Publications & Thought Leadership

Compliance and Regulatory Challenges in Private Wealth Management for 2021

Apr 14, 2021

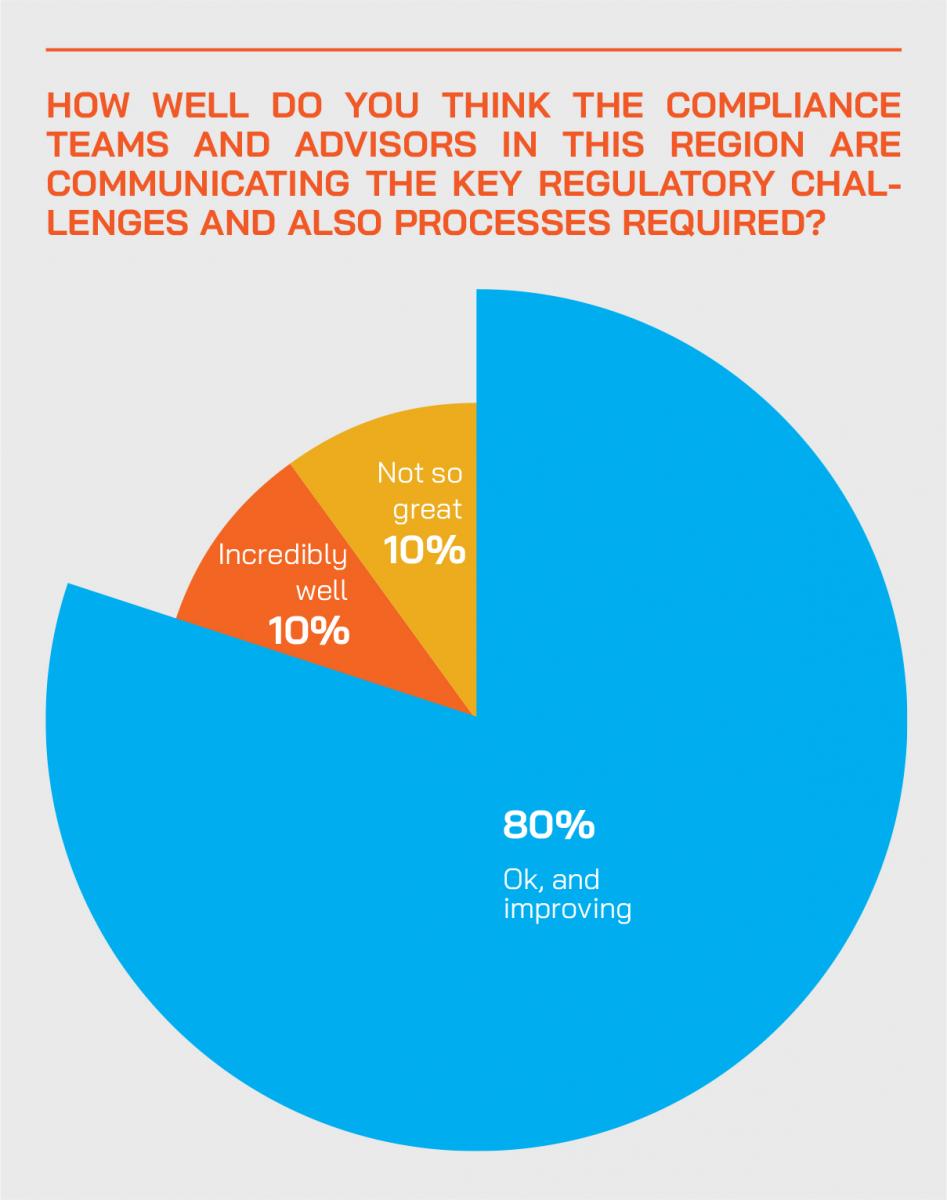

As the Asian private banking and wealth management industry goes through various degrees of recalibration and strategic rethinking since the onset of the pandemic, the one thing that has not changed is the relentless rollout of regulations across the globe, as seemingly nothing will halt the drive to regulate at local, regional and global levels. The Hubbis Digital Dialogue of April 8 tackled many of the most crucial current and upcoming topics on regulation and compliance.

What are the main compliance challenges for the year ahead, both globally and also specifically within Asia? In what ways has the pandemic impacted the wealth management community in its adaptation to the new rules, monitoring and enforcement of, for example, CRS, AEOI, Mandatory Disclosure, Economic Substance and BEPS, Accountability & Conduct, and whatever other new regulations and compliance protocols have arrived, or are due? Where does the underlying business gel with the demands of compliance, or is regulation so pervasive and indiscriminate that it is hampering the revenue generation and profitability of the players in this industry? Have onboarding, KYC, AML, and transaction monitoring and reporting been functioning properly and what new rules and challenges lie ahead in these areas? How about privacy, security and cyber hygiene in the current environment, is that not an insurmountable challenge when most of the industry is working remotely?

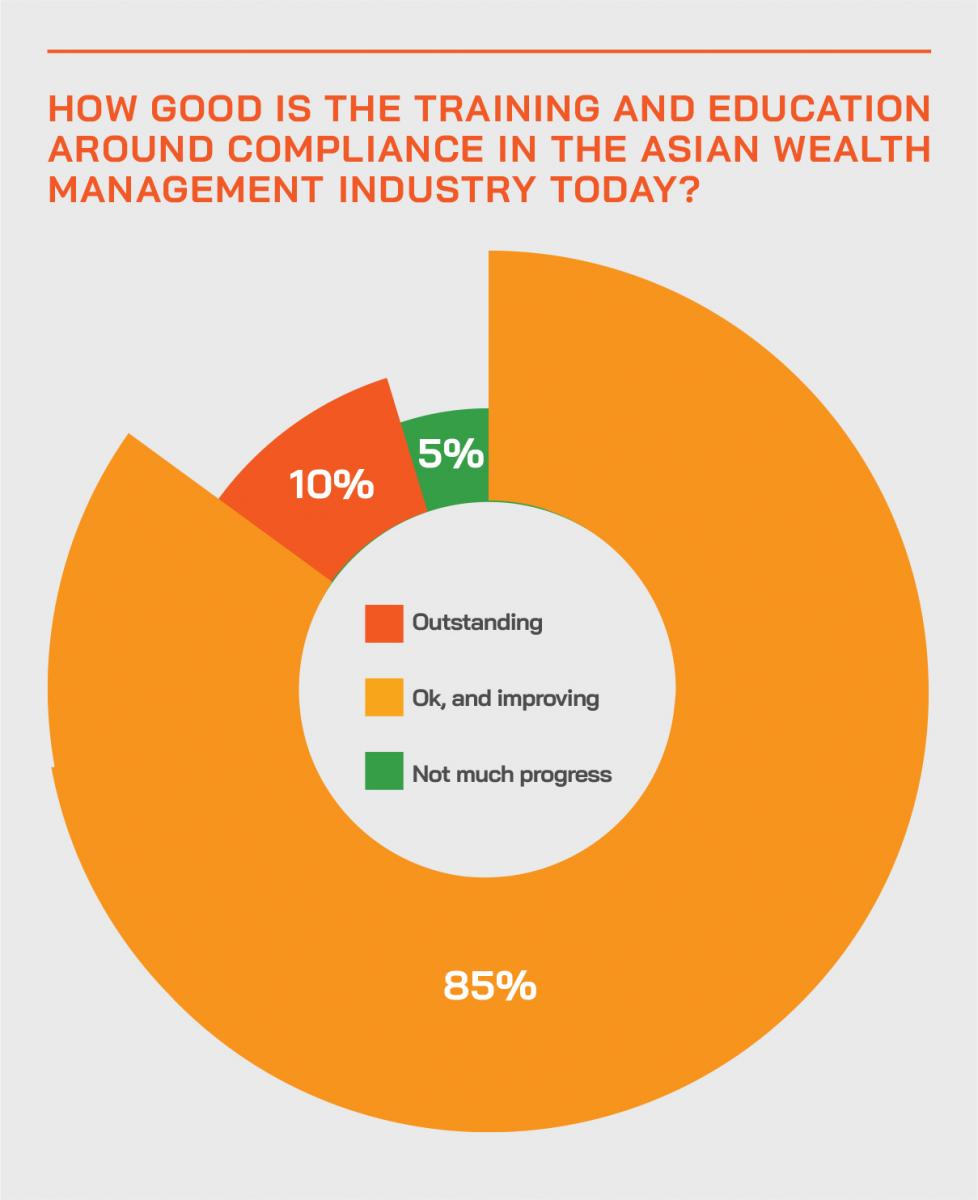

How do compliance teams at the banks and the independent wealth firms actually conduct their roles efficiently, when remote working is now the norm, not the exception? What roles do training and further education play in the rollout of effective compliance, both amongst the compliance professionals, but also amongst back, middle and front-office team members? Aside from the rules themselves, what role do ethics and self-regulation play in the evolution of the wealth industry, and are Financial Institutions in Asia really ready for the ‘Culture and Conduct’ revolution?

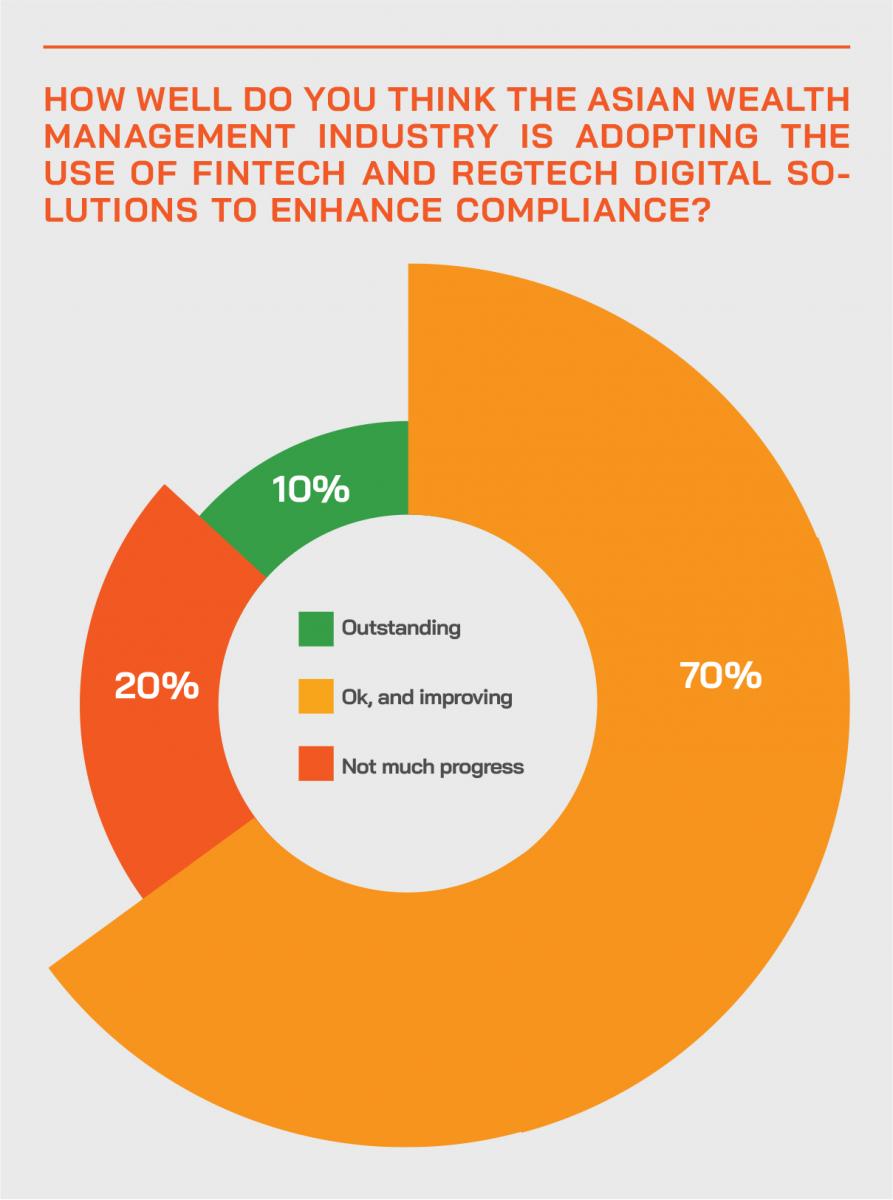

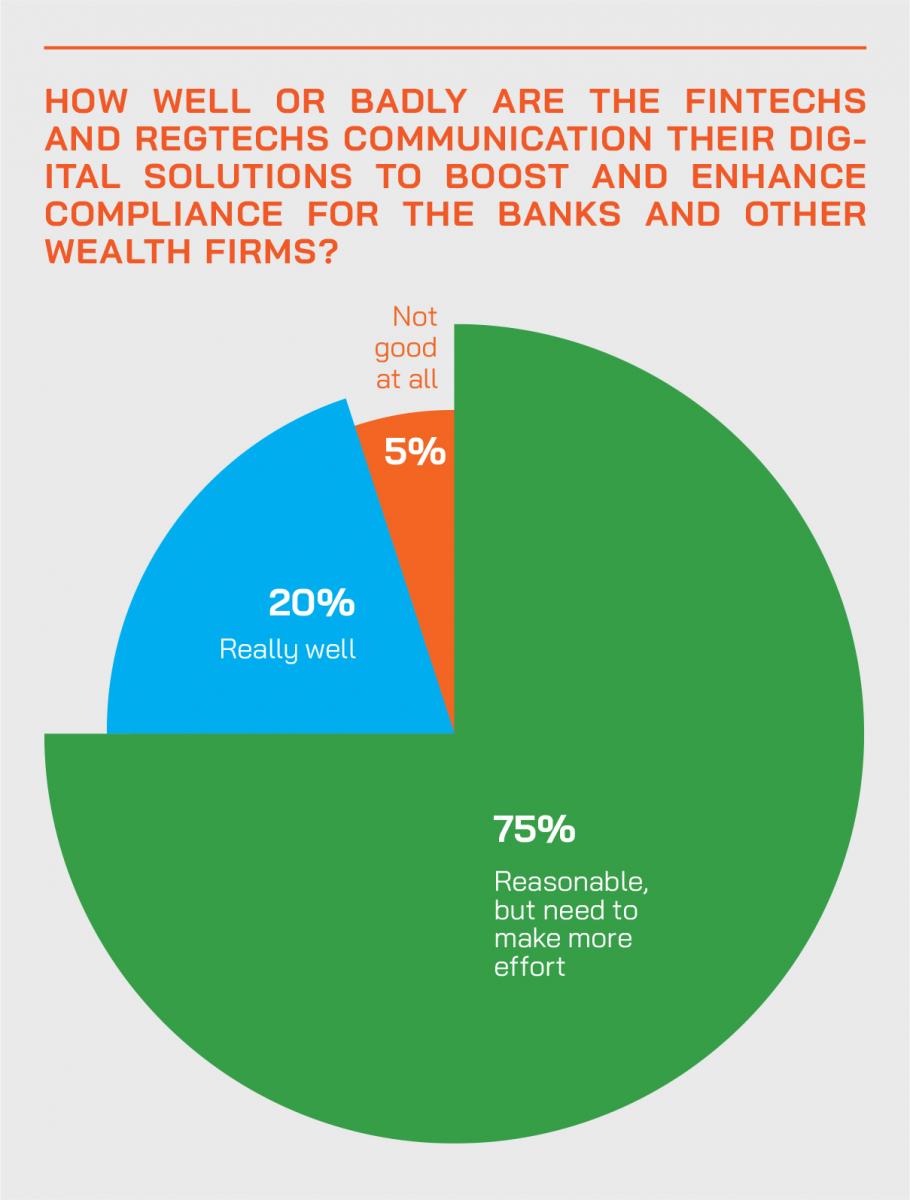

And what established or newer digital solutions are being introduced that can truly help the wealth industry as it struggles with all these new rules and oversight, and are these digital solutions actually achieving their stated goals? How does the industry make it selections from the growing range of sophisticated solutions out there? Are compliance experts, digital solutions providers and the leaders of the WM providers speaking the same language?

These and other key issues relating to regulation and compliance we debated by our panel of experts in what was a lively and engaging discussion.

The Panel

- Ralf Huber, Co-Founder, Apiax

- Stephen Yee, Managing Director, Head of Compliance, Bank Julius Baer

- Vincent Koo, Head of Compliance, EFG Bank

- Natalie Curtis, Partner, Herbert Smith Freehills

- Rolf Haudenschild, Co-founder, Ingenia Consultants

- Neil Thomas, Head Sales, Asia Pacific, SIX

Setting the scene – nothing remote about regulation and compliance

A banker set the scene for the discussion by commenting on how rapidly they had needed to adjust to remote working practices in the past year or more, and he observed that remote working is likely to endure well beyond the pandemic for a certain portion of the workforce, a view supported by internal surveys that bank had conducted. But he added that the relentless demands of the regulators and compliance protocols are anything but remote for the wealth management industry.

Another banker said the early period of remote working caused major headaches and logistical hurdles to overcome, right down to the availability of sufficient laptops and home PCs of sufficient quality. “But we can see that a year later, we have done rather well and the business itself has performed well,” he reported, “with record numbers in 2020. That is the beauty of the human situation, we can and do adapt to our new environment.”

The new ‘normal’

The panel seemed to agree that a considerable degree of remote working is very likely to be the new normal, looking ahead, essentially a mixture of home and office work. “WFH reduces the human interaction, staff engagement,” a banker observed, “but it gives the employer more flexibility and reduce costs. From my own viewpoint, I did not feel that efficiency and productivity have been reduced. If there is a negative impact, it is the blurring of office time from personal time.”

Rules and compliance developments in the headlights

An expert reported that in Singapore, the Monetary Authority of Singapore has been rolling out new regulations in particular on individual accountability and conduct, with those coming into play later in 2021. Another area of focus is the drive from the MAS for cyber-security, privacy and technology risk management, described by an expert on the panel as the biggest challenge at the moment, especially because of remote working practices.

Culture & Conduct in the limelight

Another expert highlighted the global drive to accountability of personnel in the financial world, a responsibility that lies both with the individuals and with their employers.

“With these regimes, we're the regulator put a lot of onus back on the organisation to address errant behaviour,” they explained, adding that at the ground level the regulators seem to be seeking to mitigate some of the misbehaviour, especially now that WFH is so prevalent, reducing face time between the business leaders and their teams. They also noted that cyber-security and privacy are key issues and that the regulators are shifting the burden increasingly onto the businesses, driving an enhanced culture and conduct environment to aid progress in this area.

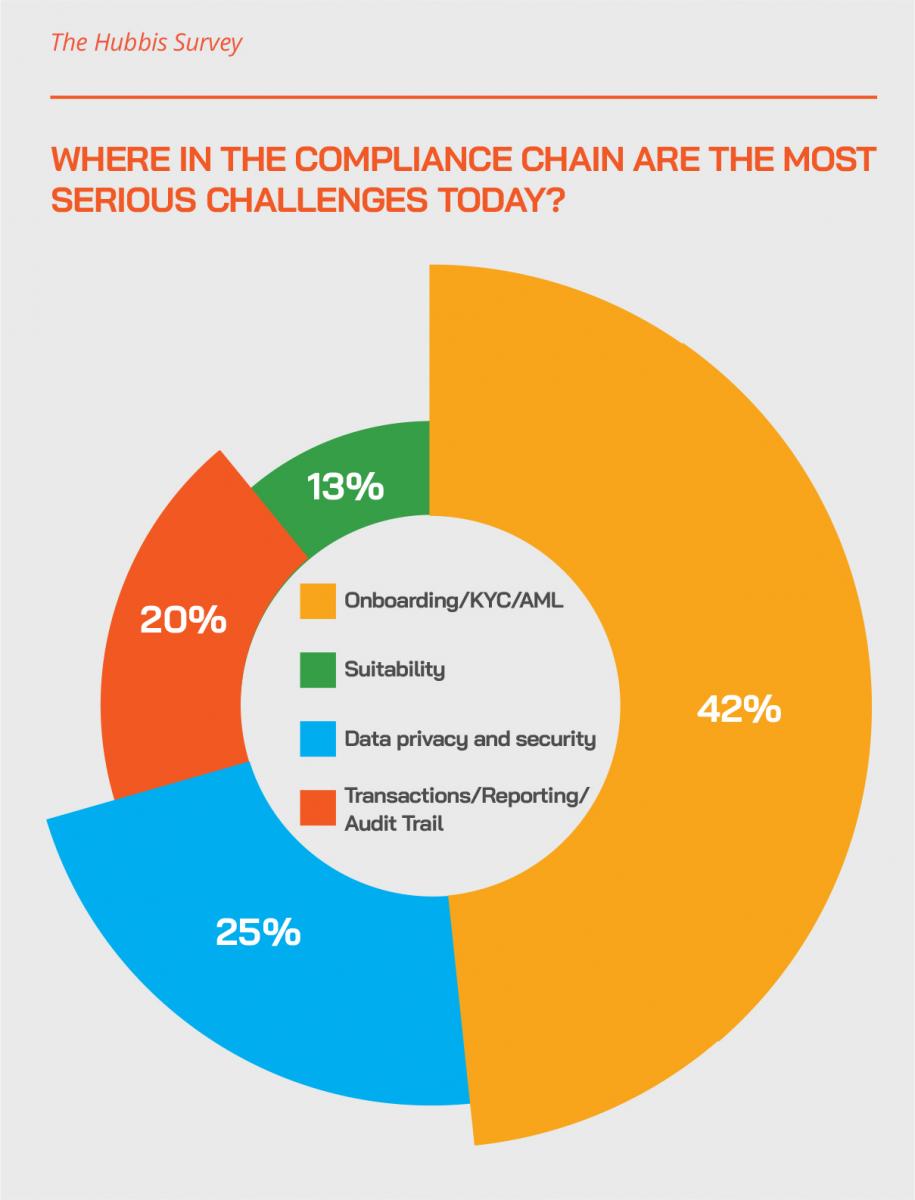

Onboarding challenges

Another area that involves the RMs and where there is increasing effort is onboarding and helping the RMs and advisors identity anomalies when clients come into the banks and other organisations to open accounts. Digital tools are increasingly relevant and powerful, including weaponry such as AI, analytics and ML, to help improve the outcomes, but also to help the RMs right from the outset of the process. Onboarding, screening and periodic reviews are direct beneficiaries of new digital tools, he reported.

“We look at the high impact areas, the high workload areas where we see false hits or just additional work for both RMs and try to see how we can streamline through technology,” he explained, adding that the wealth industry must adopt such solutions in order to become more efficient and to manage the greater complexity of the myriad of rules and regulations.

Another banker reported that their bank is very close to implementing robotic tools on negative news screening to improve the cumbersome and costly KYC process, which is largely manual today in the industry.

A fellow panellist agreed that better screening tools resulting in fewer false positives and better insights into the clients are actually rather expensive for the smaller firms, but also necessary. And reporting tools for top management to better understand their clients and their activities are also crucial to keep the business on track commercially and also compliant.

Sanctions – to be avoided!

An expert pointed to the rise in sanctions against financial institutions across the globe and how the scale of such sanctions has been rising fast, especially those delivered by the US Office of Foreign Assets Control (OFAC), the EU, the UN, OECD and others.

Be vigilant – fraud is rising fast!

Cyber-security, or the lack of it, is often the wormhole through which fraud can be unleashed; there is indeed a fast-expanding and increasingly agile and malevolent global machinery to defraud institutions and individuals. Some fraud, an expert commented, might be facilitated initially by non-malicious issues such as hardware of software problems, creating vulnerabilities at organisations, and some fraud is far more planned and malicious, with people internally not properly monitored and controlled and criminals externally fighting to take over data and systems for their own gain. Here again, conduct, culture and accountability are essential to mitigating these types of cyber risks.

Operational resilience

An expert commented that much of the efforts they are making with their bank and other clients is around operational resilience to help ensure that cyber-attacks are averted or better managed, especially amidst the rise in ransomware. “There are three types of financial institutions,” they commented. “Those who have already been the subject of a cyber-attack, those that will be the subject of a cyber-attack, and those that may actually already be the subject of a cyber-attack, but don't know it yet.”

They added that the issue of whether to pay a ransomware demand often comes up, and that is muddied by the likelihood that many of these cyber criminals already appear on some of the domestic or multilateral sanctions lists, further complicating matters. “In those cases, that type of situation can very well preclude a payment being made,” they explained, “while in other cases, we are seeing payments being made due to the need to get systems back running and online, as there are dangers of course from long disruptions.” They added that the whole arena of operational resilience is therefore increasingly central for financial institutions.

Virtual compliance

Another expert pointed to the need to apply a proper compliance regime around the numerous virtual meetings now taking place, similar to the face-to-face protocols that have been in place increasingly in recent years. He explained that smart digital tools can help significantly in this area, by digitising what can be immensely lengthy pdfs full of rules for domestic and internal guidance for client-facing bankers and advisors. “He explained that by using this type of smart tool the organisations can help their RMs and the RMs can help themselves, so that they both understand and adhere to strategic policies of the banks and firms.

He also observed that in the complex regulatory arena of investment advisory and suitability, smart digital tools can be applied in a similar manner so that domestic and cross-border rules and regulations can be much more easily embedded into the business practices and processes. “Once the RM comes up with a portfolio,” he reported, “as he or she is putting together an investment proposal for a client, all those rules are checked automatically in the back, and actually recommendations can be made based on regulatory or tax restrictions.”

Brief lulls, but more regulatory storms ahead

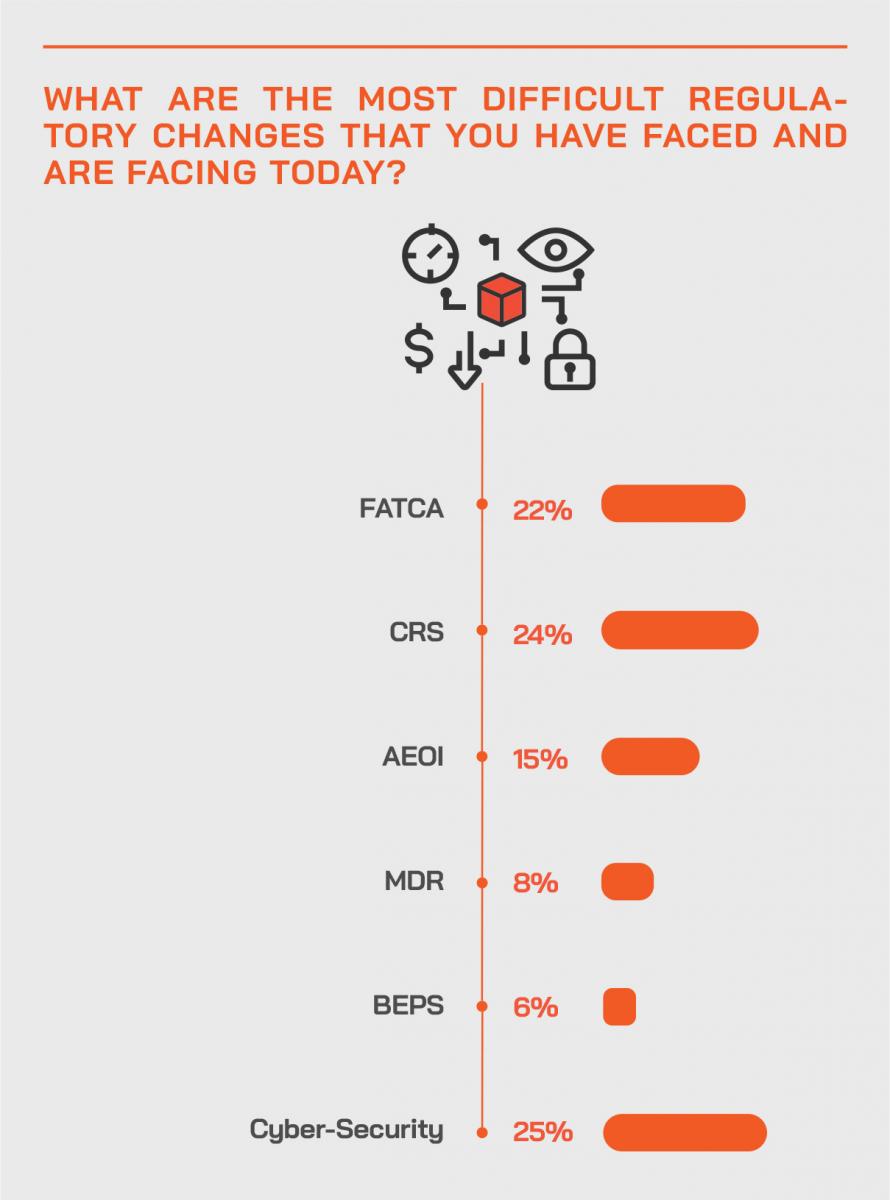

Although the regulators took their foot off the pedal somewhat during 2020, they are generally now back energetically pushing out new rules and guidance again, making it tough to keep up with the many changes, especially for the smaller firms. An expert highlighted for example plans to implement mandatory reference checks for representatives, with the MAS due to deliver more on that issue, and the HKMA having offered their views on this topic. This is likely to impose yet another major layer of compliance ‘paperwork’ as for example there is talk in Singapore of mandatory information on this topic to cover the compliance history for up to a 10-year period.

The drive for efficiency and alignment

From an operator’s perspective, the ever-rising burden of compliance means greater need for headcount, analysis and implementation. But as one guest explained, it is not feasible to continue to expand headcount, so the drive for greater efficiency is full on.

Another expert pointed to the need to align business expansion – which was robust in 2020 – with appropriate risk management, and within the resources that are available and realistic.

Expert Opinion -Ralf Huber, Co-Founder, Apiax: “We see a rapid shift away from traditional resource-intense compliance frameworks which are based on policies, training and monitoring towards digital-centric compliance frameworks. And there are obvious reasons for this: reducing compliance risk by replacing sample-based compliance monitoring with an embedded compliance solution.”

Expert Opinion - Rolf Haudenschild, Co-Founder, Ingenia Consultants: “Technology will be a key enabler of compliance. However, small financial institutions will struggle to purchase solutions and tailor them to their needs without support.”

Digital solutions

A guest highlighted the growing range and efficacy of digital RegTech solutions to compliance. A core challenge, he reported is to change the approach to compliance, to new ways to manage the greater complexity, and at the same time to support the business.

He said he sees a big shift in compliance and legal functions becoming digital, taking on innovative solutions that help the business. This, he said, is embedded compliance, where there is a close relationship between the actual business and the regulatory environment and compliance at the bank or wealth firm. “This involves a shift towards digital and compliance-by-design framework,” he reported.

Huge potential ahead for digital solutions

Another expert pointed to the enormous potential for such smart digital tools to enhance practices, monitoring and outcomes, and thereby help guide practitioners away from the regulatory dangers that are so prevalent and ubiquitous these days. He said there are huge advantages for the banks and wealth firms, for the team members, and of course also for the clients themselves, especially potentially from a tax compliance perspective, and particular when investing cross-border. “This,” he stated, “can add real value for the clients. “With new tools and AI and machine learning, the organisations can work more closely together with clients, help reduce complexity, and make the whole process more efficient, and at the same time more compliant.”

Expert Opinion - Rolf Haudenschild, Co-Founder, Ingenia Consultants: “Covid-19 initiated a massive shift to remote working. Resulting technology risks (and other risks) must be properly mitigated.”

Expert Opinion - Ralf Huber, Co-Founder, Apiax: “Providing investment advice is highly regulated in many countries. This means that the interpretation of cross-border, product, ESG, suitability and tax restrictions by relationship managers—without tech support—can suppose a big risk.”

Many rivers to cross for EAMs

An expert highlighted as an example some of the compliance and licensing rivers to cross to establish and operate an EAM in Singapore, starting with the application for the Capital Market Services (CMS) license for funds management to provide discretionary asset management services. He explained that there had been a steady increase in numbers, both local firms setting up and foreign firms establishing a local base. He explained that there are certain mechanical requirements in terms of personnel, capital and so forth, and then these firms need a proper operational framework for compliance and risk management, at a scale relevant to the business.

He highlighted the key operational risks for EAMs of the WFH protocol, which imposes a new layer of challenges around connectivity, risk, cyber-security and so forth. To help with this in Singapore, the MAS, he reported, had for smaller financial institutions introduced the digital acceleration grant for co-financing up to 80% to implement remote working and enhanced efficiency technologies.

ESG in the spotlight

Another guest highlighted the immense efforts taking place globally to move ESG into a more regulated environment, so that the taxonomy and definitions and data points become more standardised, all of which will help further boost the already rapidly expanding world of ESG investing. He said that this will also directly impact how companies and organisations report themselves, so that the reality of their strategies and activities are more plainly visible and not obscured by misinformation from internally or from PR experts.

“We do a lot of work now with wealth management organisations, with banks and asset managers, to look at ESG compliance, making sure that as people look to change their investment style to be more suited to ESG, helping make sure they have the data component to back that up,” he added.

Product due diligence

Those comments led onto the need to conduct appropriate due diligence on new products and funds offered to investor clients. “I think the key challenge for most of the private banks is where clients invest in funds that are not actually approved internally, which are actually outside of the bank, and that's proving particularly difficult to manage as a risk, so how do we put on some controls to mitigate that type of activity, and how do we actually make sure that the RM is not recommending clients to invest in something that is actually outside the bank's approved product range. That will continue to be a challenge for some time.”

Pricing and fairness

The panel also discussed pricing and best execution practices, noting that the regulators have been circling these particular wagons for some time already, including looking at price changes between instruction and execution and so forth.

Compliance cannot be brushed under the rug

The final comment went to a banker who observed that the increasingly complex world of regulation, and the rising drive to accountability of both personnel and their organisations combine to produce an environment in which compliance needs to advance in terms of its technologies, its processes, and its internal adoption throughout those banks and wealth firms. If compliance is not fully embedded within each entity, there will be disruptions and dangers and the rising risks might then run rampant.