CREALOGIX – Leading the Digital Transformation Charge into Asia Pacific

Aug 11, 2020

The CREALOGIX Group describes itself as a multinational digital transformation specialist and a Swiss FinTech Top 100 company, as well as one of the market leaders in digital banking. The firm develops and implements innovative FinTech solutions for the digital bank of tomorrow and while its roots are coming from the wealth management industry, it also offers digital solutions for both retail banking as well as corporate banking / SME type of environments. The firm’s focus is on evolving bank’s and end customer’s needs for digitalisation in a secure and personalised way within a comprehensive user experience. Hubbis had the pleasure of meeting up with the new Asia-Pacific MD Karsten Kemna by video link recently; in this role, he is responsible for the strategic development of CREALOGIX in this dynamic growth market and will continue to drive CREALOGIX’s group-wide expansion and transformation to become the leading global provider of Digital Banking SaaS software in the region.

Kemna comes into his new role armed with considerable experience, having spent most of his career at Diebold Nixdorf (formerly Wincor Nixdorf), an IT solution provider for banks, where he was head of the company’s banking division in Asia Pacific. Before joining CREALOGIX, he was MD of the software company ERI Bancaire in Asia-Pacific. Kemna is energised and excited by the new challenge, and by the solutions that CREALOGIX offers the banking industry in Asia, and quite naturally he is itching to get out and about once the pandemic abates.

The CREALOGIX Group is a Swiss FinTech 100 company and is among the global market leaders in digital banking in Europe, Asia and beyond. The firm develops and implements innovative FinTech solutions for the digital bank of tomorrow. According to its literature, banks can use their solutions to react to evolving customer needs in the area of digitalisation, enabling them to hold their own in a very demanding and dynamic market, and to remain one step ahead of their competitors. And CREALOGIX has a broad suite of state-of-the-art solutions for not only wealth management, its traditional business, an area in which the firm believes it will be able to compete highly effectively in Asia, but also with a stronger push for retail banking and corporate banking solutions going forward. Starting from a small but healthy customer base in Asia, with Kemna on board, the company is aiming to expand rapidly.

A solid track record

The group, founded in 1996, has around 700 employees worldwide. CREALOGIX Holding AG (CLXN) shares are traded on the SIX Swiss Exchange. The company counts more than 550 banks worldwide as customers in countries such as Switzerland, Germany, Austria, the UK, Spain, Singapore, Hong Kong, Thailand and Saudi Arabia, and CREALOGIX has carried out more than 1,200 installations for its customers and has a wealth of valuable experience. Offices are located in most of the key countries where the firm has an extensive client base.

“We provide banks and other financial organisations with reliable, and forward-looking support for their digital transformation journey, and we empower them to successfully master the inevitable digitisation of their business as well as offer opportunities and perspectives that actively shape the digital future of the financial world,” says Karsten, opening the discussion. “With the firm’s many years of experience and our unique, innovative solutions, we are your trustworthy partner for secure digital transformation.”

Asia-Pacific – a major priority

CREALOGIX considers Asia-Pacific to be one of its strategic key markets globally, and although only with a relatively small team of six persons on the ground thus far and a number of clients in hand, the firm is making far-reaching investments in order to strengthen the local organisation on a sustainable basis. Together with its vast partner network, the Swiss software company is addressing the growing demand for digital products in wealth management, retail banking and corporate banking in the vast Asia-Pacific region, where the firm sees huge opportunity ahead.

“We are delighted to have Karsten on board; he is an exceptionally experienced industry expert, and through his leadership we will to be able to serve our customers and the overall market in Asia-Pacific even better,” said Oliver Weber, Chief Executive Officer of CREALOGIX back in April, when the news became public.

Kemna has lived in Singapore for over 13 years and has a strong and deep engagement with the business community of the region, as well as with local social and family life. He is married to a Singaporean, and they have two young children under the age of four. “If you ask me what keeps me awake at night,” he quips, with a smile, “it is not the new challenge here at CREALOGIX, as we have great potential ahead, it is actually our young children. But I would not swap that for the world.”

Innovative to the core

CREALOGIX offers a variety of FinTech solutions. The CREALOGIX Digital Banking Hub provides open architecture for open banking, the firm’s website explaining that its scalable, secure and highly modular software solutions and products enable banks to implement their digital banking strategy effectively, quickly and cost-effectively.

“The Digital Banking Hub is our core innovative architecture for open banking of the future – online, mobile, or in direct contact with an advisor,” Kemna reports. “The API-based architecture allows for seamless integration with all the banks’ systems, ensuring that and open banking demands and regulations such as PSD2, for example, are met effortlessly.”

Front-end focus

“When we talk about digital solutions,” Kemna explains, “we talk mostly about the front-end, for example, the mobile banking app or e-banking solution. We compete in two areas, the end customer using, for example, a mobile banking transaction, and also the advisory side, specifically in a wealth management situation, the relationship manager and what he would have on his hands in an advisory both face to face or remotely ‘virtual’, such as has been the necessity since this pandemic.”

Sharpening the focus in Asia

Historically, CREALOGIX was more focused on wealth management and private banking, but the firm in the last few years has enjoyed tremendous success in Europe in retail banking, as well as corporate banking and SME-type digital solutions. “We are now reorganising and segmenting,” he reports, “so in Asia, we will be able to target more client solutions not only in wealth management, but also in retail and corporate banking. And when we talk about solutions, it is really a software product that we are trying to implement in the banks, and we are very much flexible and agnostic when it comes to the core banking supplier we would be implementing on top, or whether it is cloud-based or on-premise model.”

He observes that in Asia-Pacific, the firm has a good track record and a positive story. “We have a healthy nucleus of clients,” he reports, “and we are on a growth path in this part of the world, but we recognise the width of the Asian banking landscape, which is why we are really trying to invest additional resources to bring CREALOGIX Asia-Pacific to the next level. The focus is for the time being mostly on the sales and business development side, since we do use strong partnerships on the implementation side. From that perspective, and looking at the currently planned additions to the team you can be sure that whatever situation you engage with us will result in a very positive outcome.”

And Kemna clearly believes that CREALOGIX is optimally positioned for the challenges ahead. “Wealth management customers have high expectations of their bank’s products and services,” he observes. “At the same time, legal regulations and documentation requirements are becoming increasingly important for banks, while internationalisation and increased competition are reducing margins. On top, especially in certain parts of Asia, with a growing middle class and more mass affluent people coming up, the banks have to reconsider their strategy for these type of client groups.”

“Ultimately, the digital transformation is in full swing and business models, as well as services, need to be updated and adapted to new technologies and customer expectations. Also, considering the more positive sides of the current virus situation, banks do speed up their digital roadmap in order to be relevant and competitive in the future.”

He explains further that the ready-to-use products and modules allow private banks and other wealth firms to offer their private clients modern, digital services for mobile banking or financial management, thereby creating greater customer loyalty especially with the younger generation of tech-savvy affluent people.

The CREALOGIX Offering

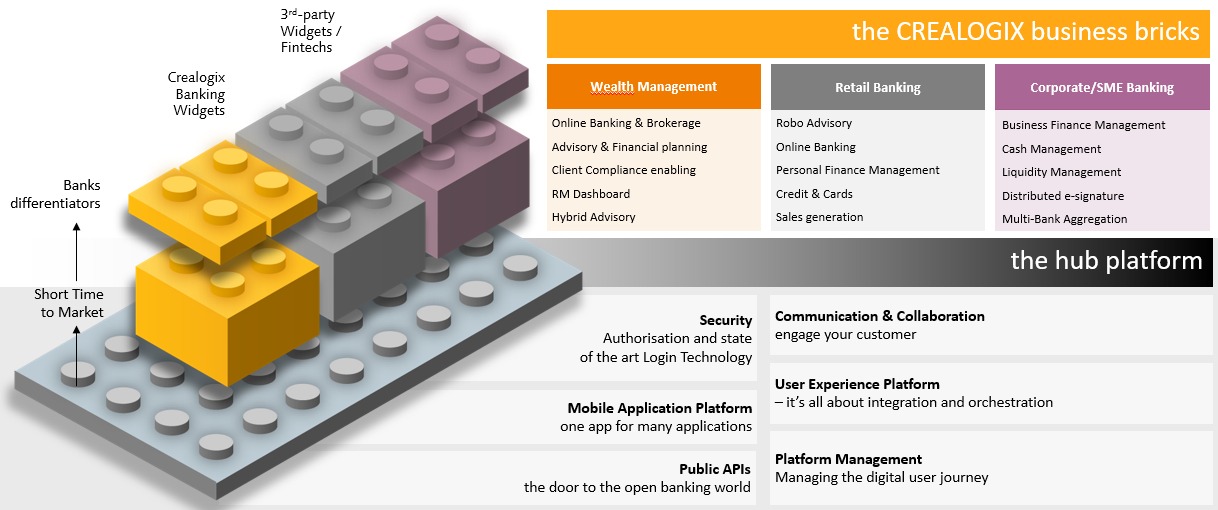

CREALOGIX has a suite of products created for the segments of wealth management, retail banking as well as Corporate / SME banking. The common engine driving these products is the Digital Banking Hub platform which acts as a core architecture to open banking and allows banks to integrate seamlessly with third party providers via APIs.

For wealth management, CREALOGIX offers a variety of products for online banking and brokerage, advisory and financial planning, client compliance enabling, RM dashboard, and hybrid advisory, with a target audience of both the end customers of the banks as well as the relationship managers.

For retail banking, the firm offers banks’ end users with a comprehensive online banking platform with a completely configurable dashboard. CREALOGIX also offers a personal finance management and robo advisory tool for personal investment to help the customers understand their financial situation and anticipate future potential performances with such personalised analysis and prediction tool.

For corporate/SME banking, CREALOGIX provides business finance management, cash and liquidity management and multi-bank aggregation as key features. Most of the banks’ corporate and SME customers have multiple bank relationships which is why the multi-banking portal is an essential requirement. By positioning the bank as a central contact point for its customer’s financial needs, banks can provide services to build engagement and loyalty and extend cross-selling activities via a single portal.

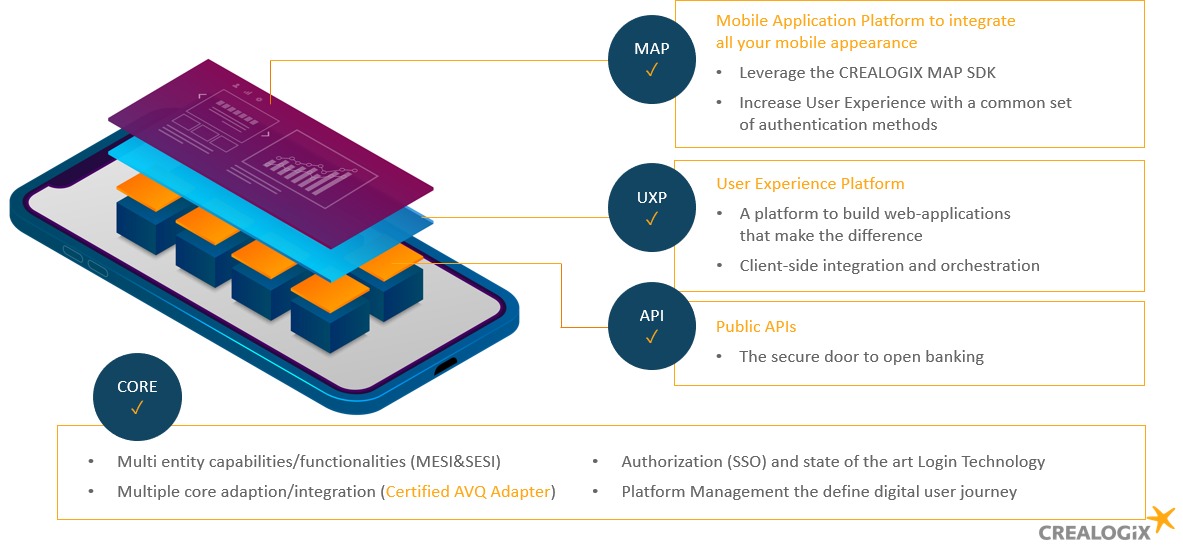

CREALOGIX Digital Banking Hub (DBH)

The Digital Banking Hub provides a scalable and state-of-the-art platform with an efficient layer to facilitate the integration of functional hub modules provided by all units across CREALOGIX products. Its functionality will be built to address functional and non-functional requirements across different markets. Core functions include security, identification and authorisation, auditing, logging, UI & mobile framework and API layer, just to name a few.

The CREALOGIX Digital Banking Hub allows banks to easily deploy and maintain any combination of such functional modules. It will also provide the flexibility to manage and extend capabilities at all levels, spanning from business logic across APIs to front-ends.

Being part of the DBH, the CREALOGIX User Experience Platform delivers an attractive, high quality user experience on web applications that impress demanding digital users. It optimises the customer experience and facilitates the interaction with relationship managers or service staff. Its modern UI and workflows across all CREALOGIX applications for both mobile and desktop will allow third parties to build compatible UI elements so that financial institutions can go beyond what we offer.

On the top level, the CREALOGIX Mobile Application Platform increases the user experience with a common set of authentication methods such as biometrics which can be all integrated throughout the different mobile experiences of the bank. It is a wrapper for anything from a simple, single application to a complex combination of different underlying applications, enabling banks to offer their customers a consolidated banking app for a single point of contact in one place.

CREALOGIX Financial Advisory

An innovative software solution for the relationship manager of the bank which is designed for a digital wealth platform with standardised client service processes in a set of configurable, fully paperless workflows for face-to-face or telephonic advice or hybrid omnichannel consultation and sales of financial products. Client CRM-type data is combined with investor profiling and can be used for ongoing advisory and discretionary wealth management services.

CREALOGIX Financial Advisory helps wealth management advisors to perform better, improves quality of service for end clients and reduces costs by benefiting from one standard paperless set of processes and information flow.

CREALOGIX Banking Portal

The CREALOGIX Banking Portal is a comprehensive front-end digital banking platform incorporating day-to-day current accounts and investment features. This forms the center of our feature set for retail banking and supports various business processes of bank staff as well as a fully designable set of UI for end user self-services on desktop and mobile. Banks can utilise the banking portal for sales generation by pushing relevant marketing campaigns to a certain customer segment.

CREALOGIX also offers a new communication channel for banks to enhance existing digital banking services with secure live chat features to build closer relationship with customers. Banks can serve customers, especially the millennial and digitally native generation who are highly tech-savvy and who prefer ad-hoc chat to traditional email, phone, or meeting for advice and support.

With this new feature, CREALOGIX helps banks to redefine the relationship, bringing two-way interactions back to digital banking and therefore combining the best of both worlds. It provides personalised banking services and bridges omnichannel customer interaction from onboarding to successful long-term relationships, while establishing a secure, manageable, and efficient set of processes around the chat channel.

The digital journey – keeping on track

Kemna then steps back to look at the bigger picture, commenting that from a value proposition it is vital for banks in general, but especially for wealth management organisations to have the right digital solutions and to keep investing and modernising, and to keep the end customers at bay while also giving them the chance to transact digitally.

“Indonesia is a good example,” he observes. “The wealthy people become younger and younger by the year and are increasingly tech-savvy. And specifically, in the world of wealth management, we have integrations or options for the whole advisory process from onboarding and goal-based advisory and investments, in short along the whole customer journey.”

He adds that the open banking API type of environment that CREALOGIX completely embraces makes it super-easy to connect with other tools, with other legacy software, and it makes it easy for financial institutions to bring new functionalities to the market. “Flexibility and agility are key to the future,” he says. “And overriding all of this digitalisation, we are helping our clients to generate new business and generate new revenues by enabling more and more transactions, in particular mobile, besides making it easier to onboard new customers.”

Kemna adds that the back-end, the traditional core banking engine, is generally rather old-fashioned across Asia, but that the future is more about user experiences and journeys, plus how you drive transactions and customer engagement at the front end, as that is what is truly driving customer acquisition and retention.

“For example,” he says, “I might have a portfolio with a German online bank and every time I even look at my portfolio current standings I have to open up one additional app to get approval to get into the other app which I find rather cumbersome and annoying. It is essential to win the battle for the customer experience, to be customer friendly, as well obviously as safe and secure. To do so, the organisations need to invest smartly and keep ahead of the game.”

Asia – a world of opportunity

As to opportunities in Asia, Kemna observes that the wealth management space in the region has tended to be somewhat behind the European curve, but that organisations not only in more mature financial centres such as Singapore and Hong Kong are determinedly addressing that gap. “Banks are modernising their existing products, they are looking at especially, the API supporting type of products, they are increasingly receptive to bringing into the region this open banking culture from the more mature markets. And the underlying market itself is dynamic, with private wealth creation so strong across all categories of wealth.”

He adds that corporate banking and the SME space is another of the firm’s strengths in terms of products and is a segment that is evolving rapidly in the region.

Kemna also highlights CREALOGIX’s capabilities in the neo bank space in Asia, which is developing apace, particularly in Singapore, Hong Kong, Taiwan, and Malaysia. Here the firm is looking to partner up with other innovative, fintech type of solution providers to create a compelling value proposition for these neo banks;

“Our end-to-end approach is well suited to working together with some of the more innovative cloud-based vendors in and around this space to create a bigger solution,” he explains. “Obviously we are focussing on our front-end capabilities but working with others maybe in the backend to be a trusted partner within this new part of the industry would be very interesting. The neo bank phenomenon also means that traditional banks will have to adapt more quickly which means again they may have to re-look into the digital strategy sooner than they would like to actually, so I think this whole initiative of the neo banks is going to make some significant changes in the market space, and I am convinced that also we at CREALOGIX can benefit from this.”

The best, not the cheapest

Kemna explains that if customers are looking for the lowest entry costs to these products, it is not CREALOGIX.

“We are drivers of innovation, and we have an excellent track record and credibility,” he says. “Innovation, speed to market, user experience and reliability do not come cheap. We are a very high-quality and proven provider based out of Switzerland, but clients adopt our offering because it represents value.”

Kemna draws the discussion towards a close by reiterating his view that by having a strong digital product, the bank is able to create more leads, win more potential customers and engage more easily through more digital touchpoints. “Secondly, if you have the right level of customer servicing, a client platform can also help to increase transactions, and that also means transaction fees and then services fees. And if you can help the mass affluent type customers do most by themselves, the RMs then have more time and the firms more resource to focus on the HNW and UHNW categories.”

Kemna closes by saying that CREALOGIX offers him a great opportunity to build from the ground upwards. “I am pleased to call Singapore home, it is where we are raising our family, and where we thoroughly enjoy living,” he says. “Similarly, I am excited by the prospect of nurturing CREALOGIX in this region, which offers such diversity, dynamism and opportunity.”

Key Priorities for CREALOGIX in Asia

Kemna reports that the number one mission is to ramp up the Asia-Pacific business, including investment in strengthening the team and growing the local organisation in the region. He notes that the firm today has only six people in Asia and his mission is to grow the team into a much more complete organisation. “Accordingly,” he reports, “we are currently recruiting, and I think by the end of September we will double that number.”

“Secondly,” he says, “it is really important for us, especially in the ASEAN countries, to build a comprehensive partner ecosystem, mostly on the business development side and on the implementation side, we already have a trusted partner with Synpulse that we are already doing a lot of work with not only in different countries in Asia-Pacific, but also in European projects.

This partner ecosystem will consist on one side of door openers in the countries, local system integrators that have the right networks locally to bring solutions to the market, but also more regional solution providers that would complement the CREALOGIX market offering into something even more unique and appealing. Lastly, there is also a need to strengthen the relationship with the top consultancy firms as those do have lots of say when it comes to the banks’ digitalisation strategies.

And the third mission is to significantly boost brand awareness in the region, to let bankers especially, but also the broader range of the financial sector and wealth industry know what we do and what the relevant products are. “We want to make sure people associate the firm with something very innovative, with something very high-quality and positive,” he reports, “and therefore also through this brand recognition to win more leads and bring more opportunities.”

CREALOGIX on Digital Transformation and the Dangers of Falling into the ‘Legacy Thinking Trap’

In a White Paper that CREALOGIX published this year, the author, Dr Richard Dratva, Co-Founder and Chief Strategy Officer at the firm, highlights how the positive but disruptive changes of the digital era are putting established financial brands under pressure to act. Above all, banks and wealth management firms will have to find answers for five problem areas the report identified. These are: too slow to compete, a cluttered product portfolio, scepticism towards open banking, fear of change, and a widening technology gap. He warns that too many banks and other financial institutions invest unwisely in upgrading tired, legacy systems, and not enough on shiny, new solutions to fast-forward their organisations into the brave new world.

“In response to their new digital-only competitors many conservative banks and wealth management firms are inclined to follow a common sense and low risk approach,” Dratva writes. “But the tried and trusted recipes are often leading into a dead end since the strategies used are based on old habits from the analogue age. Established financial institutions do what intuitively seems right to them against the background of their business practices, operating principles and processes that have evolved over decades. Yet these established approaches often are mistaken in the digital era. Nevertheless, with the right ability to challenge convention, it is easy to find solutions for the bank of tomorrow.”

Dratva explains how the rapid rise of FinTechs and challengers has highlighted how unfocused and slow large established financial institutions have become. Under the surface, incumbents struggle with decades of complexity and costs from hundreds of different systems to maintain.

Describing what Dratva terms the ‘legacy thinking trap’, he explains that established firms often dedicate most of their technology budgets to the maintenance of their existing systems, but the disproportionate cost of those legacy systems eats up the valuable resources needed to create new useful features which their customers can see or feel, which add up to make a digital user experience that can compete with the sleek offerings of the challengers, he observes.

Then concluding that these organisations need to adopt a counterintuitive strategy, he states that banks and wealth management firms need to be much more aggressive about prioritising the delivery of tangible improvements for the end customer. “Modernising the underlying systems is important,” he writes, “but innovation is even more important – and, in order to be innovative, the existing resources must be radically redistributed. Moreover, a budget boost in this area will send a clear message to the company’s teams that rhetoric must turn into action.”

There is an interesting observation also from René Raabe, Head of Sales, Private Banking and Wealth Management at CREALOGIX. “In order to become faster and more innovative,” he comments, “but also in order not to annoy their customers, financial institutions must become leaner and more focused, and this means they will have to radically streamline their offering. However, one size doesn’t fit all. Therefore, my advice for banks is to personalise their user experiences instead of constantly showing all options to all customers.”

Dratva also observes that established financial institutions often take a defensive stance against open banking, as this, he explains, means that they have to share their greatest treasure – their customer data – with potential competitors. “For this reason,” he writes, “many banks consider it rational to limit the opening of their systems to the bare minimum, just enough to satisfy open banking regulation. However, in the future the real drivers of open finance will not be the regulators, but the bank clients – and the bank clients know what they want: a banking experience that is corresponding to their digital lifestyles.”

The conclusion Dratva reaches is that as the financial world of tomorrow is hyperconnected, it is far better to be part of this phenomenon early on than to fight it. “The key to future success,” he writes, “will be to use third-party data intelligently, rather than just make your data available to third parties – open banking is only the beginning. Be it energy, mobile phone contracts or media services, many bank customers can readily see themselves purchasing non-financial products from their bank. This enables established financial brands to tap into new digital sources of revenue by offering additional services.”

Managing Director Asia Pacific at CREALOGIX

More from Karsten Kemna, CREALOGIX

Publications & Thought Leadership

Digital Convenience in Wealth Management – Driving an Innovative and Personalised Client Experience

Latest Articles