So much of the world’s highest quality sovereign and quasi-sovereign fixed income was submerged in negative yield territory for most of 2020 while the ongoing global pandemic wrought devastation on many of the economic, fiscal, credit and equity market assumptions that analysts and investors had previously held. But China is a different story, and its onshore fixed income market is simply vast and also growing apace.

PANEL MEMBERS

- Donald Amstad, Global Head of Client Growth, Aberdeen Standard Investments

- Bruce Zhang, Fixed Income Portfolio Manager, CSOP Asset Management

- Ye Ting Ting, Chief Operating Officer, LU Global

- Dhiraj Bajaj, Head of Asia Credit, Fixed Income, Lombard Odier

- Johan Jooste, Managing Director, The Global CIO Office

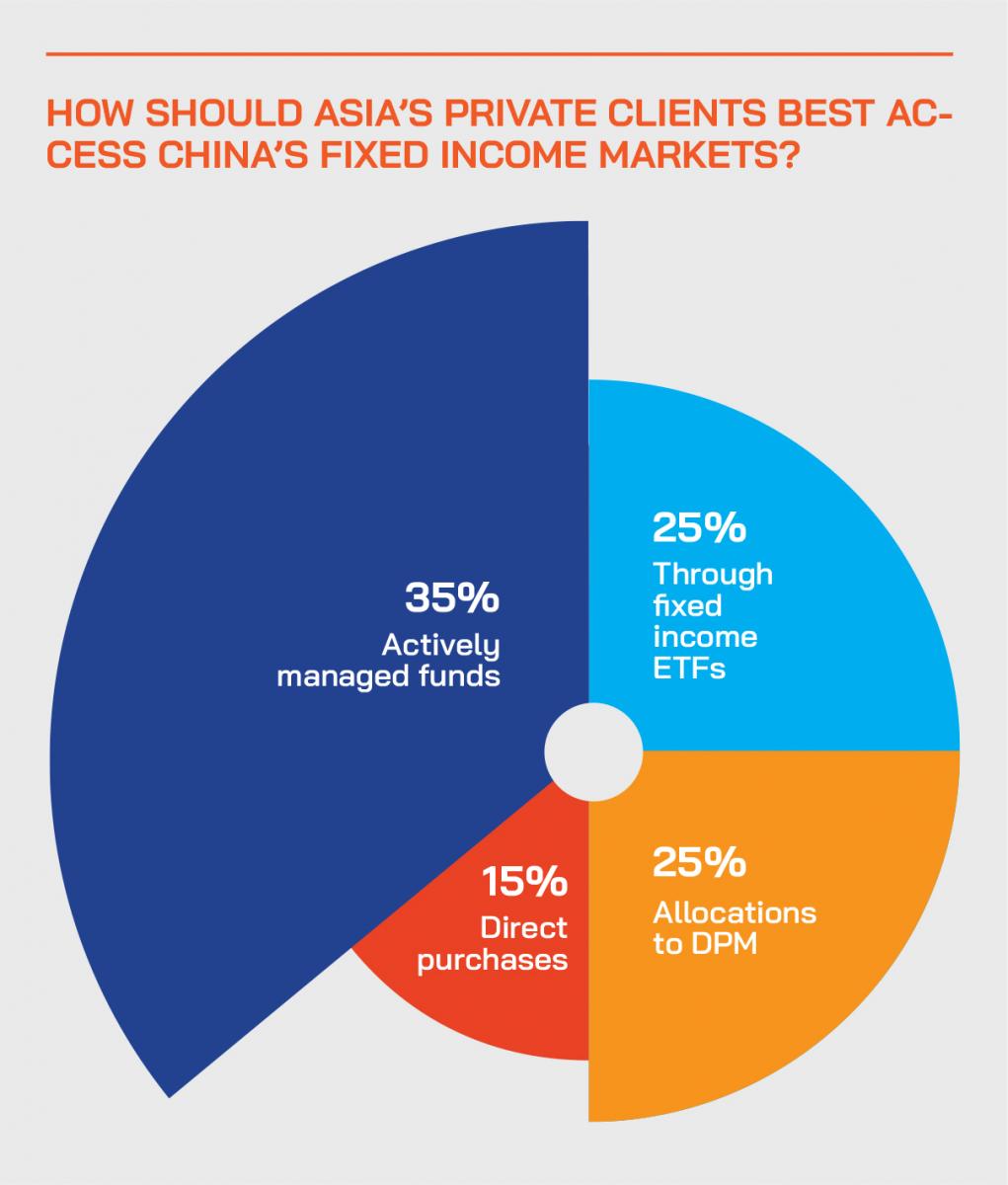

As the onshore debt market liberalises and as China aims to attract more foreign capital to this enormous sector of its capital markets, there is immense opportunity for investors to participate, but there are also huge dangers in taking the wrong approaches, misunderstanding the market and making the wrong investments. Thus far, foreign investors have largely cut their teeth in China’s debt market in offshore US dollar corporate bonds, or the offshore RMB bond market – known as the ‘Dim Sum’ market. But the range of paper is limited and it is the onshore RMB bond market, now valued at the equivalent of over USD14 trillion, and second in size only to the US bond market, that is attracting the most attention these days. However, accessing this vast market as a private investor is remarkably difficult and potentially treacherous. However, more and more investors are lining up to do so as a major diversification taking in both credit and currency exposures in the search for yield and capital gain in a world of falling and often negative yields. The optimal route into China’s onshore debt market for private clients in Asia is therefore to buy either the still relatively limited number of fixed income ETFs – best for government paper - or the actively managed funds whose managers have genuine expertise in the onshore bond market, and which are realistically the best way to gain exposure to onshore RMB corporate paper. Asia’s private clients will very tentatively be following the leading global institutions, who are themselves very gradually allocating more capital to this market as global bond benchmarks slowly incorporate more Chinese bonds into their indices. At the same time, the whole ecosystem involved in China’s onshore debt markets is evolving to include more and better-recognised credit ratings, as well as more and better research from reputed sources. But as our panel of experts agreed on July 15, while the opportunities are immense, the approach must be one of caution.

Some of the questions addressed:

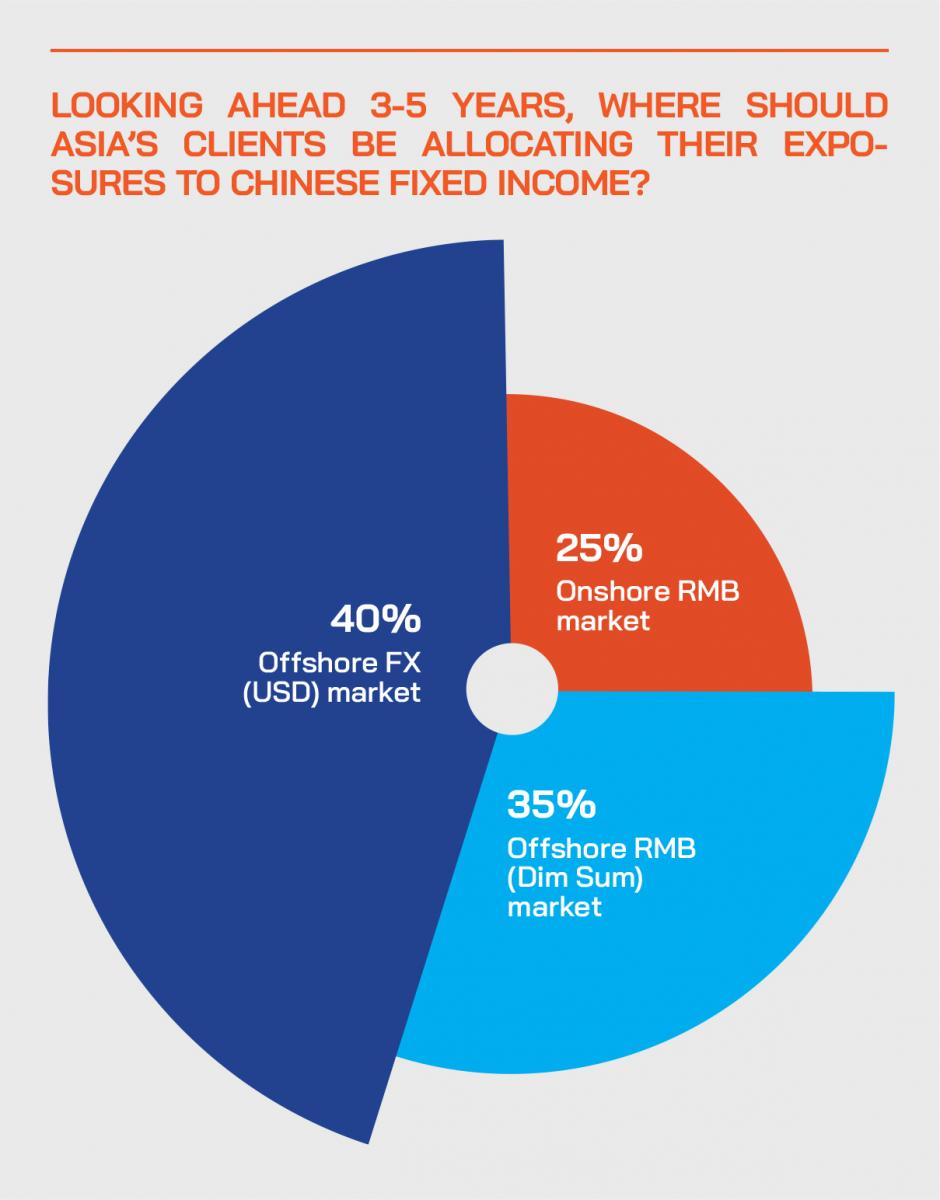

- How big is China’s fixed income market, in onshore RMB paper, offshore RMB (Dim Sum) paper and in offshore FX-denominated paper, and why is the overall market gaining more attention amongst international investors?

- What is happening to China’s fixed income market in terms of global bond indices and percentage weightings, and why?

- Is this a market in which private clients should get exposure?

- How do foreign investors access the market and find the best opportunities?

- ETFs? Actively-managed funds? Allocating specific money to DPM mandates? Which way is best?

- What are the dangers, and what are the must-avoid sectors?

- Is there a genuine risk of financial and currency instability in China?

- Is China’s financial sector liberalisation – both of the fixed income market and of the RMB - opening the doors to great opportunity or potential disaster for foreign investors?

- Are foreign credit rating agencies making headway in the onshore market both from a regulatory and also a credibility point of view?

- What are the most appealing segments?

- What about ‘Green’ bonds, are they really taking off, or will they?

- How is Asia’s wealth management community addressing the opportunity?

An expert opened the discussion by remarking that this is a once-in a generation opportunity to join in the opening up of the second largest domestic capital market in the world to foreigners. “It is only 40 years since Deng Xiaoping opened up the Chinese economy to the rest of the world, and it is now the second biggest economy in the world,” he said. “And now the signature policy of Xi Jinping or one of the signature policies, is this opening up of China's bond and stock markets to foreigners. It's a momentous event.”

Higher yield, lower volatility, better diversification

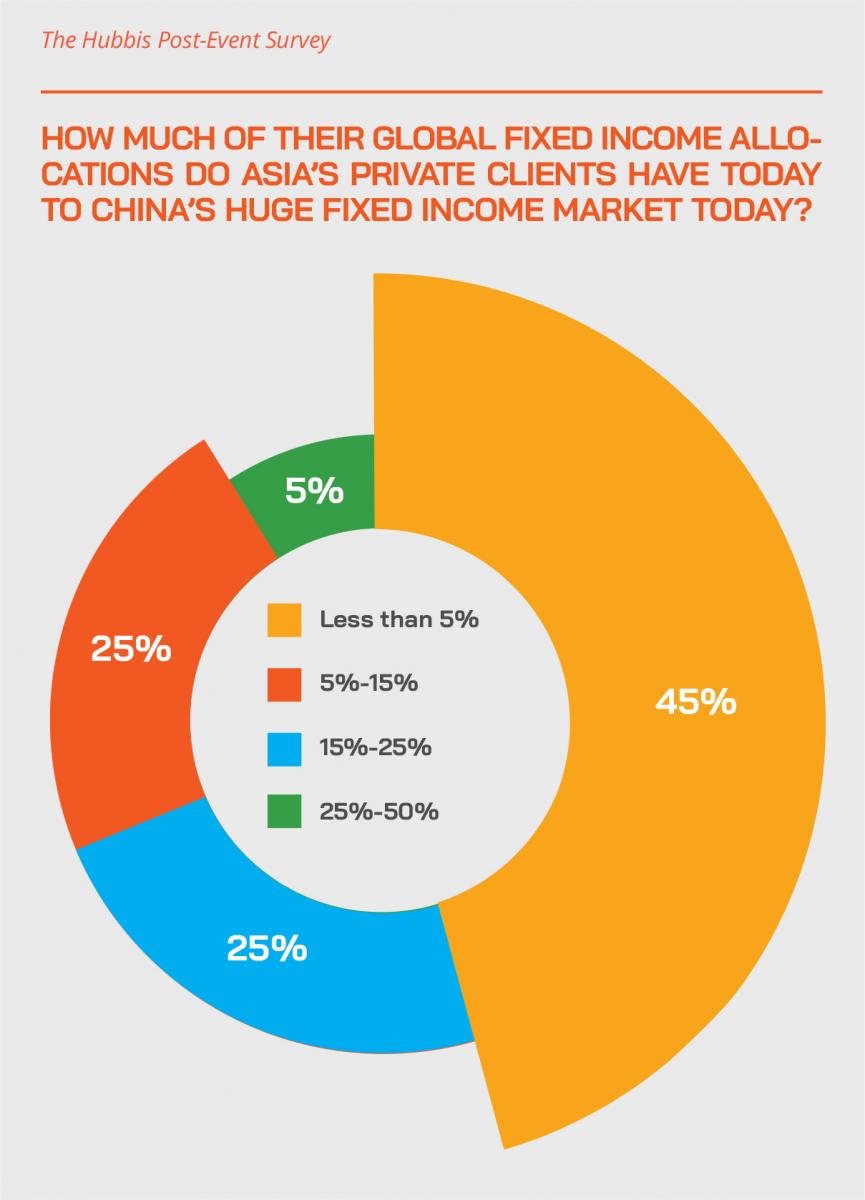

He said there are three important elements. The 10-year Chinese government bond yields around 3%, while in the US it is 1.3% roughly, and global high yield paper around 3%. “The junk bond market as we used to know it should be renamed the not very high yield bond market,” he quipped. Secondly, volatility in both the Chinese currency and the Chinese onshore bond market is very low. Thirdly, the diversification benefits are very high, with only 3.5% of this enormous USD17 trillion equivalent bond market owned by foreigners, meaning price determination come from onshore investors focused on domestic not international news. “All these factors,” he stated, “make for an extremely attractive proposition.”

Another expert with long experience of the EM fixed income markets reported that sovereign wealth funds, insurance, pension and other major funds allocating globally have very little exposure to China. “China’s growth has been so rapid and the liberalisation of the financial markets is only quite recent,” he reported. “We are now in the midst of the epic creation of a debt market opening up to the world, yet global clients have had very little time to understand it all, so the trillions of US, European and other money has barely started scratching the surface of China.”

Expert Opinion - Donald Amstad, Global Head of Client Growth, Aberdeen Standard Investments: “At Aberdeen Standard Investments (ASI) we find Chinese Onshore Bonds tremendously attractive for three reasons : yields are high, whilst both volatility and correlation with other asset classes are low. The ASI China Onshore Bond strategy in Luxembourg is an ideal solution for those who wish to take an active approach to this opportunity.”

Dipping toes onto the vast ocean of Chinese debt

He said these funds are therefore still at the stage of reading research on what to make of the China onshore inclusion to the Barclays Global Index, and whether they should buy into the market offshore or onshore.

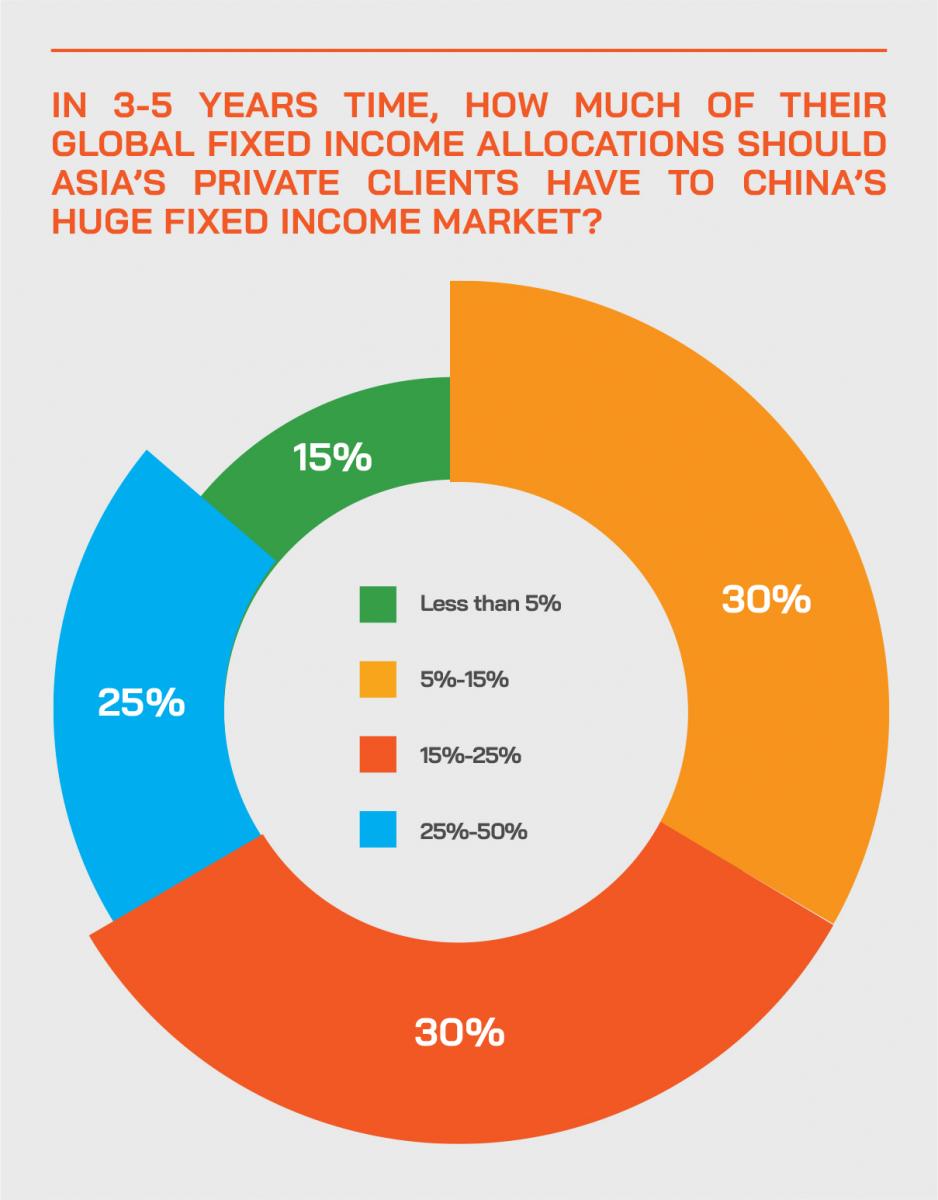

He added that those who had been buying into Asian credit in recent years had been testing the market, but still consider it very small and not yet meriting the establishment of teams in the region to cover the markets directly. “Investors are working on this region from outside Asia, but things will change in the next five years, the wave of capital that will come in is huge. It has stated and it will accelerate.”

Another expert remarked that the Chinese currency is in the next 5-10 years likely to be more dominant in global trade. Allied to solid credit, which we think the Chinese government certainly has, and this is an historic opportunity,” he stated.

Investors must choose their access points carefully

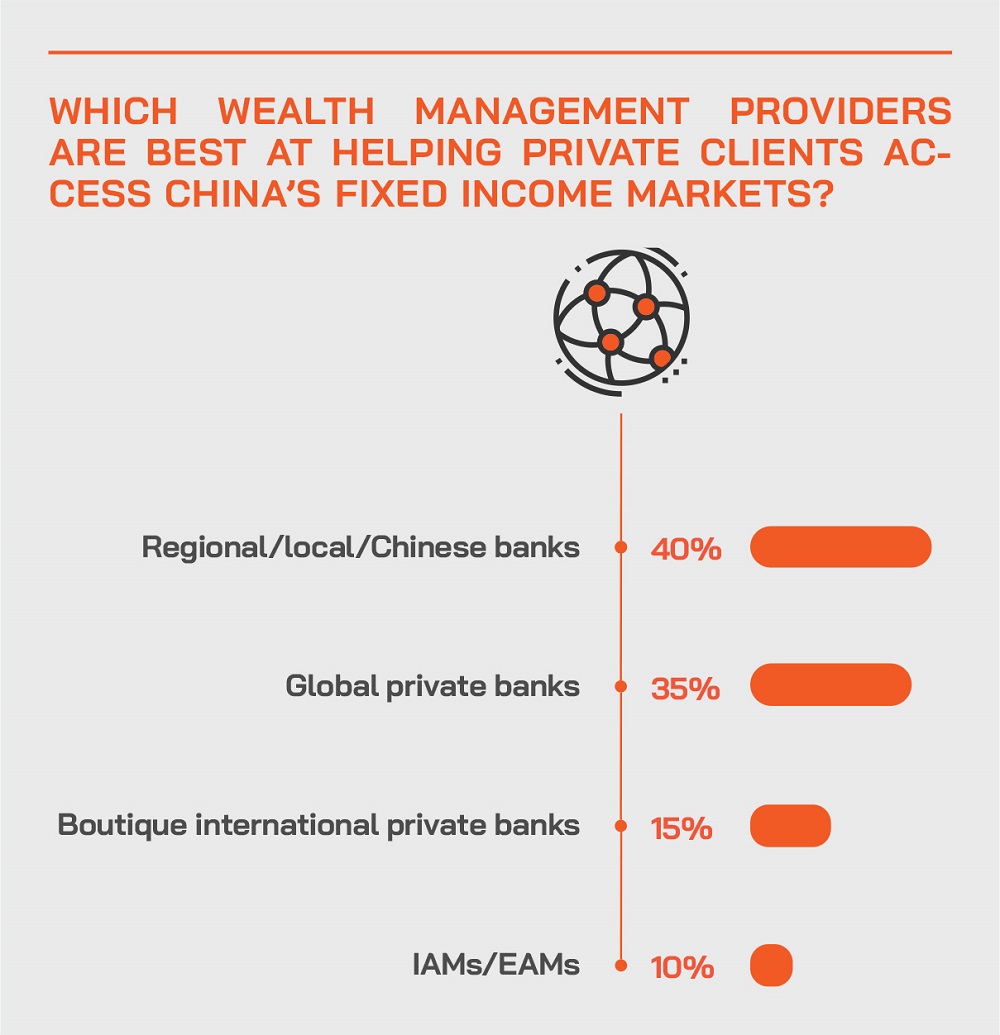

As to private clients in Asia, he observed that they are not yet equipped to venture into the market directly. “If I am advising a client on US high yield or global high yield or emerging markets, there's every possibility that we can source those bonds directly for them, but for China onshore that is a much bigger challenge.”

Another guest explained that foreign investors can actually directly access the markets through, for example, CIBM Direct, Bond Connect or QFI, but for private clients it remains difficult to directly invest into the Chinese onshore bond markets. For example, the entry level trading size, within the CIBM, the interbank market, starts from RMB10 million, or just over USD1.5 million. Comparatively, he remarked that ETFs can be quite efficient vehicle, as they have onshore access, smaller trading thresholds, and are relatively easy to trade in and out of.

A panellist explained that as one of the largest China-centric ETF providers, both equities and bonds, they offered one of the largest Chinese bond ETFs. The FTSE Chinese Government Bond ETF now has AUM of about USD1.5 billion, he reported, and invests solely in the onshore China government bonds issued by the Ministry of Finance. All the underlying bonds are rated at A1 or A+ by S&P or Moody's. “Actually,” he noted, “these credit ratings are quite high, equivalent to Japanese Government Bonds.”

The appeals of some compelling numbers

Another guest agreed with the appeals of the Chinese market, quoting figures of a 4% annual return in dollars for onshore China government bonds with volatility low at around 4% annualised.

“The return risk ratio is actually close to 1, and the correlation is very low versus major developed market paper, just 0.3 over the past 12 years actually,” he said. “With the high credit rating, it is an excellent diversification opportunity.” And with the prospect of inclusion in the FTSE Russell index, slated for October this year, that will bring well over USD100 billion equivalent inflows to Chinese government paper in the coming few years. Add to that the 50bp rate cut from the government, and that all adds up to a bullish environment, he said.

A panellist zoomed in on risks and the currency. He remarked that the Chinese Yuan had been remarkably stable, and more on a strengthening trend. And regarding credit exposure, he said there is a debate as to whether investors should take credit risk onshore or offshore.

The market, regulation and practices need to further develop

He reported their preference is to take credit risk in the offshore US Dollar bond markets. “There are two reasons,” he explained. “First, the spread over the benchmark government bond is a lot wider than similar onshore paper. The offshore paper is also governed by London and New York laws, whereas onshore there is a lack of proper and proven bankruptcy procedures. If you buy a high yield bond issued by a US entity, you have a very clear idea of what the recovery value of that bond is in the event that that company declares bankruptcy, you can price that to within 10 points in terms of recovery value.” But there is nowhere near those levels of certainly onshore in China.

He explained that in their China onshore (actively-managed) bond fund is centred on the benchmark of government paper and, while the fund can buy into onshore credit, this is only done if the conditions are exactly right, and then credits are chosen from the bottom-up analytical approach.

Expert Opinion - Donald Amstad, Global Head of Client Growth, Aberdeen Standard Investments: “ “At ASI we believe that an active approach is especially important when taking credit risk in the Chinese bond markets, both onshore and offshore; both in terms of how much credit risk to take and in terms of which individual bonds to buy.”

China – keeping the lid on inflation

An expert observed that inflation is very much frowned upon as a political hotcake because the mantra of the government is social stability, for which you require economic sand financial stability. They are very focused on keeping the inflation genie in the bottle, he reported, whereas other governments around the world have a different view currently.

“China shut down first and then came roaring back and is 6-12 months ahead of the world in terms of economic activity,” he reported. “While the US economy is now performing much better, the Fed is thinking about raising rates just at the time when China is cutting. This offers tremendous diversification benefits through an allocation to Chinese onshore bonds.”

Another expert observed that many elements of inflation – for example power and food prices – are controlled by the national or local governments, unlike in the liberalised Western economies.

Onshore credit is the riskiest play

A guest returned to the issue of credit risk, reporting that some argue onshore credit is better as it is closer to the actual issuers and assets, while his firm is of the view that the offshore market is actually preferable for building credit exposures.

“The offshore credit market is a lot smaller, but the onshore market is very homogeneous, it is basically controlled by the local rating agencies, the liquidity is low, the processes for buying and selling bonds are different, and the players are very different,” he reported. “Essentially, it's a very one-way market. In the offshore market there is more dispersion, and there is generally considerably more liquidity – when things become difficult, there are usually different sources of capital that will come in, such as global distress funds, private funds, global high yield buyers and some other Asian accounts. This diversity of accounts brings a lot more liquidity into the market for people to exit if needed.”

But in the onshore market, trading in tough times is limited and prices can jump around significantly. “People get spooked,” he reported, “as sometimes there might be no exit.”

An additional reason for taking the offshore route for accessing Chinese credit is duration, as it is relatively easy to hold on for 5, 7 or 10 years to achieve the returns investors anticipated.

But the offshore credit seas need careful navigation

On the other hand, the offshore market has its negatives as well. Looking back in time, he said that when the offshore credit market went significantly wider, the same names that were significantly tighter in 2015-2016, when the Chinese regulators liberalised the bond markets, allowing these companies to issue onshore for the very first time. And in 2017-2018, the authorities had stopped their onshore issuance, leading yields in the dollar market to spike.

Country Garden was a well-known case, with yields of 4% or 5% jumping to 10% and then issuing again in early 2019 at 8%. Today, those bonds are trading at 3% or below. These big swings open the door to significant capital losses, but also if timed properly significant gains. He pointed also to the far better and broader research available for offshore bonds, all of which also helps create a far more efficient market than onshore.

He noted we have already seen in 2021 that there has been weakness specifically in the high yielding segment of the offshore Chinese FI market.

“It is an opportunity for investors to pick through some of the opportunities obviously,” this expert remarked. “Not all opportunities are going to be great, but there are significant alpha opportunities and money should be put to work, especially given what we have in the rest of the world, in US, Europe and some other parts of emerging markets, where for example LatAm high yield bonds are trading at 3% plus on the back of how tight US high yield is. It is really unprecedented to get 10% to 15% for Chinese high yield bonds. And we have seen before how they can then bounce, and yields go back to 5%.”

Onshore – best for government paper

A panel member addressed credit risks in China onshore and offshore. Government credit is liquid and highly rated. But credit has a wide dispersion of quality, with the best controlled by the government and the worst without that government support. For those, credits, he advised, take the active funds approach, not the ETF route. He also reported that at this time, there is no evidence of major default risk in Chinese credit, despite what had been happening to names such as China Huarong, which has a significant volume of offshore dollar paper outstanding.

A guest pointed to hurdles for international investors in approaching the domestic market, including the poor information on and also differentiation in pricing for onshore credit, something unlikely to change until the global rating agencies cover the onshore market. International buyers see the logic and opportunity, but the lack of clarity and transparency are major deterrents currently.

The Hubbis Post-Discussion Survey

Very briefly, what are the key developments that need to take place to make China's onshore fixed income market more appealing to international investors?

- Opening up by China’s authorities for foreign capital to invest directly.

- Liberalisation/internationalisation of the RMB for easy convertibility.

- Having better Chinese local rating agencies that international investors can trust.

- Development of the Chinese legal system and governance framework to deal with bond defaults, restructurings.

- Improving the rule of law including bankruptcy protocols.

- More transparent credit ratings and allowing much more and easier access by international rating agencies.

- Lower entry investment thresholds.

- Greater and better regulation, governance and transparency.More understanding of government policy.

- Currency convertibility for RMB onshore.

- Better financial scrutiny of companies.

- Easier working relationships with Western firms, banks and investors.

- Sincere openness to work with the international parties.

- Increased transparency but most importantly, there should be clarity what happens in case a bond issuer struggles or defaults. The legal framework should be set up preferably similar to the well-proven European civil law.

- Having more of the China onshore bond issues rated by international rating agencies like

- Standard & Poor, Moody’s and Fitch.

- More transparent bid/offer pricing mechanisms.

- Greater liquidity.

- It needs to have a more open market environment offered to foreign investors, such as ease of FX control, investment restriction, etc.

- Accessibility and education.

How would you characterise the opportunity opening up in China’s fixed income market for Asia’s HNW and UHNW private clients?

- Limited. It is not easy for HNW and UHNW to directly buy into the China onshore bond markets. Most players currently are Institutional clients with relevant licences.

- Exposure to China's fixed income market could improve risk adjusted returns.

- Most PB clients are still wary of Chinese credits, due to increased default rates and negative news.

- It will be very appealing, but later as there are many issues to be solved first.

- It will be increasingly attractive if the US Dollar keeps declining.

- It might take a while as the trust component is not there yet, so there is a long way to go.

- It looks enticing offering diversity in asset allocations to World’s second largest economy for

- Asia’s HNW and UHNW.

- A great alternative to the prevailing international fixed income space.

- Excellent, it has huge potential.

- It will be a potential high-growth asset class for Asia's HNW and UHNW market in the future.

- An excellent choice. But most Chinese firms are not as transparent as those in the developed markets, and we need to be wary over their financial statements, but when that is clearer, there is great potential.

- Definitely opening up, and we are welcoming increasing product offerings through vehicles such as ETFs or active funds.

What are the key attractions of the Chinese fixed income markets, and which types of issuers offer the best opportunities, and very briefly, why?

- Higher yields versus developed market government bonds, diversification benefits and the huge domestic market. At the current time, we look only at the onshore government bonds and for corporate paper prefer to go offshore.

- Diversification, there is almost zero allocation amongst international investors to this truly vast market.

- Higher yields/spreads as compared to traditional developed markets for fixed income.

- Higher yields. The government bonds, or paper issued by major financial entities offer the

- best opportunities.

- China is growing.

- A stable economy and clear interest rate policy.

- Higher yields, lower correlation to global markets. Take the top-rated Government paper, which offers appealing yields with minimal or almost zero risk.

- Yields, stable currency, government strategy and organisation, strong antipathy at state and semi-state level to inflation, and powerful controls against price rises in CPI constituents, improving regulation, gradual liberalisation, and arrival of more international money will further drive impetus and evolution of this truly vast market.

- Corporate issuers, but we prefer to access them offshore and highest credits and most transparent companies in best sectors.

- We like corporate paper, in the financial, industrial, property and technology sectors.

- Chinese fixed income markets offer better yield and stable rating for the government bonds in comparison to global government bonds.

- China has more fiscal power and government control to maintain stability in their ratings and currency. They can and will weather the storms that are inevitably ahead in one shape or another.

- Higher yields and higher growth prospects aligned to liberalisation and improving clarity is a great combination. Stick to government paper and the very best corporate paper – offshore first – for now, and then gradually expand into onshore credit as things become clearer in the years ahead.

What are the main risks in China’s fixed income market, and why?

- Poor corporate governance.

- Opaque legal system.

- Questionable quality of ratings.

- Bankruptcy laws and therefore recoveries not yet clear or effective.

- Relatively illiquid.

- Significant but also potentially difficult to quantify credit risks.

- Lack of clear information on the onshore credits.

- many issuers have complicated shareholding structures.

- Many issuers are highly leveraged.

- Inadequate investor protection.

- Lack of transparency.

- Weaker corporate governance, but better for offshore issuers.

- Strong government is good in many ways, but means there is also susceptibility to sudden major policy shifts.

- High levels of corporate debt.

- China-US tensions, might escalate unexpectedly.

- Worries about China flexible its military might and projecting its power overseas, much as the US has done for decades since WW2.

Should Asia’s private clients take a larger exposure to China’s fixed income market, and if so, why?

- Yes, in the offshore segment, not onshore.

- Yes. They should be taking a larger exposure to reduce correlation with traditional asset

- classes. This could provide better risk adjusted returns.

- Yes, for diversification.

- Yes, for diversification into higher yields in this low yielding environment, but via a fund structure with active management.

- Yes, we are long-term positive about the currency.

- China's fixed income market is mainly open to institutional investors, whereas the entry size will be an impediment for the private clients.

- Yes, but they should be aware of the asymmetric risks that exist in the market.

- No great sense yet, wait a few years to see how things develop and see if there is greater clarity and liquidity. Onshore, only buy government bonds, nothing else. Offshore, stick to the best and most liquid credits in less volatile or unpredictable sectors, and then take only modest exposure.

- Great diversification into the worlds second largest economy and second largest debt market.

- Yes, but stick to liquid ETFs or the best-managed active funds.

The passive versus active discussion

Another expert agreed with that comment, noting that ETFs neatly fit the government bond market, even if that approach slightly diminishes the opportunity in playing the yield curve or tweaking some extra returns. “But I must stress the need to go active in credit,” he stated. “And that opens the door to the Green bond developments and the ESG agenda, both becoming much more important for offshore buyers, especially European investors, with the new regulations that are coming in Europe, and the drive in China to go carbon neutral by 2060.”

Green is the colour of the future

He explained his firm takes ESG very seriously and had a dedicated team and had linked up with AIIB, the Asian Infrastructure Investment Bank in Beijing to launch an Asian credit mandate, focusing on infrastructure throughout China and the region with heavy emphasis on ESG. “China going ‘Green’ is a huge thematic for the next decades ahead,” he stated, “and we will see a lot more ‘green’ bonds coming through in China.”

Expert Opinion - Donald Amstad, Global Head of Client Growth, Aberdeen Standard Investments: “ “Overseas investors hold only 3.5% of the Chinese onshore bond market. Therefore the price of Chinese onshore bonds is determined by local investors, who follow developments in Beijing and Shanghai, rather than London or New York. This is why Chinese onshore bonds are such a great diversifier for overseas investors.”

A panellist said that the market will evolve further when defaults are put to the test, as happened decades ago in Europe, setting precedents for the processes and the outcomes. The market will thereby find a way to cope with whatever names struggle or default, and after those events, there will be a degree of consistency in the way these problems are resolved, and then it will become easier to price. “That is part of the normal evolution of the market,” he observed. “Active is the right approach [to credit], as this is a development phase in the market. The US Chapter 11 has been around for decades, it is easy to assess the outcomes.”

China’s debt markets will inch closer to global norms

He also noted that while major global bond indices are the basis for global allocations from major funds worldwide, there is a real shortage of data for China. “In this case, it is best to mind your step,” he warned. “Without the necessary data, you can be blindsided. As more foreign players come in there will be closer correlation between Chinese and global bonds, they will converge slowly I expect.” Although China’s market ticks along on its own heartbeat almost completely without foreign participation, this will gradually change as more foreign money pours in.

This is a one-way road to market maturity

The final word went to a guest who observed that actively managed funds should also continue to develop their expertise, for example with partnerships with onshore asset management firms, as well as employing more investment professionals with onshore experience. It is important, he said, not only to understand onshore China credit markets, for example, in terms of their bond selection skill or their sensitivity to the internal news flows, but also because they have the insights of the onshore liquidity, because they may know how to trade those bonds efficiently and effectively