mitigate the tax risk. “And for these and other reasons, you do really need to understand the client position, and really understand where those liabilities lie and where the priorities lie in mitigating them.”

Family offices – a rich source of dialogue and the 360-degree vision

An expert in dealing with family offices, many of which house huge wealth, pointed to the opportunity afforded to enter discussions on insurance encompassing a whole host of inter-related issues to cover the entire holistic needs of the family and not just at one particular asset class, or one particular individual.

“When you have a family office, it is very comprehensive in coverage, so issues such as succession, family governance, planning for liquidity, planning for the next generations, management succession, asset transfer, maintenance of ownership control, and also move on to engage the family members into issues such as insurance, planning using structuring,” he explained.

“These are all key topics which you can expand the understanding of the clients, so insurance can have a very pivotal role to play when you engage family offices, because the extent of the discussion is just so much broader, and so much more dynamic, and involves the future needs of future generations. And when you have a very, very clear understanding of how these needs will evolve and how they should evolve, bearing in mind your issues concerning residency, nationality, locality of the assets, this brings in a lot of options, to really then talk about different kinds of insurance policies and solutions.”

Expert Opinion - Lee Sleight, Head of Business Development, Asia, Lombard International Assurance: “As to the need for tailored wealth planning solutions, far from curbing this, the pandemic has only intensified the demand for bespoke wealth planning solutions. For many, it has been a catalyst, urging HNW and UHNW families to review long term estate and succession plans. Having passed the accumulation stage, the focus is now towards protecting and preserving the wealth and ensuring this can be passed on in an organised and controlled manner. Combining more traditional structures with the benefits of PPLI can be very powerful.”

Elevating the hard and soft skills of the RM and advisor community

He added that from the RM perspective and training the RMs to engage in more such conversations, they need to see the big picture of tax, and other crucial wealth planning issues such as matrimonial issues, bankruptcy, residency issues, all of which are critical. “So, before we tell the RMs, ‘let's train you better in how to sell insurance’, we first train them to understand the profiles of the clients they serve, we train them to understand the landscape of the countries in which these clients reside before we even move on to say, this is how you market insurance because we believe that understanding this background contextual information will help the client advisors better appreciate how to serve the needs of their clients, and better able to really see when a client will be keen to have a conversation about insurance.”

He added that the bank had spent significantly last year to get experts to prepare tax ‘cheat sheets’ for core markets, and then asked each of the advisors in all of these markets answer the same set of questions, addressing issues on trust planning, insurance planning, and find angles which their advisors can use from these answers in these cheat sheets to better engage with the end clients. “We found that now with CRS, many clients are now accepting the fact that we have to pay for good advice and they're willing to sit with an advisor, working with an ecosystem of stakeholders to comprehensively and collectively address all the issues of the clients from A to Z.”

The Hubbis Post-Event Survey

Amongst the private banks and independent wealth firms, which are doing the best or most at promoting life solutions amongst their clients, and briefly why?

- Most bankers really operate as asset managers, and like most active managers these days after fees and costs they often add little value, but they need to approach these issues holistically, really understanding the clients, their cashflows, their assets and liabilities, and what tools then from the insurance space in particular can be used to mitigate those liabilities. The pandemic has helped encourage this approach, but there is more to do. They need to work with wealth planners who are tax experts, even though they may not give tax advice, for example suggest liability matching solutions, which may involve, for example, PPLI, as a solution to some of those problems. The banks need to continue to invest into their wealth planning capabilities.

- Independent wealth firms, because of their more holistic approach toward promoting VUL and PPLI as estate and succession planning tools.

- Most of the international and local banks are good at promoting life solutions as clients are more open to using insurance as a tool for financial planning especially related to high taxation jurisdictions.

- Both - there is a trend moving toward holistic service offerings, and life solutions are part of the picture today.

- I think private banks could have a better capacity at promoting life solutions amongst their clients, as most private banks have better resources and knowledgeable tax experts, and they can thus they can provide the most suitable training to their RMs before approaching to the clients.

- Private banks with wealth planning departments where wealth planners are more aware and can focus on issues rather than where RMs are more product oriented.

- Our business mainly comes from independent wealth managers, however the HNW brokers in Asia take referrals from the private banks. We find a lot of the time the private bankers are dictating the products to the HNW brokers.

- Independent wealth firms as the products could also enable the wealth managers to invest for and on behalf of the clients towards a win-win for all. Client working with the IAMs are not limited to the bank's products only.

- Private banks as they can provide premium financing and a range of better solutions.

- Global banks as they offer life solutions as a part of the overall strategy.

- In terms of traditional HNW/UHNW insurance solutions, the PB channel remains strong although some evolution in the nature of the solutions with a move away from UL and they have wealth planners to help support the overall proposition, but independent channels better positioned to adapt to new solutions, deliver broader market view and deliver real customer value.

- Private banks will tend to perform best as they have a huge client base, the know-how and the infrastructure and huge capital investment at their disposal and good networking with insurance brokers.

- Independent wealth firms, as the private banks are still product pushing and chasing revenues.

- Independent wealth firms are doing the most at promoting life solutions as they are keen to provide a more holistic approach towards the needs of their clients.

- Independent wealth firms tend to be the most active and best in this arena, as they normally cover a wide range of services in addition to the wealth management as provided in the private banks, in particular the tax planning, succession planning, the legacy and estate planning and so forth, which are basically offered in a one-stop-shop package to clients by more of the IAMs.

- I think the private banks, with their dedicated resources and expertise, would be able to do more in this market segment. Having in-house trust services may make a difference too.

Working life insurance solutions into the broader suite of structures

A guest commented on the use of trusts with life insurance structures such as PPLI, remarking that bankers and clients need to assess the relevance of those in different jurisdictions. He advised that the combination of trusts with the right insurance solutions will allow many clients form many different jurisdictions to potentially have their cake and eat it.

“Combined with the trust becoming the policyholder of the insurance policy, putting assets that the trust holds today into the insurance policy, you get the benefits of the insurance policy while still maintaining that trust structure, which may give you the control,” he explained. “And you have the PPLI, the insurance policy potentially underneath owning those assets, which gives financial benefits to the trust that maybe the trust doesn't enjoy because the settlor, for example, is resident in Indonesia, resident in Taiwan, for example, which do not recognise trusts.”

Digital days and holistic perspectives

The panel briefly discussed the vital importance of digital solutions, e-documentation and digital connectivity in the new world today, not just for client engagement on sales but also for ongoing servicing, which is vital through the life of the solutions.

The final word went to a guest who spoke on behalf of the wealth management community to reiterate that there are many, many great opportunities ahead to promote life insurance solutions to the HNW and UHNW market in Asia.