Publications & Thought Leadership

Empowering the Relationship Manager & Delivering Wealth Management for Tomorrow’s World

Sep 15, 2021

The premise for our Digital Dialogue discussion of September 2 was that the relationship manager will continue to be central to the delivery of the enhanced capabilities and solutions in the Asian wealth management industry, particularly for the robust HNW and UHNW segments. Experts and leaders in the wealth industry believe this will be true, even in the world of remote working practices and diminished face-to-face communication. In short, the wealth industry is future-focusing and the RM community for direct or ‘virtual’ communication, empowering them with the right strategies and the optimal digital tools and solutions so that they can deliver the best versions of themselves and the banks and firms they represent. The September 2 discussion analysed how the RM’s day can become much more efficient and productive, how much of that day is essentially dedicated to non-productive administrative and compliance tasks, what tools and technologies the RM can be provided with to make them more efficient, more productive and most importantly more client-centric. The panel discussed the constant investment in technology and processes the banks and WM firms must adapt their approach and strategies to the mission to empower the RM, and how the RMs themselves must evolve in order to improve outcomes for their clients and to enhance their share of client wallet, as well as their professional satisfaction and career longevity. The discussion went a good long way towards painting a clear picture of how in the decade ahead, the RM can be enhanced and empowered to the betterment of themselves, their clients and the banks and firms they work for.

The Panel:

- Avishek Nandy, Partner, Bain & Company

- Urs Lichtenberger, Managing Director - Head Client & Front Office Platform, Asia Pacific, Credit Suisse Private Banking

- Neil Thomas, Head Sales Asia Pacific, SIX

- Alan Lim, Senior Director, Simon-Kucher & Partners

- Gabriel Chan, Head of Sales – APAC, Wealth Dynamix

We all know that the client has become far more front and centre of the world of private banking and wealth management, and the experts will debate how the wealth industry can align itself with the needs of those clients and the ongoing quest for client-centricity and the objective of boosting RM engagement, and of arriving at and retaining the trusted advisor status, which is so central to revenues and longevity. There are many ways in which the relationship manager can be re-invented in the decade ahead, and many steps are already being undertaken to achieve precisely that.

While Asia’s economic growth and private wealth creation has been truly remarkable for the past two decades, the wealth management market has in some respects lagged behind its counterparts, for example, in the far more mature markets of Europe. Boosting the capabilities of the RM is a crucial element in upgrading capabilities and productivity for the private banks and the independent wealth management sector, as they are fight increasingly tough and smart to retain and boost their share of the buoyant HNW and UHNW markets.

The constant journey to future wealth management

A senior banker opened the event by reminding the delegates that it was as far back as 2013 when their bank took the strategic decision to go omnichannel, but always with the RM absolutely an ongoing integral element of the wealth management and the private banking business.

“We have stayed true to that vision, and Covid-19 has without doubt accelerated technology adoption and has spurred a survival-of-the-fittest landscape,” he reported. “We keep innovating and have some newly introduced offerings from a digital perspective, such as our private bank chat app, which enables the RM to interact with their clients on their choice of social platforms, whether that is WhatsApp, Apple iMessage, WeChat or others that might be more specific to certain markets.”

He told delegates how the chat app had seen an enormous rise in adoption since the pandemic, rising to a high level of engagement that has continued and expanded today. “It facilitates interaction, instructions to the RMs and advisors, execution, delivery of documents and so forth, as it is an entirely secure delivery protocol,” he explained.

The multi-faceted approach to innovation and the hybrid model

A specialist in digitisation observed that banks are investing heavily in technology, looking at new models, thinking about omnichannel and the role that RMs will play in the future. “A key question for all of them is to simplify and focus on the things that matter rather than swinging to be really technology led,” he commented. “And then as you move into an omnichannel world, where you are asking clients to do a lot of the self-service digitally, what happens to things like KPIs and what how do RMs measure, and drive customer adoption? Finally, the banks must really boost the RMs’ digital capabilities, so upskilling is very important as well. Addressing all these key issues will help make these models work.”

The RM is here to stay, so leverage their capabilities

He added that the RM is here to say, just digital is not going to be moving the needle so much, human touch points really matter, definitely in the higher end, but even in the mass affluent space. “Research that we have done recently in some of the markets in Southeast Asia that clearly highlights that point,” he reported.

He also commented that RMs tend to concentrate on their most valuable clients – the 80/20 rule – but digital can help RMs to understand who these other clients are, with a focus on a tiered model that focuses on the individual characteristics of each client.

Another expert added that the RMs are being freed up to better understand more of a client needs, and then boost client engagement. “The RM should be effectively used to really advise customers on the proposition, on the products and relating them to their portfolios,” he said. “That is where they can add value.”

In an omnichannel world, consistency is essential

A panellist observed that in an omnichannel environment, consistency of perspective and message is vital. “We are going very much into a digital world, where we are able to generate personalised insights, and where there are multiple touchpoints in an omnichannel environment, but there needs to be a consistent approach and recommendation that comes from all these touch points including the RM, otherwise the client can get very confused. Consistency of message and recommendation and advice is essential.”

Additionally, he advised that pricing consistency and transparency are also essential, certainly from a business perspective in an omnichannel environment with multiple touchpoints, but also from the viewpoint of the ever watchful and increasingly vigilant regulators.

CLM and CRM – vital to drive relevance and productivity

Another expert focused on the role of client lifecycle management (CLM) and CRM, or customer relationship management for wealth management. “Omnichannel is not new, but right now the focus is on extending self-service to private banking, and while I do believe that relationship managers will continue to be central to wealth management in every bank and firm, their role is going to be radically different. To achieve that, data is the oil for the 21st century, but many banks are not able to unlock the value of this data due to their legacy systems. However, by harnessing technology and making a hybrid implementation, whether it's digital, self-service, and face to face engagement for an RM workbench, RMs can improve productivity, and creating a lot more client satisfaction and drive AUM growth.”

Turning data into insights

Another guest concurred with this big picture view on behaviour and the role of data, noting that their firm is an expert provider of financial information.

“It is essential for the RMs to have the right information for their interaction with clients,” he commented. “Our role as a data provider is to ensure that we have all of the right types of data, so if they want to trade, they can do it quickly, and have the right information. And then we need to take that data further, to look at the themes, for example ESG based strategies, or digital assets and the cryptocurrency space, where there is somewhat of a dearth of regulated exchanges. So, we need to support these areas by bringing our institutional reputation, particularly in trading and exchanges, to support RMs and so they can then support their customers. This is certainly all about empowering RMs, it is really a critical part of what we want to do long term.”

He offered further insights, noting that there is no shortage of data, but the trick is to take that data in its raw form to create analytics and therefore insights. “We need to take data to the next level, merging it with non-traditional financial information and alternative data, so that when an RM is having that interaction with clients, they have the full picture. We call this turning data into insights.”

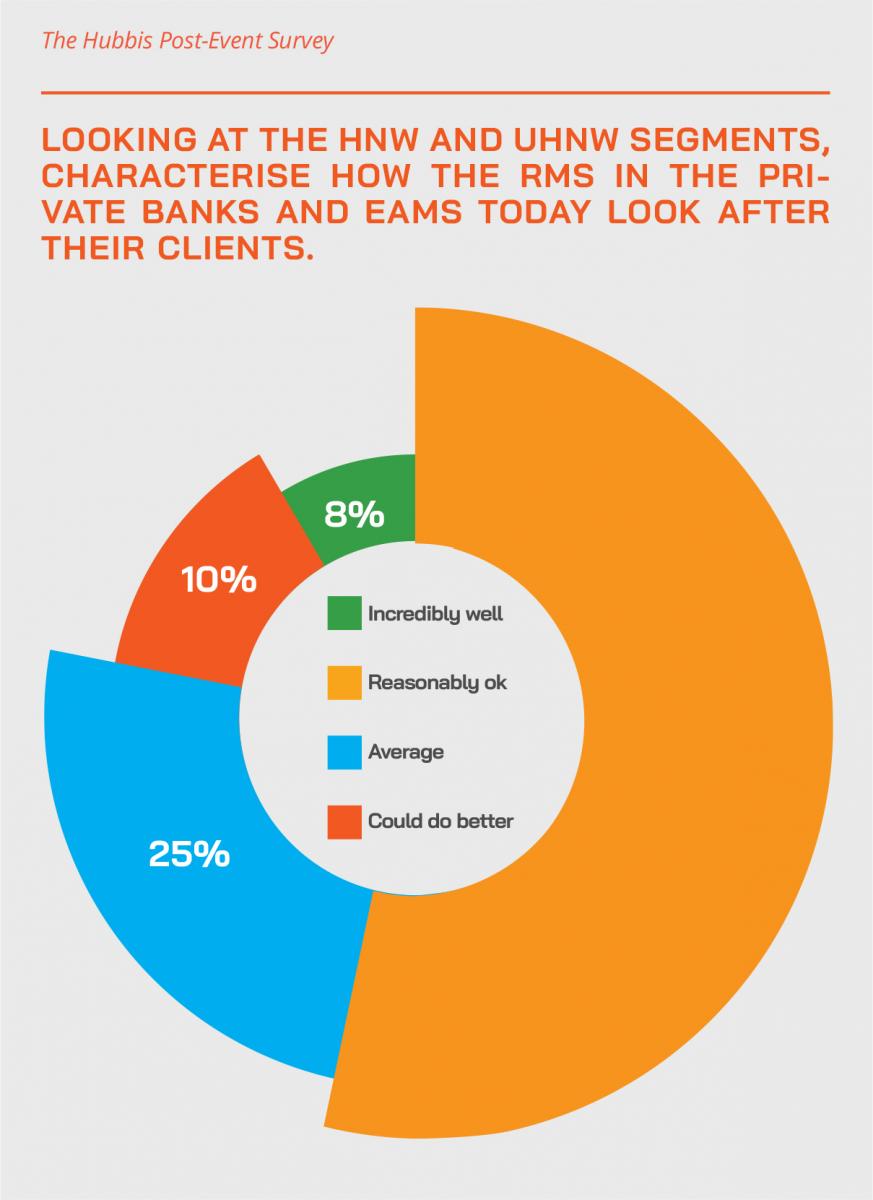

The Hubbis Post-Event Survey

In your view, in the HNW and UHNW segments, do you think the RMs will remain central to those relationships in the decade ahead? Why, or why not?

- Yes, the RMs will still remain central to relationships with HNW and UHNW segments as they need face-to-face contact which cannot be replaced or displaced by digitisation.

- Not really, I think the RM should shift to the UHNW segment because of the technology advancement, and more of the HNWIs will conduct investment activities by themselves.

- I think RM still play vital role in UHNW segment, however, services to HNW will be divested

- to digital platform.

- Only if they are able to make the transition from selling to providing advice. The proper digital tools can facilitate this.

- Yes. In my opinion, RMs will be the centre to their relationships, as the human touch still makes a lot of difference.

- Yes, because the RM possesses the ability for further relationship building by distinctively knowing all their clients' needs as they grow their wealth. It is not replaceable by technology.

- RMs will still remain central to those relationships in decade ahead because HNW and UHNW clients still prefer to talk their RMs, especially on more complex matters and solutions.

- Yes, if they can buck up and adapt. No, for those who choose not to move on.

- Somewhat. The robo-advisor will have an adverse impact on the RM especially investment related. The RM will still be the contact person, but less influential. Clients would be more institutionalised by the banks as clients become more reliant on their systems, and at the same time, RMs will haves lesser influence over clients and less ability to take them away when he/she leave the entity.

- Yes, it is a people business that requires empathy towards the client's verbal and non-verbal

- communication and needs.

- HNW and UHNW clients require complex solutions, and it is not possible to automate those.

- Yes, the RM has to source the clients!

- I think that the role of the RM will continue to evolve but they will remain central to the

- relationships between the private bank and client because in the end the client is a person.

- Ultimately, for HNWIs using a private bank/institution, they require a relationship manager (a person) that they can contact anytime.

RMs – still core to the proposition

As to the role and importance of the RMs themselves, an expert told delegates that the omnichannel approach ensures actually that there is scalability for the RM. “And scalability translates to profitability,” he reported. “That is because the client to RM ratio is expanding, even in the pure private banking segment, as well as in lower segments of wealth where there is more self-serve.”

Having said that, he observed that part of the key to successful omnichannel is segmentation. “But this is not simply categorised by AUM, but also based on the client behaviour and how the RMs actually interact with the clients, and vice versa,” he explained. “Are the clients more active traders, in which case we must ensure they use the digital portal for self-serve. Or if the client is more of a ‘validator’, as we call them, where they have the need more support, with these clients more served by the RMs.”

Expert Opinion - Gabriel Chan, Head of Sales, APAC, Wealth Dynamix: “With the onslaught of digitisation, many have debated that digital tools such as robo advisors, online investment will replace and displace the Relationship Managers. While we echo that wealth management firms are investing to extend digital channels for advisory purposes, we firmly believe the RM is still central and here to stay. Complemented by technologies, the RM roles will be uplifted to focus on the best opportunities, tailor financial products according to risk at scale and even pre-empt next investment products client will be keen. Digitisation gives clients choice of channel, convenience and reduces cost for the firms but wealth management is still a people business and RM high touch is needed for complex financial advisory such as taxation, compound investment to deliver even better client experience.”

Scalability and expertise

Another expert added that the other core issue to address is around the RMs’ scale and experience. “It is vital at the same time to train up the RMs out there,” he reported. “They were great on sales, they were great on the relationship building and on the financial products themselves, but less so on using digital products themselves, which is a new skill any RM these days needs to possess. Accordingly, we have training teams for digital products to support the RMs.”

RMs – needing support in three core areas

A fellow panellist agreed, remarking that the RMs need advances in three core areas. First is process efficiency from onboarding to transactional excellence, with proper operational support, whether it's done digitally or via someone in the back office. Then there is commercial effectiveness, the client 360 view, bringing in data and analytics and generally helping them develop business and be more focused on the client.

Then the third area is the client communication and engagement, with the ability to seamlessly and pleasantly deliver information, the analytics, research, the CIO view, and so forth.

The context – the client journey

“As a fellow panellist said earlier, the data on clients and other information is really only valuable if seen in the context of a complete understanding of the client journey,” this expert opined. “And it is the client experience that is going to be the differentiator in the wealth management world, so while products are available across all firms and switching costs are ever lower, the more the banks understand the clients and tailor and customise ideas and solution to their needs, the better they understand their clients, the better positioned they will be for the growth ahead in Asia.”

Another expert agreed, adding that it is vital to stay close with the client, and use every of the digital opportunities available. “Most of the clients here in Asia are multi-banked, so they key is to create the optimal kind of advice for that particular client, stay close to them and keep in contact with the client progressively.

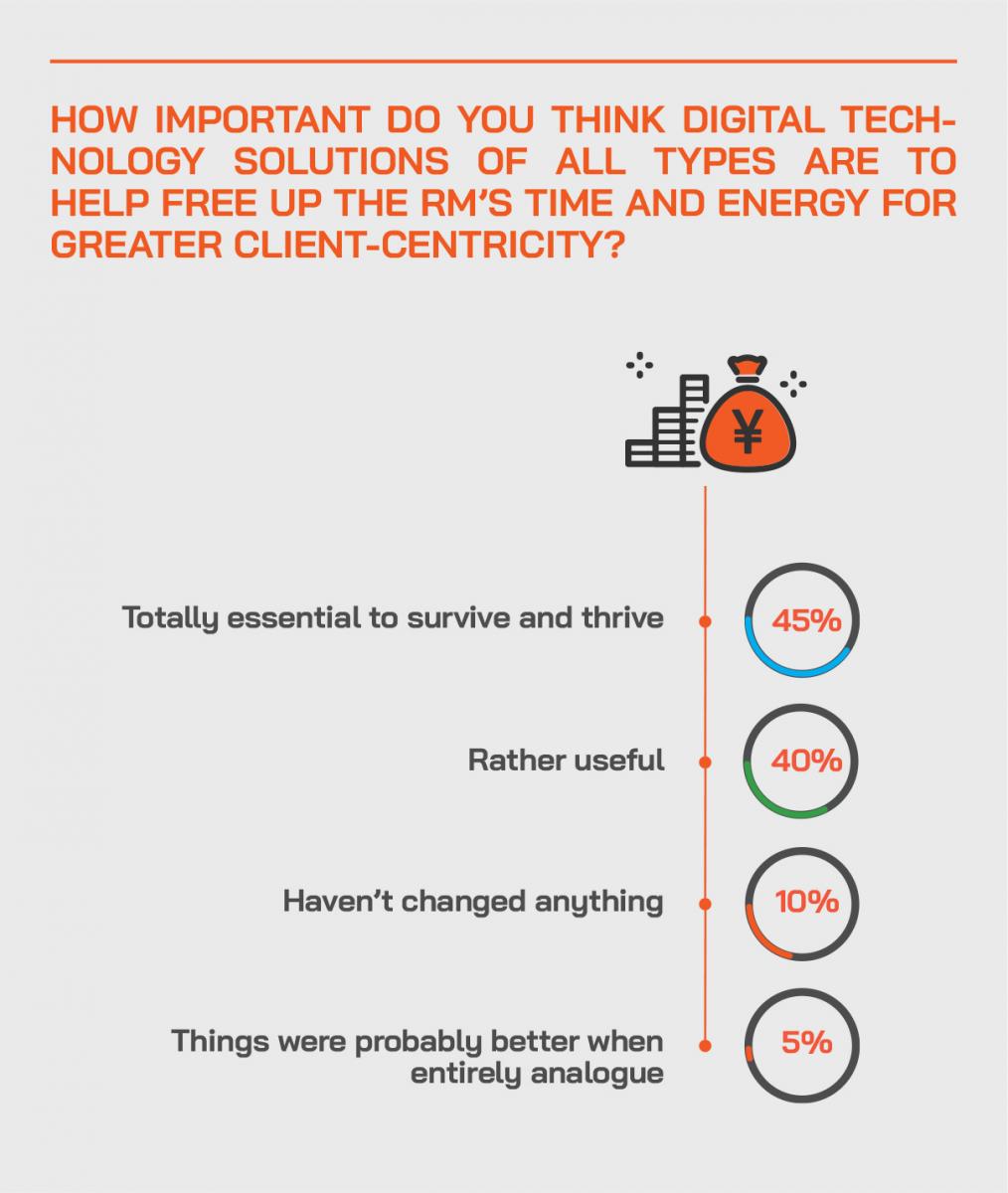

The Hubbis Post-Event Survey

What do you think the RMs need to better improve their capabilities, productivity, and to boost client satisfaction?

- RMs need to improve their digital skills so that they can be more tech-savvy when dealing with upcoming generations of HNW and UHNW individuals and families as they become better educated and more sophisticated investors.

- It is always in the banks best interests to enhance RM capabilities and knowledge, resulting in improved productivity and elevated client satisfaction, although the actual results may vary depending on individual RM.

- The ability to empathise and detect real needs, instead of selling into constructed 'wants' is a core requirement for an advisor's longevity.

- Make best use of AI and CRM software which uses algorithms to help them know what the client expectations are and what KPIs to develop.

- Have the right tools to boost their presentation and knowledge, communication skills need to be sharpened, they should accept digital adoption and expand outwards from the old 80-20 rule, as that is limiting their scope for business with the majority of clients.

- RMs need to improve their digitalisation by guiding active trading clients to use the digital platforms and tools available.

- Be adaptable and proactive in anticipation of change in working practices, markets and behaviour.

- Look for ‘outside the box’ ideas and solutions.

- Improve their awareness of and ability to converse about estate and wealth planning, including philanthropy, in fact on all areas that robo-advisory cannot replace as yet.

- Work out how best to manage both digital tools and align those with personal touch.

- In the current post-pandemic scenario, RMs should undergo upskilling and ‘retooling’ in the areas of digital banking and electronic processing of transactions.

- RMs should practice hyper-personalisation, diving deep into their clients’ histories and behaviour and activity and making sure they truly understand them, before then delivering relevance and suitability.

- In general, RMs need to improve their financial, technical and IT knowledge.

- RMs need technology to free them up for more face time with the clients. For example, automated yet personalised emails, automated portfolio monitoring, streamlining the pre and post sales procedure so that when compliance needs to check it is readily available to them and the RM does not have to manually answer routine questions.

- Good RMs should become more technology capable and be able to hand hold the client through the various investment, planning and also compliance issues that almost certainly arise.

Continuous innovation

“At our bank,” a guest reported, “our continuous innovation journey in the last few years has placed us in good stead to be the private bank that is at the forefront of technological innovation. As digitalisation remains a key strategic long-term driver and enabler of sustainable business growth, we have continued investing in and strengthening our digital capabilities.”

He told delegates the bank had also further built out its digital private banking app and platform, where clients can execute their trades, where they can self-service any banking needs, and review their positions and portfolios. “Again, since the pandemic hit, this has been incredibly active, especially for execution, with equities trading there surpassing the trades conducted via the RMs, at least for the plain vanilla, simpler products,” he reported. “In short, digital is here to stay and with that combined alongside a strong relationship manager who can support the clients in more complex wealth management matters, is working extremely well.”

Staying ahead of the pack

A banker addressed the question as to whether, as an early and prime mover towards digitisation, some of the other banks had now caught up and therefore it might be more difficult today to differentiate.

“We have definitely seen ourselves as the first mover and proven our commitment to this, and yes, competition has increased and others have been catching up with us,” he commented. “But what we are now doing, is refining the offering based on that success. And to offer some data points, around 80% of our clients are actually digitally enabled and are engaged with a frequency of up to 60% through the digital platform of up to 60%. And some 65% of our equity trades are done through the digital channel, and clients can still engage with the RMs as well, of course.”

Accordingly, with so much adoption amongst clients already in the bag, he reported that the bank is now well into phase two, where the bank is aiming to further automate to facilitate more complex products, and more complex processes. “We are advancing all these areas, and yes, we recognise that competition has risen since we set out on this journey in 2013.”

The hard yards needed to cut the heavy labour

Turning to automation of more mundane tasks, a guest observed that this type of ‘heavy sweat’ work remains cumbersome, but that digital solutions are gradually improving the situation.

“However, if you take a suitability process, for example, the Hong Kong regulator is basically enforcing similar regulations for a private banking client as a retail banking client, so there are still many forms. Accordingly, to redesign that process front to back and to then disclose and accept those disclosures digitally with the clients, that's where you can then gain the efficiencies. Similarly with KYC and AML risks. So, under the hood there is a lot of process reengineering banks need to do given the new norm from a regulatory perspective, to enable efficiency.”

The intelligent platform for intelligent wealth management

A technology expert reported that their platform offered clients the capability to make the onboarding process incredibly efficient and the portal allows all the requisite client and regulatory documents to be visible across all the departments and for the process and status to be completely transparent.

“The entire platform is intelligent because what we are doing is to have all the data points, all the different relationships that a client has with the bank on a single page, so that the relationship manager can meaningfully advise a client in terms of his portfolio, his risk level, what to invest in,” he explained.

Prompting and encouraging – with suitability

But he explained they also go one step further. “We then go one step further, as there is technology available today such as next best action that can actually prompt the RM to make informed decisions on what will be the most likely investment tool or product that the customer will buy. These are all available today, it simply depends on how the banks are willing to take forward.”

Moreover, he also observed that digitisation is also an avenue to drive costs down, via choice and convenience. “The banks may already have implemented the facility for customer to go on to the portal to make their own investment,” he noted. “And with next best action and rules, they are able to look at some of the investments that will be tailored to the risk appetite and do portfolio relocation as well.” And the result should be lower costs for the providers for those clients to execute their own investments and strategies.

Tailoring omnichannel to relevant segments and generations

An expert also addressed the issue of age suitability and the younger generations of private clients and also RMs.

“Younger, digital native clients know how to use digital tools in that sense, and thus feel much more comfortable with all this, where older clients might be more reluctant to actually use those. But from an RM’s perspective, you need to find the proper kind of balance, you need to have the internal capabilities to actually train and to make the RMs feel comfortable using technology. Accordingly, the approach we have taken is to train, expand knowledge, and find the right balance. And we also know that technology moves very fast, so the younger RMs of today will likely be challenged in the years ahead by technology that is new to them.”

He reported that the bank has very elderly clients adopting digital as well as much younger entrepreneurs. “Age is less of a factor perhaps than the social background, and it comes back to the need to train the RMs to project digital solutions and access to the clients, to explain why these are of benefit to them, from a risk perspective, from a timeliness perspective, from an efficiency perspective, so on and so forth.”

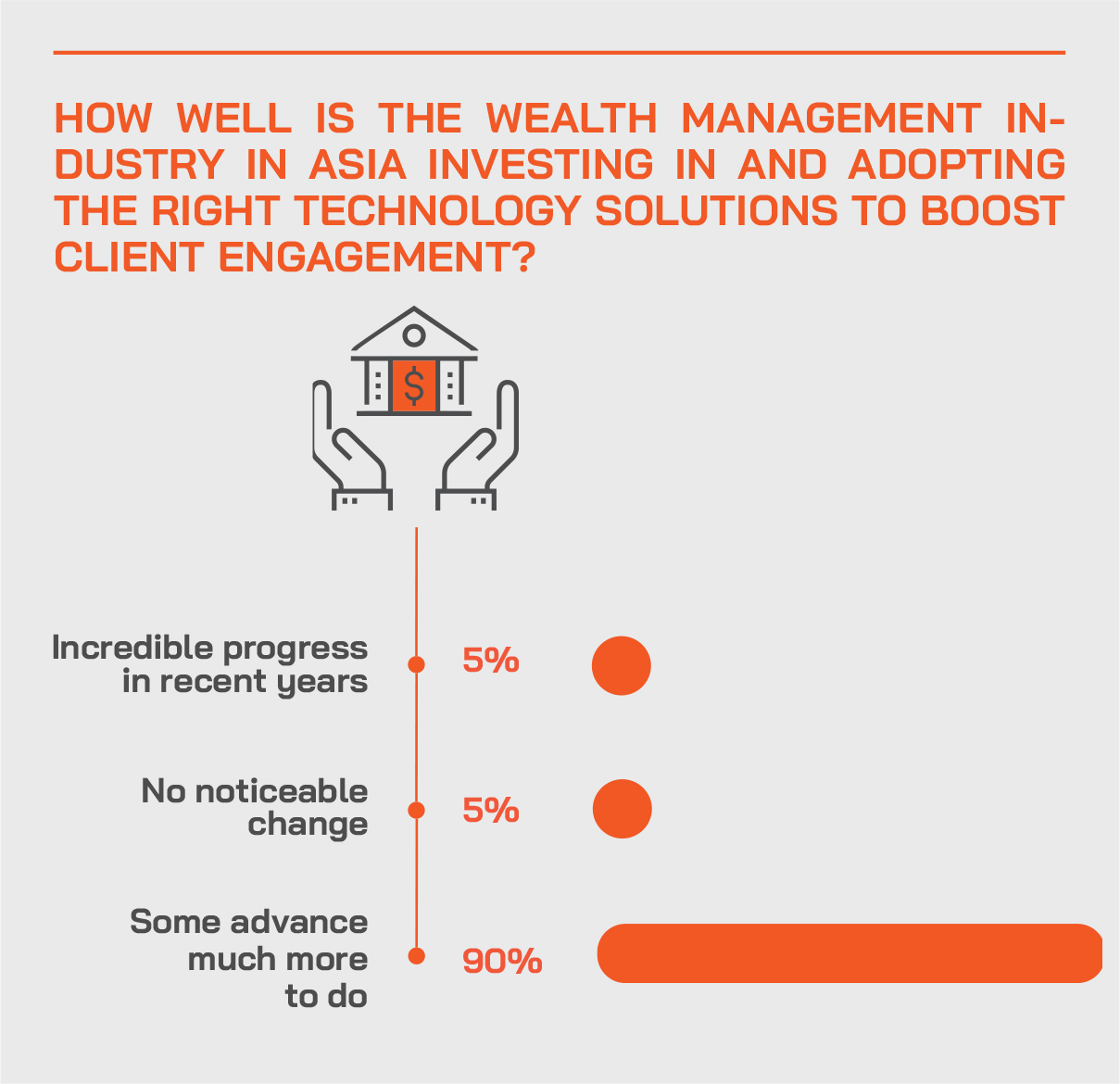

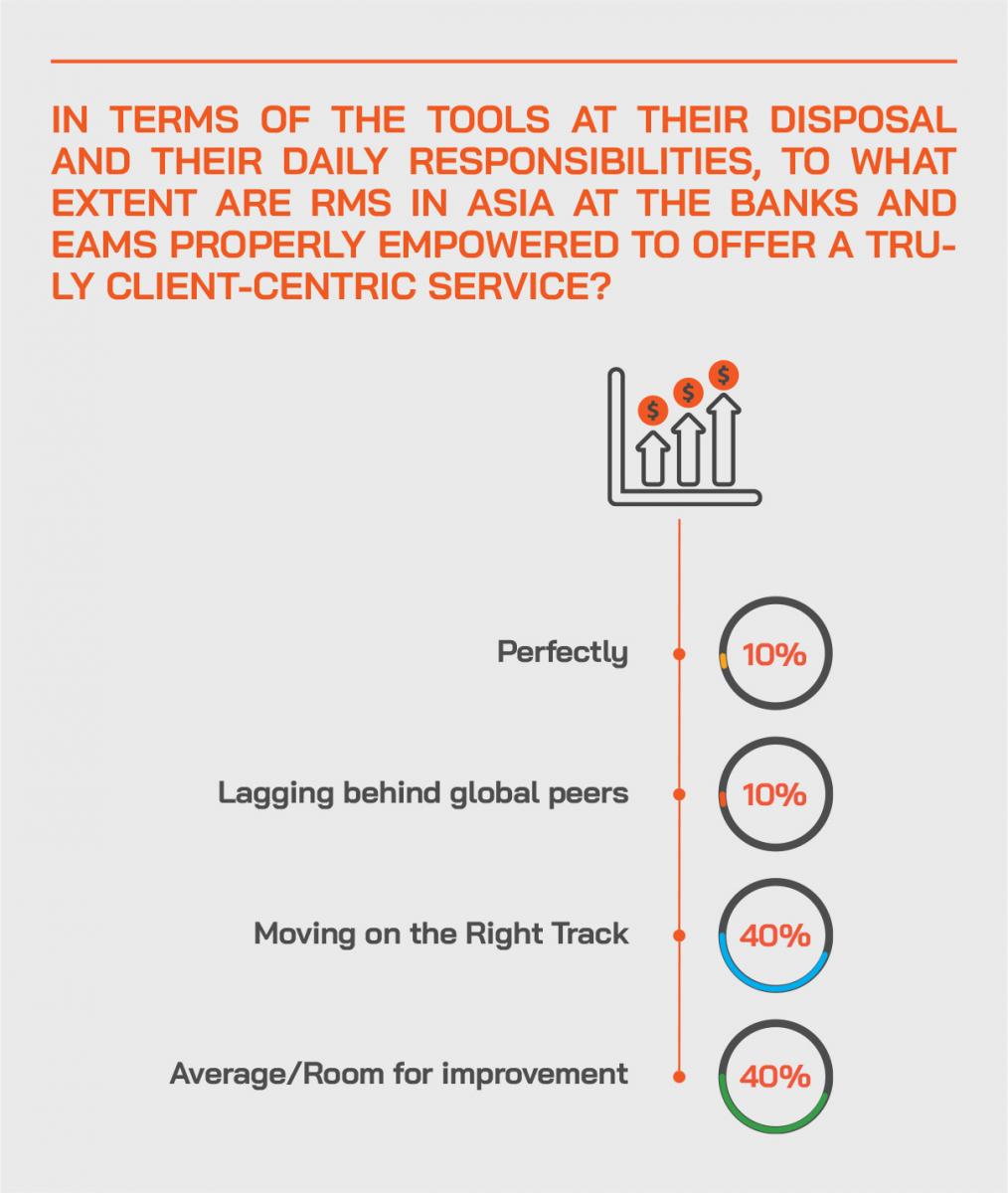

The Hubbis Post-Event Survey

In your view, are the private banks and IAM/EAM community doing enough to empower the RM? Why or why not?

- Yes, the overall industry of professionals are better empowered now to meet the needs of the future generations. I see and hear more professionals (especially they now WFH) attending webinars organised by Hubbis (and others) to acquaint themselves with developments in the industry.

- Not enough, as they cannot match with the speed of technology advancement.

- Not really. I feel their focus is still on old fashioned sales, and RMs are not yet incentivised properly financially to act in a client's best long-term interests.

- Yes. They are giving appropriate training and offer a better work life balance, helping RMs stay motivated to generate more business.

- Not enough across the industry. There is the right investment by the global private banks, but less so in the mid-tier and smaller boutique private banks.

- No, and much more is needed. That's the reason why RMs can't focus effectively on private clients and the churn rate is increasing.

- The RMs’ KPI is to sell and profit in between. They are not well equipped to serve clients' needs at different stages of their growth and evolution. The ‘One Bank’ type approach is good but usually private banking RMs don't even know the other parts of the bank. They are not keen to internally refer clients to other departments as it is not included in their KPIs, and they are defensive of their relationships.

- Yes, mostly. I believe the institutions are generally doing their fair share in uplifting the RM in their capacity and capability to bring in more volume and quality revenues for the banks. They just need to ensure that the RMs are continuously in the learning mode in sharpening their sales and marketing skills particularly in the area of handling objections amidst what is a very competitive arena.

- No, most banks are still judging RMs only by current sales and emphasis on compliance which takes up most of RMs time.

- No, due to costs in many cases and sheer inertia in the case of others.

- The bigger private banks are providing more training to their RMs, especially in the areas of

- compliance, investments and portfolio construction. However, I think the level of training/empowerment varies depending on the type of offering and scale of the institution.

- There is still a lack of delegation to the RM to deliver pricing to clients and therefore more effectively manage and direct the relationship. This should improve over time with better MIS. Clients want to speak with decision makers on all aspects including the pricing.

Ceaseless introspection and constant upgrades required

A senior guest closed the discussion by explaining that the priority for their institution is to continuously reflect on the market, the offering and the operations and then constantly upgrade and refine the digital platform and offerings.

“We are already seven-plus years old in this regard, and after all we tend to change our phones every three years, so we must continue to renovate, refine and upgrade, to boost the offering for the clients and for the RMs across the board, with greater automation, be that in the suitability space, or the KYC space, or further automating a chat, or automating other processes,” he explained. “We continue to challenge ourselves and to invest for the future, that must be a key priority.”